Você também pode gostar

- Fake Money, Real Danger: Protect Yourself and Grow Wealth While You Still CanNo EverandFake Money, Real Danger: Protect Yourself and Grow Wealth While You Still CanAinda não há avaliações

- Lane Asset Management Stock Market Commentary March 2012Documento6 páginasLane Asset Management Stock Market Commentary March 2012Edward C LaneAinda não há avaliações

- The Investment Trusts Handbook 2024: Investing essentials, expert insights and powerful trends and dataNo EverandThe Investment Trusts Handbook 2024: Investing essentials, expert insights and powerful trends and dataNota: 2 de 5 estrelas2/5 (1)

- Lane Asset Management Stock Market and Economic Commentary July 2012Documento7 páginasLane Asset Management Stock Market and Economic Commentary July 2012Edward C LaneAinda não há avaliações

- Lane Asset Management Stock Market Commentary April 2012Documento7 páginasLane Asset Management Stock Market Commentary April 2012Edward C LaneAinda não há avaliações

- Lane Asset Management Stock Market and Economic February 2012Documento6 páginasLane Asset Management Stock Market and Economic February 2012Edward C LaneAinda não há avaliações

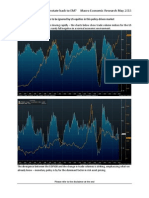

- Lane Asset Management Stock Market Commentary December 2011Documento8 páginasLane Asset Management Stock Market Commentary December 2011Edward C LaneAinda não há avaliações

- Lane Asset Management Stock Market Commentary June 2012Documento6 páginasLane Asset Management Stock Market Commentary June 2012Edward C LaneAinda não há avaliações

- Lane Asset Management Stock Market Commentary For October 2013Documento9 páginasLane Asset Management Stock Market Commentary For October 2013Edward C LaneAinda não há avaliações

- Too Much Love Will Kill YouDocumento7 páginasToo Much Love Will Kill YoumaAinda não há avaliações

- Market Analysis Nov 2022Documento12 páginasMarket Analysis Nov 2022Muhammad SatrioAinda não há avaliações

- Trading Range IntactDocumento8 páginasTrading Range IntactAnonymous Ht0MIJAinda não há avaliações

- Sweet Spot Fading enDocumento4 páginasSweet Spot Fading enwindson_sgAinda não há avaliações

- Market Analysis August 2021Documento19 páginasMarket Analysis August 2021Thanh Trịnh BáAinda não há avaliações

- Weekly Trends March 10, 2016Documento5 páginasWeekly Trends March 10, 2016dpbasicAinda não há avaliações

- There's Nothing Good Here: Views From The Blue RidgeDocumento8 páginasThere's Nothing Good Here: Views From The Blue RidgeZerohedgeAinda não há avaliações

- Lane Asset Management Stock Market Commentary May 2012Documento6 páginasLane Asset Management Stock Market Commentary May 2012Edward C LaneAinda não há avaliações

- Bear Marke - CorrecDocumento30 páginasBear Marke - CorrecSoren K. GroupAinda não há avaliações

- Analisis de Indicadores para Ver El Momento Como Inversor - 061022Documento10 páginasAnalisis de Indicadores para Ver El Momento Como Inversor - 061022Luis Gil - Inspira y AvanzaAinda não há avaliações

- LAM Commentary July 2011Documento8 páginasLAM Commentary July 2011Edward C LaneAinda não há avaliações

- The List Market Outlook en UsDocumento12 páginasThe List Market Outlook en UsothergregAinda não há avaliações

- EdisonInsight February2013Documento157 páginasEdisonInsight February2013KB7551Ainda não há avaliações

- FX Compass: Looking For Signs of Pushback: Focus: Revising GBP Forecasts HigherDocumento25 páginasFX Compass: Looking For Signs of Pushback: Focus: Revising GBP Forecasts HighertekesburAinda não há avaliações

- EPF March 2015Documento2 páginasEPF March 2015dpbasicAinda não há avaliações

- Is The Market About To CrashDocumento21 páginasIs The Market About To CrashSoren K. GroupAinda não há avaliações

- Lane Asset Management Stock Market Commentary February 2014Documento8 páginasLane Asset Management Stock Market Commentary February 2014Edward C LaneAinda não há avaliações

- Bar Cap 3Documento11 páginasBar Cap 3Aquila99999Ainda não há avaliações

- Lane Asset Management Stock Market Commentary August 2011Documento9 páginasLane Asset Management Stock Market Commentary August 2011Edward C LaneAinda não há avaliações

- Lane Asset Management Stock Market and Economic Commentary February 2016Documento11 páginasLane Asset Management Stock Market and Economic Commentary February 2016Edward C LaneAinda não há avaliações

- Stock Market Commentary November 2014Documento7 páginasStock Market Commentary November 2014Edward C LaneAinda não há avaliações

- Hussman Funds 2009-07-27Documento2 páginasHussman Funds 2009-07-27rodmorley100% (2)

- Olivers Insights - Share CorrectionDocumento2 páginasOlivers Insights - Share CorrectionAnthony WrightAinda não há avaliações

- Ecfp March 2015Documento2 páginasEcfp March 2015dpbasicAinda não há avaliações

- Lane Asset Management Stock Market Commentary May 2014Documento7 páginasLane Asset Management Stock Market Commentary May 2014Edward C LaneAinda não há avaliações

- The Global View: What Does The ISM Mean For US Equities?Documento5 páginasThe Global View: What Does The ISM Mean For US Equities?mustafa-ahmedAinda não há avaliações

- Hussman Funds - Stocks Extreme Conditions and Typical Outcomes - May 2, 2011Documento6 páginasHussman Funds - Stocks Extreme Conditions and Typical Outcomes - May 2, 2011KoalaCapitalSICAVAinda não há avaliações

- 06-06-2011 10:27 AM A Converation Between A Sell-Side Rates Trader & Buy-Side Equities TraderDocumento5 páginas06-06-2011 10:27 AM A Converation Between A Sell-Side Rates Trader & Buy-Side Equities Traderapi-80847199Ainda não há avaliações

- Convexity Maven: "A Model Portfolio - 2022"Documento12 páginasConvexity Maven: "A Model Portfolio - 2022"piwipebaAinda não há avaliações

- Chart Review - Can We Rotate Back To EM? Macro Economic Research May 2013Documento4 páginasChart Review - Can We Rotate Back To EM? Macro Economic Research May 2013kcousinsAinda não há avaliações

- ValuEngine Weekly Newsletter January 27, 2012Documento12 páginasValuEngine Weekly Newsletter January 27, 2012ValuEngine.comAinda não há avaliações

- Year End 2012 Investment Commentary: January 22, 2013Documento9 páginasYear End 2012 Investment Commentary: January 22, 2013api-196977895Ainda não há avaliações

- Investment Directions en UsDocumento12 páginasInvestment Directions en UsothergregAinda não há avaliações

- Don't Wait For May SAUT 041910Documento5 páginasDon't Wait For May SAUT 041910careyescapitalAinda não há avaliações

- Market Analysis Feb 2022 (Updated)Documento16 páginasMarket Analysis Feb 2022 (Updated)Penguin DadAinda não há avaliações

- Wally Weitz Letter To ShareholdersDocumento2 páginasWally Weitz Letter To ShareholdersAnonymous j5tXg7onAinda não há avaliações

- Samson Corporate Strategy BulletinDocumento5 páginasSamson Corporate Strategy BulletinAnonymous Ht0MIJAinda não há avaliações

- TomT Stock Market Model 2012-05-20Documento20 páginasTomT Stock Market Model 2012-05-20Tom TiedemanAinda não há avaliações

- MKT ThoughtsDocumento6 páginasMKT ThoughtselmoatazshawkyAinda não há avaliações

- Looking Ahead - The Market, Volatility & Portfolio PositioningDocumento5 páginasLooking Ahead - The Market, Volatility & Portfolio Positioningdominico833352Ainda não há avaliações

- GS Market Know How 1Q2015Documento20 páginasGS Market Know How 1Q2015asdfgh132Ainda não há avaliações

- 9/22/14 Global-Macro Trading SimulationDocumento10 páginas9/22/14 Global-Macro Trading SimulationPaul KimAinda não há avaliações

- Weekly Market Commentary 3-512-2012Documento4 páginasWeekly Market Commentary 3-512-2012monarchadvisorygroupAinda não há avaliações

- Deteriorating Financial Conditions Threaten To Escalate The European Debt CrisisDocumento2 páginasDeteriorating Financial Conditions Threaten To Escalate The European Debt CrisisKevin A. Lenox, CFAAinda não há avaliações

- Economist Insights 20120416Documento2 páginasEconomist Insights 20120416buyanalystlondonAinda não há avaliações

- Market Analysis November 2020Documento21 páginasMarket Analysis November 2020Lau Wai KentAinda não há avaliações

- Global Economics Weekly - Goldman Sachs 02.10.13Documento13 páginasGlobal Economics Weekly - Goldman Sachs 02.10.13Martin Tsankov100% (1)

- 0320 US Fixed Income Markets WeeklyDocumento96 páginas0320 US Fixed Income Markets WeeklycwuuuuAinda não há avaliações

- Hedgfx 19-06-2012Documento4 páginasHedgfx 19-06-2012HedgfxAinda não há avaliações

- Weekly Market Commentary 03092015Documento5 páginasWeekly Market Commentary 03092015dpbasicAinda não há avaliações

- ICMAniacs Report Final (In Need of Finishing Touches)Documento19 páginasICMAniacs Report Final (In Need of Finishing Touches)George Stuart CottonAinda não há avaliações

- Model Paper 1: Question No. 1Documento11 páginasModel Paper 1: Question No. 1Ashish SinghAinda não há avaliações

- Explanations: D) Short Term Capital Asset - S. 2 (42A) Income TaxDocumento3 páginasExplanations: D) Short Term Capital Asset - S. 2 (42A) Income Taxmanik kapoorAinda não há avaliações

- English HKSI LE Paper 1 Pass Paper Question Bank (QB)Documento10 páginasEnglish HKSI LE Paper 1 Pass Paper Question Bank (QB)Tsz Ngong Ko0% (2)

- Proposed Rule: Commodity Exchange Act: Investment of Customer Funds and Related Recordkeeping RequirementsDocumento17 páginasProposed Rule: Commodity Exchange Act: Investment of Customer Funds and Related Recordkeeping RequirementsJustia.comAinda não há avaliações

- ADR and GDR - CFDocumento16 páginasADR and GDR - CFlove_abhi_n_22100% (4)

- Basel II Capital Accord SlidesDocumento25 páginasBasel II Capital Accord SlidesAamir RazaAinda não há avaliações

- 2022 CiDocumento22 páginas2022 CiK60 Lâm Nguyễn Minh TấnAinda não há avaliações

- The Weekly Profile 01Documento65 páginasThe Weekly Profile 01Devie ChristianAinda não há avaliações

- Fundamental Analysis On Steel Sector & CompanyDocumento94 páginasFundamental Analysis On Steel Sector & Companykalariyadhiren75% (4)

- Reading 9 The Firm and Market StructuresDocumento61 páginasReading 9 The Firm and Market StructuresNeerajAinda não há avaliações

- A Guide To Futures Roll Analysis: TimingDocumento6 páginasA Guide To Futures Roll Analysis: TimingPARTHAinda não há avaliações

- Bank Statements AY 2020-21Documento21 páginasBank Statements AY 2020-21rohit madeshiyaAinda não há avaliações

- Arrey-Lambert - Dicussion 1Documento2 páginasArrey-Lambert - Dicussion 1Ismail AliAinda não há avaliações

- MKTG1100 Chapter 1Documento40 páginasMKTG1100 Chapter 1Marcus YapAinda não há avaliações

- The Sharpe Index Model: Hari Prapan SharmaDocumento11 páginasThe Sharpe Index Model: Hari Prapan SharmaHiral ShahAinda não há avaliações

- Revision Problem For Final Exam INS3032 2017Documento2 páginasRevision Problem For Final Exam INS3032 2017magical_life96100% (1)

- Beyond Cash Dividends: Buybacks, Spin Offs and DivestituresDocumento49 páginasBeyond Cash Dividends: Buybacks, Spin Offs and DivestituresayzlimAinda não há avaliações

- Discuss The Main Contribution of Modigliani and Miller To Financial TheoryDocumento4 páginasDiscuss The Main Contribution of Modigliani and Miller To Financial Theorykebede desalegnAinda não há avaliações

- Demo - Nism 5 A - Mutual Fund ModuleDocumento7 páginasDemo - Nism 5 A - Mutual Fund ModuleDiwakarAinda não há avaliações

- Order Block Institutional Trading Practical Guide by James J KingDocumento59 páginasOrder Block Institutional Trading Practical Guide by James J KingKishor shinde75% (4)

- Macquarie Infrastructure and Real AssetsDocumento28 páginasMacquarie Infrastructure and Real AssetsOon KooAinda não há avaliações

- 107 09 IPO Valuation ModelDocumento8 páginas107 09 IPO Valuation ModelAnirban Bera100% (1)

- Chapter 5.pptx Risk and ReturnDocumento25 páginasChapter 5.pptx Risk and ReturnKevin Kivanc IlgarAinda não há avaliações

- Grey Modern Professional Business Project PresentationDocumento53 páginasGrey Modern Professional Business Project PresentationNgọc Minh ĐỗAinda não há avaliações

- Case Study: Look Before You Leverage: Submitted To: Mr. Johnel Fil T. ArcipeDocumento8 páginasCase Study: Look Before You Leverage: Submitted To: Mr. Johnel Fil T. ArcipeWelshfyn ConstantinoAinda não há avaliações

- Aud Rev, Investments Wit Ans KeyDocumento17 páginasAud Rev, Investments Wit Ans KeyAngela RamosAinda não há avaliações

- A List of Wrong Narratives I Have Seen RecentlyDocumento2 páginasA List of Wrong Narratives I Have Seen RecentlyEdgar MuyiaAinda não há avaliações

- GST 231 Pq&a IiiDocumento4 páginasGST 231 Pq&a IiiMuhammad Ibrahim SugunAinda não há avaliações

- Trade Plan Worksheet: Analyze The Markets Implement Your TradeDocumento1 páginaTrade Plan Worksheet: Analyze The Markets Implement Your TradeActive88Ainda não há avaliações

- Deposi TED: B. C. Reg.Documento36 páginasDeposi TED: B. C. Reg.oregomez432963Ainda não há avaliações