Você também pode gostar

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

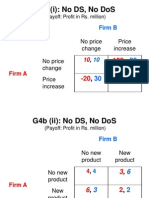

- G4B (I) : No DS, No Dos: No Price Change Price Increase No Price Change Price IncreaseDocumento6 páginasG4B (I) : No DS, No Dos: No Price Change Price Increase No Price Change Price IncreaseAnuj AgarwalAinda não há avaliações

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Communication ProjectDocumento3 páginasCommunication ProjectAnuj AgarwalAinda não há avaliações

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Infosys Technologies Limited: Type - PublicDocumento8 páginasInfosys Technologies Limited: Type - PublicAnuj AgarwalAinda não há avaliações

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- The Evolution of Management ThoughtDocumento30 páginasThe Evolution of Management ThoughtAnuj AgarwalAinda não há avaliações

- Defining Leg Vs Base Candle: Leg-Base Isolation Method For Buy Zones and Sell ZonesDocumento7 páginasDefining Leg Vs Base Candle: Leg-Base Isolation Method For Buy Zones and Sell Zonesrnumesh1Ainda não há avaliações

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- The Analysis of China's Housing Price Based On The Demand: 1 InstructionDocumento5 páginasThe Analysis of China's Housing Price Based On The Demand: 1 InstructionEkta DarganAinda não há avaliações

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

- Singapore Property Weekly Issue 346Documento9 páginasSingapore Property Weekly Issue 346Propwise.sgAinda não há avaliações

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- Accounting For Merchandising BusinessDocumento21 páginasAccounting For Merchandising BusinessJunel PlanosAinda não há avaliações

- Basic IqDocumento5 páginasBasic IqSidhartha JainAinda não há avaliações

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Pivot Point Trading Strategy GuideDocumento12 páginasPivot Point Trading Strategy Guideforstermakhado492Ainda não há avaliações

- Case - Study - Lumabao, Rianne Karisa - EntrepDocumento3 páginasCase - Study - Lumabao, Rianne Karisa - EntrepRianne LumabaoAinda não há avaliações

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- ECO101 Problem Set 7 Questions Firm CostsDocumento2 páginasECO101 Problem Set 7 Questions Firm CostsEshika SehgalAinda não há avaliações

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- InvoiceDocumento1 páginaInvoiceSumit AgrahariAinda não há avaliações

- Turbocharged - Assuming Coverage With Outperform - 23set19 - BBIDocumento17 páginasTurbocharged - Assuming Coverage With Outperform - 23set19 - BBIbenjah2Ainda não há avaliações

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (345)

- Amaia PampangaDocumento1 páginaAmaia PampangadusteezapedaAinda não há avaliações

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- 16 Inventory ValuationDocumento28 páginas16 Inventory ValuationSidra MalikAinda não há avaliações

- Name: - : InstructionsDocumento6 páginasName: - : InstructionsAboo HafsaAinda não há avaliações

- Industry and Marketplace Analysis: Stephen Lawrence and Frank MoyesDocumento20 páginasIndustry and Marketplace Analysis: Stephen Lawrence and Frank MoyesAjit ShindeAinda não há avaliações

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- Project On BankingDocumento31 páginasProject On BankingsarthakAinda não há avaliações

- Cost SheetDocumento15 páginasCost Sheetnagesh dashAinda não há avaliações

- Factory Overhead Can Be Charged On The Basis of - .: A. Material CostDocumento31 páginasFactory Overhead Can Be Charged On The Basis of - .: A. Material CostLeny MichaelAinda não há avaliações

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- File 01 - Bonds + Equity Practice QuestionsDocumento9 páginasFile 01 - Bonds + Equity Practice QuestionsNormanMichaelAinda não há avaliações

- Class VIII Test 13-11-2023Documento1 páginaClass VIII Test 13-11-2023Veena DhingraAinda não há avaliações

- Update - Debt Cancellation For Haiti: No Reason For Further DelaysDocumento18 páginasUpdate - Debt Cancellation For Haiti: No Reason For Further DelaysCenter for Economic and Policy Research100% (1)

- Tut 2-AfaDocumento10 páginasTut 2-AfaDiệp HyAinda não há avaliações

- Net Metering Reference Guide Philippines E.pdf 2Documento88 páginasNet Metering Reference Guide Philippines E.pdf 2jhigz25Ainda não há avaliações

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- Chapter 27 Section 27.1Documento20 páginasChapter 27 Section 27.1alejandroAinda não há avaliações

- Price Elasticity of DemandDocumento4 páginasPrice Elasticity of DemandMADmanTalksAinda não há avaliações

- Makeover of Britannia: A Path Less TravelledDocumento8 páginasMakeover of Britannia: A Path Less TravelledSnehal BhattAinda não há avaliações

- The Impact of Inflation On The Students and Staff at South East Asia Institute of Trade and Technnology Legazpi 1Documento19 páginasThe Impact of Inflation On The Students and Staff at South East Asia Institute of Trade and Technnology Legazpi 1cathleenAinda não há avaliações

- The Lean Canvas: Problem Solution Unique Value Prop. Unfair Advantage Customer SegmentsDocumento7 páginasThe Lean Canvas: Problem Solution Unique Value Prop. Unfair Advantage Customer SegmentsPrianurita QuirogaAinda não há avaliações

- Munehisa Homma - The Father of Price Action TradingDocumento6 páginasMunehisa Homma - The Father of Price Action TradingJohan HallatuAinda não há avaliações

- Summer Training Report ON Acc Cement Pvt. LTD.: SESSION (2017-2018) Career Point University Hamirpur (Himachal Pradesh)Documento15 páginasSummer Training Report ON Acc Cement Pvt. LTD.: SESSION (2017-2018) Career Point University Hamirpur (Himachal Pradesh)lucasAinda não há avaliações

- Service Tax: Aiaims Mms-ADocumento31 páginasService Tax: Aiaims Mms-AAbbas Haider NaqviAinda não há avaliações