Você também pode gostar

- Draft Scope Riverhead Logistics CenterDocumento20 páginasDraft Scope Riverhead Logistics CenterRiverheadLOCALAinda não há avaliações

- Kenneth RothwellDocumento5 páginasKenneth RothwellRiverheadLOCALAinda não há avaliações

- RXR/GGV Qualified & Eligible Documents (Final 09.26.22)Documento23 páginasRXR/GGV Qualified & Eligible Documents (Final 09.26.22)RiverheadLOCALAinda não há avaliações

- Riverhead Town Proposed Battery Energy Storage CodeDocumento10 páginasRiverhead Town Proposed Battery Energy Storage CodeRiverheadLOCALAinda não há avaliações

- Robert E. KernDocumento3 páginasRobert E. KernRiverheadLOCALAinda não há avaliações

- Riverhead Town Board Comprehensive Plan Status Discussion Feb. 17, 2022Documento30 páginasRiverhead Town Board Comprehensive Plan Status Discussion Feb. 17, 2022RiverheadLOCALAinda não há avaliações

- N.Y. Downtown Revitalization Initiative Round Five GuidebookDocumento38 páginasN.Y. Downtown Revitalization Initiative Round Five GuidebookRiverheadLOCALAinda não há avaliações

- 5-10-2022 Budget Hearing Presentation UpdatedDocumento12 páginas5-10-2022 Budget Hearing Presentation UpdatedRiverheadLOCALAinda não há avaliações

- Riverhead Budget Presentation March 22, 2022Documento14 páginasRiverhead Budget Presentation March 22, 2022RiverheadLOCALAinda não há avaliações

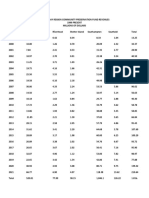

- Peconic Bay Region Community Preservation Fund Revenues 1999-2021Documento1 páginaPeconic Bay Region Community Preservation Fund Revenues 1999-2021RiverheadLOCALAinda não há avaliações

- AKRF Public Outreach Report AttachmentsDocumento126 páginasAKRF Public Outreach Report AttachmentsRiverheadLOCALAinda não há avaliações

- Juan Micieli-MartinezDocumento3 páginasJuan Micieli-MartinezRiverheadLOCALAinda não há avaliações

- 2022 - 03 - 16 - EPCAL Resolution & Letter AgreementDocumento9 páginas2022 - 03 - 16 - EPCAL Resolution & Letter AgreementRiverheadLOCALAinda não há avaliações

- Riverhead Comprehensive Plan Update Public Outreach Compendium Feb 16, 2022Documento7 páginasRiverhead Comprehensive Plan Update Public Outreach Compendium Feb 16, 2022RiverheadLOCALAinda não há avaliações

- Pediatric Covid-19 Hospitalization ReportDocumento15 páginasPediatric Covid-19 Hospitalization ReportKevin TamponeAinda não há avaliações

- Yvette AguiarDocumento10 páginasYvette AguiarRiverheadLOCALAinda não há avaliações

- Riverhead Town Police Monthly Report July 2021Documento6 páginasRiverhead Town Police Monthly Report July 2021RiverheadLOCALAinda não há avaliações

- Catherine KentDocumento7 páginasCatherine KentRiverheadLOCALAinda não há avaliações

- Riverhead Town Police Report, March 2021Documento6 páginasRiverhead Town Police Report, March 2021RiverheadLOCALAinda não há avaliações

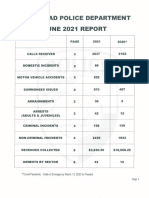

- Riverhead Town Police Monthly Report, June 2021Documento6 páginasRiverhead Town Police Monthly Report, June 2021RiverheadLOCALAinda não há avaliações

- 2021 General Election - Suffolk County Sample Ballot BookletDocumento154 páginas2021 General Election - Suffolk County Sample Ballot BookletRiverheadLOCALAinda não há avaliações

- Evelyn Hobson-Womack Campaign Finance DisclosureDocumento3 páginasEvelyn Hobson-Womack Campaign Finance DisclosureRiverheadLOCALAinda não há avaliações

- League of Women Voters of NYS 2021 Voters Guide: Ballot PropositionsDocumento2 páginasLeague of Women Voters of NYS 2021 Voters Guide: Ballot PropositionsRiverheadLOCAL67% (3)

- Riverhead Town Police Report, January 2021Documento6 páginasRiverhead Town Police Report, January 2021RiverheadLOCALAinda não há avaliações

- Aguiar-Kent Campaign Finance Report 32-Day Pre GeneralDocumento2 páginasAguiar-Kent Campaign Finance Report 32-Day Pre GeneralRiverheadLOCALAinda não há avaliações

- Riverhead Town Police Report, August 2021Documento6 páginasRiverhead Town Police Report, August 2021RiverheadLOCALAinda não há avaliações

- Old Steeple Church Time CapsuleDocumento4 páginasOld Steeple Church Time CapsuleRiverheadLOCALAinda não há avaliações

- "The Case of The DIsappering Landfill, or To Mine or Not To Mine" by Carl E. Fritz JR., PEDocumento10 páginas"The Case of The DIsappering Landfill, or To Mine or Not To Mine" by Carl E. Fritz JR., PERiverheadLOCALAinda não há avaliações

- NYSED Health and Safety Guide For The 2021 2022 School YearDocumento21 páginasNYSED Health and Safety Guide For The 2021 2022 School YearNewsChannel 9100% (2)

- Navy Environmental Concerns Survey For CalvertonDocumento3 páginasNavy Environmental Concerns Survey For CalvertonRiverheadLOCALAinda não há avaliações

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (399)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (265)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (119)

- VLCC Profit Loss 2012 PDFDocumento45 páginasVLCC Profit Loss 2012 PDFAnkit SinghalAinda não há avaliações

- Quiz Gen Math AnnuitiesDocumento1 páginaQuiz Gen Math AnnuitiesAnalyn Briones100% (2)

- Financial EngineeringDocumento26 páginasFinancial EngineeringjuhikohliAinda não há avaliações

- How To Get Started in Property DevelopmentDocumento42 páginasHow To Get Started in Property DevelopmentBrett Coombs100% (1)

- FRM 2022 Learning ObjectivesDocumento70 páginasFRM 2022 Learning ObjectivesPreeti KumariAinda não há avaliações

- 22049896 - Presentation Submission for session 11 - Nguyễn Hữu Minh TuấnDocumento11 páginas22049896 - Presentation Submission for session 11 - Nguyễn Hữu Minh TuấnTuấn NguyễnAinda não há avaliações

- FAR05Documento5 páginasFAR05Mitchie FaustinoAinda não há avaliações

- ObliCon Case Digests - Amber Gagajena PDFDocumento96 páginasObliCon Case Digests - Amber Gagajena PDFNowell SimAinda não há avaliações

- 2003 Bosi-Giarda-Onofri OverviewBudgetPolicy WPDocumento22 páginas2003 Bosi-Giarda-Onofri OverviewBudgetPolicy WPAntonio Annicchiarico RenoAinda não há avaliações

- Financial Management Key TermsDocumento36 páginasFinancial Management Key TermsMurli SavitaAinda não há avaliações

- Chapter 2 Macro SolutionDocumento16 páginasChapter 2 Macro Solutionsaurabhsaurs80% (10)

- Accounting With Ifrs Essentials An Asia Edition 1St Edition Full ChapterDocumento32 páginasAccounting With Ifrs Essentials An Asia Edition 1St Edition Full Chaptergloria.goodwin463100% (20)

- 0455 w17 QP 11Documento12 páginas0455 w17 QP 11Priya AngelAinda não há avaliações

- Sinking Fund MethodDocumento4 páginasSinking Fund MethodDianne Aicie ArellanoAinda não há avaliações

- Jacqueline Ponce de Leon A Descendent of Juan Ponce deDocumento1 páginaJacqueline Ponce de Leon A Descendent of Juan Ponce deMuhammad ShahidAinda não há avaliações

- New-ListingDocumento1 páginaNew-ListingTeam BouddhaAinda não há avaliações

- MOD1 Capital MarketDocumento17 páginasMOD1 Capital MarketMAGSINO, ANGELINE S.Ainda não há avaliações

- CSXDocumento130 páginasCSXmarcelluxAinda não há avaliações

- State Finances in Haryana - Manju DalalDocumento26 páginasState Finances in Haryana - Manju Dalalvoldemort1989Ainda não há avaliações

- FIN3103 ExamDocumento20 páginasFIN3103 ExamKevin YeoAinda não há avaliações

- Memorandum of UCC-8 and Book EntryDocumento108 páginasMemorandum of UCC-8 and Book EntrySylvester Moore100% (1)

- 8th Maths Chapter 8Documento25 páginas8th Maths Chapter 8Ankita PattnaikAinda não há avaliações

- Valuation of CollateralDocumento24 páginasValuation of CollateralLuningning Carios100% (1)

- Demand and Supply - Concepts and Applications (2) (1) (Compatibility Mode)Documento11 páginasDemand and Supply - Concepts and Applications (2) (1) (Compatibility Mode)Aminul Islam AminAinda não há avaliações

- 2021 Carlyle Investor Day PresentationDocumento229 páginas2021 Carlyle Investor Day PresentationJay ZAinda não há avaliações

- Chapter 7 (II) - Current Asset ManagementDocumento23 páginasChapter 7 (II) - Current Asset ManagementhendraxyzxyzAinda não há avaliações

- Other Annuity TypesDocumento7 páginasOther Annuity TypesLevi John Corpin AmadorAinda não há avaliações

- Pre Closestatement PDFDocumento2 páginasPre Closestatement PDFashokgiri6Ainda não há avaliações

- Fundamentals of Investing: Fourteenth Edition, Global EditionDocumento47 páginasFundamentals of Investing: Fourteenth Edition, Global EditionFreed DragsAinda não há avaliações