Você também pode gostar

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- For Zomato Limited (Formerly Known As Zomato Private Limited and Zomato Media Private Limited)Documento1 páginaFor Zomato Limited (Formerly Known As Zomato Private Limited and Zomato Media Private Limited)Info Loaded100% (1)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5795)

- Benefits of Wage Earner, Taxable and Non-Taxable BenefitsDocumento33 páginasBenefits of Wage Earner, Taxable and Non-Taxable BenefitsCassandra Dianne Ferolino MacadoAinda não há avaliações

- Delivery Challan/ Tax InvoiceDocumento2 páginasDelivery Challan/ Tax InvoiceshaikhAinda não há avaliações

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- Cir vs. FilinvestDocumento4 páginasCir vs. FilinvestAlphaZuluAinda não há avaliações

- Form 16 ExcelDocumento2 páginasForm 16 Excelapi-372756271% (7)

- Narayana Group of Schools: Bill of Supply OriginalDocumento1 páginaNarayana Group of Schools: Bill of Supply OriginalSk NurhasanAinda não há avaliações

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- CH 2Documento29 páginasCH 2syahirahAinda não há avaliações

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- Voylite Labs Private LimitedDocumento1 páginaVoylite Labs Private LimitedSunil PatelAinda não há avaliações

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Activity and Tutorial 1,2,3Documento4 páginasActivity and Tutorial 1,2,3NUR AFFIDAH LEEAinda não há avaliações

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

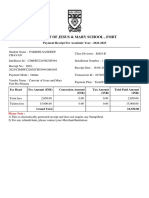

- Convent of Jesus & Mary School, Fort: Payment Receipt For Academic Year - 2022-2023Documento2 páginasConvent of Jesus & Mary School, Fort: Payment Receipt For Academic Year - 2022-2023KDAinda não há avaliações

- E-Way Bill: Government of IndiaDocumento1 páginaE-Way Bill: Government of IndiaAbdul WajidAinda não há avaliações

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (345)

- SBN-0270: Capital Gains Tax and Documentary Stamp Tax Exemption For Expropriated LandsDocumento4 páginasSBN-0270: Capital Gains Tax and Documentary Stamp Tax Exemption For Expropriated LandsRalph RectoAinda não há avaliações

- Take Home Exercise No 6 - Source of Profits (2023S)Documento3 páginasTake Home Exercise No 6 - Source of Profits (2023S)何健珩Ainda não há avaliações

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- تقرير فحص ضريبيDocumento3 páginasتقرير فحص ضريبيSmart Certified Translation ServicesAinda não há avaliações

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- FABM2Documento27 páginasFABM2Shai Rose Jumawan QuiboAinda não há avaliações

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- Tax Exemption & ConcessionDocumento1 páginaTax Exemption & Concessionßïshñü PhüyãlAinda não há avaliações

- Pascual v. CIR (Estember 3B)Documento2 páginasPascual v. CIR (Estember 3B)MasterboleroAinda não há avaliações

- Onett Developer TemplateDocumento6 páginasOnett Developer Templatejoeye louieAinda não há avaliações

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- Vanik Education PVT LTD: GSTIN - 21AAFCV2531H1ZQDocumento1 páginaVanik Education PVT LTD: GSTIN - 21AAFCV2531H1ZQNRUSINGHA PATRAAinda não há avaliações

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- Aacpt8112a 2021 110889938Documento77 páginasAacpt8112a 2021 110889938vnpAinda não há avaliações

- W-8ben For CDN Beachbody Coaches SampleDocumento1 páginaW-8ben For CDN Beachbody Coaches Sampleapi-295933330Ainda não há avaliações

- Hax To Save Tax Income Tax Calculator by Labour Law AdvisorDocumento15 páginasHax To Save Tax Income Tax Calculator by Labour Law AdvisorponmaniAinda não há avaliações

- HFMDocumento1 páginaHFMJPAinda não há avaliações

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- Invoice of EarphonesDocumento1 páginaInvoice of EarphonesSai TejaAinda não há avaliações

- Calculation of Total Tax Incidence (TTI) For ImportDocumento4 páginasCalculation of Total Tax Incidence (TTI) For ImportMd. Mehedi Hasan AnikAinda não há avaliações

- RentoMojo - Start Renting - Furniture, Appliances, Electronics (2) 1Documento2 páginasRentoMojo - Start Renting - Furniture, Appliances, Electronics (2) 1Trilok AshpalAinda não há avaliações

- HDFC FD PDFDocumento2 páginasHDFC FD PDFghesiaAinda não há avaliações

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- Abrpb4480f 2020-21Documento2 páginasAbrpb4480f 2020-21Subray N BanaulikarAinda não há avaliações

- PSNT of MFSDocumento8 páginasPSNT of MFSPayal ParmarAinda não há avaliações

- Chart of AccountsDocumento3 páginasChart of AccountsOzioma Ihekwoaba0% (1)