Você também pode gostar

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (894)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Problems - Income TaxationDocumento4 páginasProblems - Income Taxationpedrosagucio44% (9)

- Aicpa Rel Questionss Far 2015Documento33 páginasAicpa Rel Questionss Far 2015soej1004100% (4)

- New Heritage Doll CompanyDocumento5 páginasNew Heritage Doll CompanyAnonymous xJLJ4CKAinda não há avaliações

- Main SOCE Forms 1 2 3 SheetsDocumento3 páginasMain SOCE Forms 1 2 3 SheetsJohn Rey Villafuerte88% (8)

- Ohada Accounting PlanDocumento72 páginasOhada Accounting PlanNchendeh Christian100% (3)

- P&L StatementDocumento2 páginasP&L StatementiPakistan100% (8)

- Professionalism Skills For Workplace Success 3rd Edition Anderson Test BankDocumento12 páginasProfessionalism Skills For Workplace Success 3rd Edition Anderson Test BankMichaelGarciamwpge100% (18)

- Accounting as an Information SystemDocumento9 páginasAccounting as an Information SystemDyvine100% (1)

- IT Question Paper of EPBM 13Documento2 páginasIT Question Paper of EPBM 13Pravin KohaleAinda não há avaliações

- MMIDocumento5 páginasMMISreekanth NagloorAinda não há avaliações

- EPBM 8 IT Q PaperDocumento10 páginasEPBM 8 IT Q PaperBhaskar BasakAinda não há avaliações

- EPBM 14 IT Q PaperDocumento3 páginasEPBM 14 IT Q PaperBhaskar Basak100% (1)

- EPBM 7 Micro Q PaperDocumento6 páginasEPBM 7 Micro Q PaperBhaskar BasakAinda não há avaliações

- Cost Acc EPBM 11 Q PaperDocumento4 páginasCost Acc EPBM 11 Q PaperBhaskar BasakAinda não há avaliações

- Indian Institute of Management Calcutta Epbm-Vi, Vii 'End Term Examination, 2007 Operations ManagementDocumento11 páginasIndian Institute of Management Calcutta Epbm-Vi, Vii 'End Term Examination, 2007 Operations ManagementBhaskar BasakAinda não há avaliações

- Om Epbm 9Documento5 páginasOm Epbm 9Bhaskar Basak100% (1)

- Om Epbm 8Documento6 páginasOm Epbm 8Bhaskar Basak100% (1)

- Cost Acc EPBM 3 Q PaperDocumento1 páginaCost Acc EPBM 3 Q PaperBhaskar BasakAinda não há avaliações

- Epbm VDocumento5 páginasEpbm VChandan KumarAinda não há avaliações

- HRM EPBM 14 Q PaperDocumento4 páginasHRM EPBM 14 Q PaperBhaskar Basak33% (3)

- Cost Acc EPBM 4 Q PaperDocumento2 páginasCost Acc EPBM 4 Q PaperBhaskar BasakAinda não há avaliações

- EPBM 2 MM1 Q PaperDocumento5 páginasEPBM 2 MM1 Q PaperBhaskar BasakAinda não há avaliações

- Micro Course Outline RevisedDocumento3 páginasMicro Course Outline RevisedBhaskar BasakAinda não há avaliações

- EPBM 5 Micro Q PaperDocumento5 páginasEPBM 5 Micro Q PaperBhaskar BasakAinda não há avaliações

- EPBM 7 BS 1 Q PapersDocumento11 páginasEPBM 7 BS 1 Q PapersBhaskar BasakAinda não há avaliações

- EPBM 4 Micro Q PaperDocumento5 páginasEPBM 4 Micro Q PaperBhaskar Basak100% (1)

- EPBM 5 BS 1 Q PaperDocumento8 páginasEPBM 5 BS 1 Q PaperSaikat PanAinda não há avaliações

- HRM Q Paper Image FilesDocumento4 páginasHRM Q Paper Image FilesBhaskar BasakAinda não há avaliações

- HRM Epbm 6-7 Q - PaperDocumento5 páginasHRM Epbm 6-7 Q - PaperBhaskar BasakAinda não há avaliações

- EPBM 4 BS 1 Q PaperDocumento8 páginasEPBM 4 BS 1 Q PaperBhaskar BasakAinda não há avaliações

- EPBM 5 FA QuestionDocumento6 páginasEPBM 5 FA QuestionBhaskar BasakAinda não há avaliações

- DMCIHI - 030 SEC Form 20-IS - Definitive Info Statement - April 6 PDFDocumento315 páginasDMCIHI - 030 SEC Form 20-IS - Definitive Info Statement - April 6 PDFgilbert213Ainda não há avaliações

- Intern Ship ProjectDocumento75 páginasIntern Ship Projecttarun nemalipuriAinda não há avaliações

- Chapter07 XlssolDocumento49 páginasChapter07 XlssolEkhlas AmmariAinda não há avaliações

- Lesson 6 Tax Planning With Reference To Specific Magement DecisionDocumento49 páginasLesson 6 Tax Planning With Reference To Specific Magement DecisionkelvinAinda não há avaliações

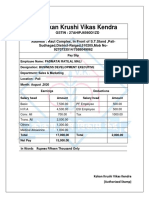

- Kokan Krushi Vikas Kendra pay slipsDocumento3 páginasKokan Krushi Vikas Kendra pay slipsDevenAinda não há avaliações

- AF210 ASSIGMENTDocumento14 páginasAF210 ASSIGMENTdiristiAinda não há avaliações

- L5 - ABFA1173 POA (Lecturer)Documento6 páginasL5 - ABFA1173 POA (Lecturer)Tan SiewsiewAinda não há avaliações

- The Business Plan WorksheetDocumento13 páginasThe Business Plan WorksheetMadduma, Jeromie G.Ainda não há avaliações

- ACC 577 Week 1 QuizDocumento8 páginasACC 577 Week 1 QuizMaryAinda não há avaliações

- Central Bay Reclamation and Dev. Corp. vs. COA and PRADocumento14 páginasCentral Bay Reclamation and Dev. Corp. vs. COA and PRAsamantha.makayan.abAinda não há avaliações

- Knowledge ReportDocumento15 páginasKnowledge ReportarsenalmanikandanAinda não há avaliações

- EC - Lecture 001 - Principles of Engineering EconomicsDocumento8 páginasEC - Lecture 001 - Principles of Engineering EconomicsDIANNEMICHELLE PINEDAAinda não há avaliações

- 19541journal Feb2009Documento167 páginas19541journal Feb2009Divya SrikanthAinda não há avaliações

- Garlic & Ginger Paste Project ProfilesDocumento7 páginasGarlic & Ginger Paste Project ProfilesArshad SheikAinda não há avaliações

- Crispynach Business PlanDocumento47 páginasCrispynach Business PlanBaby PinkAinda não há avaliações

- Mindtree Shareholders Report Q2 FY23Documento6 páginasMindtree Shareholders Report Q2 FY23Punith DGAinda não há avaliações

- Lego Group Annual Report 2015Documento72 páginasLego Group Annual Report 2015Josue Teni BeltetonAinda não há avaliações

- Nguyễn Minh Nhật KNC03 31221024307 P1.2LO 45Documento4 páginasNguyễn Minh Nhật KNC03 31221024307 P1.2LO 45Bảo KhangAinda não há avaliações

- Ch09 PDFDocumento37 páginasCh09 PDFAsh1Ainda não há avaliações

- Anaysis of Financial Statement of U.P.C.LDocumento73 páginasAnaysis of Financial Statement of U.P.C.Lmo_hit123Ainda não há avaliações

- Accounting ProjectDocumento36 páginasAccounting ProjectNin QetelauriAinda não há avaliações

- Income tax deductions under 40 charsDocumento4 páginasIncome tax deductions under 40 charsAgie MarquezAinda não há avaliações