Você também pode gostar

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (399)

- 46633bosfnd p2 Seca cp1 U1Documento3 páginas46633bosfnd p2 Seca cp1 U1Dinesh TiwariAinda não há avaliações

- 54803bos43938cp1 U1 PDFDocumento27 páginas54803bos43938cp1 U1 PDFJAIAinda não há avaliações

- Annexure IDocumento1 páginaAnnexure IKARTIK MAHAJANAinda não há avaliações

- Passport Photo and Application for Verification of DocumentsDocumento2 páginasPassport Photo and Application for Verification of DocumentsDinesh TiwariAinda não há avaliações

- APPLICATION FORM PROVISIONAL CERTIFICATEDocumento2 páginasAPPLICATION FORM PROVISIONAL CERTIFICATEDinesh TiwariAinda não há avaliações

- List of Law Colleges Having Approval by The BCIDocumento1 páginaList of Law Colleges Having Approval by The BCIDinesh TiwariAinda não há avaliações

- Consumer ProtectionDocumento20 páginasConsumer ProtectionGuddisurya FanclubAinda não há avaliações

- 2015 Case 6 MBUDocumento1 página2015 Case 6 MBUDinesh TiwariAinda não há avaliações

- 2015 Case 6 MBUDocumento12 páginas2015 Case 6 MBUDinesh TiwariAinda não há avaliações

- Human Rights Module Provides Concise OverviewDocumento10 páginasHuman Rights Module Provides Concise OverviewDinesh TiwariAinda não há avaliações

- Human Rights Module Provides Concise OverviewDocumento10 páginasHuman Rights Module Provides Concise OverviewDinesh TiwariAinda não há avaliações

- List of Law Colleges Having Approval by The BCIDocumento57 páginasList of Law Colleges Having Approval by The BCIDinesh TiwariAinda não há avaliações

- Status of Law Colleges Bar Council of IndiaDocumento71 páginasStatus of Law Colleges Bar Council of IndiaAvinash YAinda não há avaliações

- 2015 Case 6 MBUDocumento12 páginas2015 Case 6 MBUDinesh TiwariAinda não há avaliações

- Status of Law Colleges Bar Council of IndiaDocumento71 páginasStatus of Law Colleges Bar Council of IndiaAvinash YAinda não há avaliações

- List of Law Colleges Having Approval by The BCIDocumento57 páginasList of Law Colleges Having Approval by The BCIDinesh TiwariAinda não há avaliações

- General and Commercial Short NotesDocumento21 páginasGeneral and Commercial Short Notesshweta_namaya11Ainda não há avaliações

- List of Law Colleges Having Approval by The BCIDocumento57 páginasList of Law Colleges Having Approval by The BCIDinesh TiwariAinda não há avaliações

- Diff Types Companies 2012Documento5 páginasDiff Types Companies 2012Dinesh TiwariAinda não há avaliações

- Dip Fin TallyDocumento73 páginasDip Fin Tallyceasor007100% (1)

- Preliminary Examination Paper IASDocumento3 páginasPreliminary Examination Paper IASDinesh TiwariAinda não há avaliações

- Accounting For Share CapitalDocumento72 páginasAccounting For Share CapitalApollo Institute of Hospital Administration100% (5)

- Icsi Directory of Extension of Epabx Lines LDocumento8 páginasIcsi Directory of Extension of Epabx Lines LDinesh TiwariAinda não há avaliações

- Buy Back of Shares ExplainedDocumento31 páginasBuy Back of Shares ExplainedRamya NairAinda não há avaliações

- Company Secretary Job Is Very Demanding and From The Current Economic Scenario It Is The Most Worthy PositionDocumento1 páginaCompany Secretary Job Is Very Demanding and From The Current Economic Scenario It Is The Most Worthy PositionDinesh TiwariAinda não há avaliações

- Sangeet KediaDocumento1 páginaSangeet KediaDinesh TiwariAinda não há avaliações

- Civil Service India History-2005Documento19 páginasCivil Service India History-2005Subrahmanyam SripadaAinda não há avaliações

- Inflation-Linked Bonds: How They Protect Against Rising PricesDocumento1 páginaInflation-Linked Bonds: How They Protect Against Rising PricesDinesh TiwariAinda não há avaliações

- Office2010 KeyDocumento1 páginaOffice2010 KeyDinesh TiwariAinda não há avaliações

- List of Centres For December 2013 ExamDocumento1 páginaList of Centres For December 2013 ExamDinesh TiwariAinda não há avaliações

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (119)

- Meenu Chopra Income Tax BasicsDocumento66 páginasMeenu Chopra Income Tax BasicsRvi Mahay100% (1)

- Financial Institutions & Management Chapter 20Documento22 páginasFinancial Institutions & Management Chapter 20Dominic NguyenAinda não há avaliações

- Progjyoti Joining LetterDocumento6 páginasProgjyoti Joining LetterPorag Jyoti Neog75% (4)

- BR - PAL - HAL and PDYLDocumento2 páginasBR - PAL - HAL and PDYLZahed IbrahimAinda não há avaliações

- Working Capital ManagementDocumento56 páginasWorking Capital ManagementSahil KhanAinda não há avaliações

- GR 194201Documento7 páginasGR 194201RajkumariAinda não há avaliações

- Bank's Branch Head, 5 Others Get Life For Faking Documents To Avail Rs 1.5 Crore LoanDocumento3 páginasBank's Branch Head, 5 Others Get Life For Faking Documents To Avail Rs 1.5 Crore LoanJAGDISH GIANCHANDANIAinda não há avaliações

- Guide to the Negotiable Instruments LawDocumento13 páginasGuide to the Negotiable Instruments LawPaul Christopher PinedaAinda não há avaliações

- First United Constructors Corporation and Blue Star Construction Corporation, Petitioners, V. Bayanihan Automotive Corporation, Respondent.Documento7 páginasFirst United Constructors Corporation and Blue Star Construction Corporation, Petitioners, V. Bayanihan Automotive Corporation, Respondent.dteroseAinda não há avaliações

- Inflation & Unemploy Ment: Lecturer: Pn. Azizah Isa 1Documento50 páginasInflation & Unemploy Ment: Lecturer: Pn. Azizah Isa 1hariprem26100% (1)

- Completed Sba Form 413Documento6 páginasCompleted Sba Form 413api-568505563Ainda não há avaliações

- Workbook 3Documento69 páginasWorkbook 3Dody SuhermantoAinda não há avaliações

- 4DCA Sep11 - Regner v. Amtrust Bank - Reversed - Mortgagors Did Not Receive Notice of SaleDocumento3 páginas4DCA Sep11 - Regner v. Amtrust Bank - Reversed - Mortgagors Did Not Receive Notice of Salewinstons23110% (1)

- SLBS Opportunities - 24 Jan 2024Documento4 páginasSLBS Opportunities - 24 Jan 2024Pravin SinghAinda não há avaliações

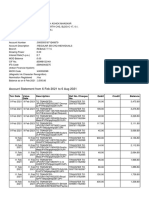

- Mr. SANTOSH ASHOK MHASKAR's account statementDocumento14 páginasMr. SANTOSH ASHOK MHASKAR's account statementSantosh MhaskarAinda não há avaliações

- Light Bill Sept 2019Documento1 páginaLight Bill Sept 2019Sanjyot KolekarAinda não há avaliações

- Chapter 6 Audit Planning Understanding The Client and AsseDocumento44 páginasChapter 6 Audit Planning Understanding The Client and Asseindra83100% (1)

- CF2012 Study Guide SolutionsDocumento11 páginasCF2012 Study Guide SolutionsDeena KhattabAinda não há avaliações

- Principal Of Budgeting: Fundamentals, Types, ComponentsDocumento6 páginasPrincipal Of Budgeting: Fundamentals, Types, ComponentsZulkarnain DahalanAinda não há avaliações

- Cost of Capital and Bond and Stock ValuationDocumento37 páginasCost of Capital and Bond and Stock Valuationzedingel100% (1)

- Surname: First Name: Campus France Registration Number: IN Age: Marital StatusDocumento2 páginasSurname: First Name: Campus France Registration Number: IN Age: Marital StatusSahil ShahAinda não há avaliações

- PercentageDocumento4 páginasPercentagesamdhathriAinda não há avaliações

- Improving settlement efficiency and mitigating risks in Hong Kong payment systemsDocumento16 páginasImproving settlement efficiency and mitigating risks in Hong Kong payment systemsSathiya RameshAinda não há avaliações

- BOOST UP PDFS - Quantitative Aptitude - SI & CI Problems (Easy Level Part-1)Documento15 páginasBOOST UP PDFS - Quantitative Aptitude - SI & CI Problems (Easy Level Part-1)ishky manoharAinda não há avaliações

- SME'sDocumento7 páginasSME'sJiezelEstebeAinda não há avaliações

- Learn investment strategiesDocumento6 páginasLearn investment strategiesAira AbigailAinda não há avaliações

- The Great Depression - Assignment # 1Documento16 páginasThe Great Depression - Assignment # 1Syed OvaisAinda não há avaliações

- I Had EnoughDocumento74 páginasI Had Enoughczabina fatima delica100% (1)

- 504b - Financial ManagementDocumento37 páginas504b - Financial ManagementHaresh Mba100% (1)