Você também pode gostar

- Study Guide - Isaca Certified in Governance of Enterprise It - Includes The Latest Practice Questions and AnswersDocumento46 páginasStudy Guide - Isaca Certified in Governance of Enterprise It - Includes The Latest Practice Questions and Answerscipioo7Ainda não há avaliações

- ACC701 Mid Exam - Question PaperDocumento5 páginasACC701 Mid Exam - Question PaperSALESHNI LALAinda não há avaliações

- Bm2009i001383850 PDFDocumento4 páginasBm2009i001383850 PDFprashant kapilAinda não há avaliações

- Landlord Tenant HandbookDocumento63 páginasLandlord Tenant Handbookrabbi_josiah100% (1)

- Index: A Study of Credit Cards in Indian ScenarioDocumento8 páginasIndex: A Study of Credit Cards in Indian Scenariorohit100% (1)

- Sub RM 502Documento77 páginasSub RM 502sohail merchantAinda não há avaliações

- Mar Jun 17 Hybrid F8 QPDocumento4 páginasMar Jun 17 Hybrid F8 QPsweet007samAinda não há avaliações

- f8 QuestionsDocumento66 páginasf8 QuestionsReem JavedAinda não há avaliações

- Auditing: Professional 1 Examination - April 2019Documento16 páginasAuditing: Professional 1 Examination - April 2019Issa BoyAinda não há avaliações

- 01 s603 MabsDocumento2 páginas01 s603 MabsMuhammad Salim Ullah KhanAinda não há avaliações

- Audit and Assurance (International) : Thursday 6 June 2013Documento6 páginasAudit and Assurance (International) : Thursday 6 June 2013Asim NazirAinda não há avaliações

- Outline 5 PDFDocumento6 páginasOutline 5 PDFfajarAinda não há avaliações

- ACC302 THEFinal A 2021 SpringDocumento5 páginasACC302 THEFinal A 2021 Springayushi kAinda não há avaliações

- 5 - (S2) Aa MP PDFDocumento3 páginas5 - (S2) Aa MP PDFFlow RiyaAinda não há avaliações

- Acct 555 - Week 1 AssignmentDocumento8 páginasAcct 555 - Week 1 AssignmentJasmine Desiree WashingtonAinda não há avaliações

- Auditing Set 2Documento7 páginasAuditing Set 2cleophacerevivalAinda não há avaliações

- Semester 1 - PAPER IDocumento7 páginasSemester 1 - PAPER IShilongo OliviaAinda não há avaliações

- Assignment (1) : B) Identify Whether Each of The Following Statements Is (True) or (False)Documento5 páginasAssignment (1) : B) Identify Whether Each of The Following Statements Is (True) or (False)Shimaa MohamedAinda não há avaliações

- Sem 5 QuesDocumento5 páginasSem 5 QuesHumayra RahmanAinda não há avaliações

- Cuac 202 AssignmentssDocumento18 páginasCuac 202 AssignmentssJoseph SimudzirayiAinda não há avaliações

- Pakistan: Time Allowed: 3 Hours Maximum Marks: 100 Roll No.Documento2 páginasPakistan: Time Allowed: 3 Hours Maximum Marks: 100 Roll No.sohail merchantAinda não há avaliações

- Audit 2023Documento18 páginasAudit 2023queenmutheu01Ainda não há avaliações

- May 2021 Professional Examinations Advanced Audit & Assurance (Paper 3.2) Chief Examiner'S Report, Questions and Marking SchemeDocumento19 páginasMay 2021 Professional Examinations Advanced Audit & Assurance (Paper 3.2) Chief Examiner'S Report, Questions and Marking SchemeVonnieAinda não há avaliações

- Chapter 2 - Tutorial SetDocumento6 páginasChapter 2 - Tutorial SetAngel Pria David LunchaAinda não há avaliações

- 304.AUDP - .L III December 2020Documento3 páginas304.AUDP - .L III December 2020Md Joinal AbedinAinda não há avaliações

- HHHHDocumento6 páginasHHHHLester Jude Del RosarioAinda não há avaliações

- Audit and Internal ReviewDocumento5 páginasAudit and Internal ReviewkhengmaiAinda não há avaliações

- GM Test Series: Top 50 QuestionsDocumento43 páginasGM Test Series: Top 50 QuestionsAryanAroraAinda não há avaliações

- 7-3-24... 4110 Both... Int-5010... Audit... QueDocumento5 páginas7-3-24... 4110 Both... Int-5010... Audit... Quenikulgauswami9033Ainda não há avaliações

- May 2018 Professional Examinations Audit & Assurance (Paper 2.3) Chief Examiner'S Report, Questions and Marking SchemeDocumento18 páginasMay 2018 Professional Examinations Audit & Assurance (Paper 2.3) Chief Examiner'S Report, Questions and Marking SchemeMahediAinda não há avaliações

- Pakistan: Time Allowed: 03 Hours Maximum Marks: 100 Roll No.Documento3 páginasPakistan: Time Allowed: 03 Hours Maximum Marks: 100 Roll No.Muhammad Zahid FaridAinda não há avaliações

- Auditing TutorialDocumento13 páginasAuditing TutorialDanisa NdhlovuAinda não há avaliações

- F1 Answers May 2013Documento15 páginasF1 Answers May 2013Chaturaka GunatilakaAinda não há avaliações

- Audit Assurance Paper 2.3Documento14 páginasAudit Assurance Paper 2.3Andrew NyumahAinda não há avaliações

- F6mys 2010 Jun QDocumento6 páginasF6mys 2010 Jun QTang Swee ChanAinda não há avaliações

- L4 Auditing Q&ADocumento23 páginasL4 Auditing Q&AChiso PhiriAinda não há avaliações

- Aa Examiner's Report March June 2022Documento26 páginasAa Examiner's Report March June 2022Saeeda ArshadAinda não há avaliações

- Audit and Assurance Int Revision Kit BPPDocumento5 páginasAudit and Assurance Int Revision Kit BPPsohail merchant100% (1)

- November 2021 Professional Examinations Advanced Audit & Assurance (Paper 3.2) Chief Examiner'S Report, Questions and Marking SchemeDocumento22 páginasNovember 2021 Professional Examinations Advanced Audit & Assurance (Paper 3.2) Chief Examiner'S Report, Questions and Marking SchemeVonnieAinda não há avaliações

- Pathfinder Peii May2010Documento148 páginasPathfinder Peii May2010Yerima AbubakarAinda não há avaliações

- Auditing The Art and Science of Assurance Engagements Canadian Twelfth Edition Canadian 12th Edition Arens Elder Test BankDocumento19 páginasAuditing The Art and Science of Assurance Engagements Canadian Twelfth Edition Canadian 12th Edition Arens Elder Test Bankalbert100% (24)

- HI6026 Final Assessment T3 2021Documento11 páginasHI6026 Final Assessment T3 2021adityapatnaik.022Ainda não há avaliações

- Cma Inter Corporate Accounts and AuditDocumento648 páginasCma Inter Corporate Accounts and Auditpari maheshwari100% (1)

- Amf 2103 Auditing & Investigations in Microfinance-1Documento4 páginasAmf 2103 Auditing & Investigations in Microfinance-1vincent ottoAinda não há avaliações

- B8af108 Audit Summer 2018 Exam PaperDocumento6 páginasB8af108 Audit Summer 2018 Exam PaperEizam Ben JetteyAinda não há avaliações

- Chap 4567 AAADocumento16 páginasChap 4567 AAAHà Phương TrầnAinda não há avaliações

- F8 RM December 2015 QuestionsDocumento14 páginasF8 RM December 2015 QuestionsatleuzhanovaAinda não há avaliações

- 1554382617CA Final Audit MCQ Booklet PDFDocumento25 páginas1554382617CA Final Audit MCQ Booklet PDFLakshay SinghAinda não há avaliações

- Ass MJ 2014Documento2 páginasAss MJ 2014Saiful IslamAinda não há avaliações

- Question and Answer - 1Documento31 páginasQuestion and Answer - 1acc-expertAinda não há avaliações

- Audit and Assurance: Diploma Stage Examination 8 June 2007Documento10 páginasAudit and Assurance: Diploma Stage Examination 8 June 2007a1000000000Ainda não há avaliações

- Implementing Audit Procedures (International Stream) : Monday 14 June 2010Documento6 páginasImplementing Audit Procedures (International Stream) : Monday 14 June 2010yaminigalAinda não há avaliações

- Fau Set 2Documento7 páginasFau Set 2BuntheaAinda não há avaliações

- Acc640 Final Project Document PDFDocumento6 páginasAcc640 Final Project Document PDFThanh Doan ThiAinda não há avaliações

- Auditing: Professional 1 Examination - April 2015Documento17 páginasAuditing: Professional 1 Examination - April 2015Issa BoyAinda não há avaliações

- MTP 12 21 Questions 1696771411Documento8 páginasMTP 12 21 Questions 1696771411harshallahotAinda não há avaliações

- 2013 S1 Tutorial - Mini Audit - Vospa LTD - QuestionsDocumento25 páginas2013 S1 Tutorial - Mini Audit - Vospa LTD - QuestionsyoAinda não há avaliações

- CAF 8 AUD Spring 2020Documento5 páginasCAF 8 AUD Spring 2020Huma BashirAinda não há avaliações

- Aud 689 Test Apr 2019 QuestionDocumento3 páginasAud 689 Test Apr 2019 QuestionHazirah GhazaliAinda não há avaliações

- QPB - Dec - 20 Mock 1 Q FinalDocumento9 páginasQPB - Dec - 20 Mock 1 Q FinalBernice Chan Wai WunAinda não há avaliações

- Cape Accounting A Literature ReviewDocumento4 páginasCape Accounting A Literature Revieweldcahvkg100% (1)

- Audit Risk Alert: Employee Benefit Plans Industry Developments, 2018No EverandAudit Risk Alert: Employee Benefit Plans Industry Developments, 2018Ainda não há avaliações

- Audit Risk Alert: General Accounting and Auditing Developments 2018/19No EverandAudit Risk Alert: General Accounting and Auditing Developments 2018/19Ainda não há avaliações

- TOP247YNDocumento52 páginasTOP247YNLaércio MatosAinda não há avaliações

- MOTO Plastic IndustriesDocumento1 páginaMOTO Plastic IndustriesAreeb BaqaiAinda não há avaliações

- In Come Tax LeaseDocumento2 páginasIn Come Tax LeaseAreeb BaqaiAinda não há avaliações

- McCosker FinalReportDocumento56 páginasMcCosker FinalReportJimmy HarvianAinda não há avaliações

- Low Speed Turbine READDocumento18 páginasLow Speed Turbine READBryan ArroyoAinda não há avaliações

- Aeorodynamics of Rotor BladesDocumento23 páginasAeorodynamics of Rotor BladesAshley_RulzzzzzzzAinda não há avaliações

- Crisis of Brain Drain in PakistanDocumento16 páginasCrisis of Brain Drain in PakistanAreeb BaqaiAinda não há avaliações

- Cost of CapitalDocumento8 páginasCost of CapitalAreeb BaqaiAinda não há avaliações

- Comp Exam1 05082k8Documento2 páginasComp Exam1 05082k8Shoaib AliAinda não há avaliações

- Cost GraphingDocumento18 páginasCost GraphingAreeb BaqaiAinda não há avaliações

- Variable and Absorption CostingDocumento3 páginasVariable and Absorption CostingAreeb Baqai100% (1)

- Chapter 7 Motivating EmployeesDocumento6 páginasChapter 7 Motivating EmployeesAreeb BaqaiAinda não há avaliações

- MM Session On Sales Force ManagementDocumento13 páginasMM Session On Sales Force ManagementAreeb BaqaiAinda não há avaliações

- Non Parametric TestDocumento15 páginasNon Parametric TestAreeb BaqaiAinda não há avaliações

- Credit Card Usage PatternDocumento3 páginasCredit Card Usage Patternak5539Ainda não há avaliações

- Nepal Rastra Bank Act 2058 2002 PDFDocumento76 páginasNepal Rastra Bank Act 2058 2002 PDFSubash PrasadAinda não há avaliações

- Suffolk Y JCC Fall 2011/ Winter 2012 Program GuideDocumento44 páginasSuffolk Y JCC Fall 2011/ Winter 2012 Program GuideSuffolkYJCCAinda não há avaliações

- Disbursement Voucher1111Documento2 páginasDisbursement Voucher1111Jocelyn Militar Amancio - DaprozaAinda não há avaliações

- Liu 2021Documento14 páginasLiu 2021Lisabet SilitongaAinda não há avaliações

- HO# (7) Chap018 Consumer Loans-, Credit Cards-And Real Estate LendingDocumento40 páginasHO# (7) Chap018 Consumer Loans-, Credit Cards-And Real Estate LendingEissa SamAinda não há avaliações

- Extra 1 Percent RatesDocumento9 páginasExtra 1 Percent RatesMinh NgọcAinda não há avaliações

- Commerce Paper2-2013Documento8 páginasCommerce Paper2-2013Zera 1402Ainda não há avaliações

- PE Assignment 15Documento4 páginasPE Assignment 15Wei Jiang HoAinda não há avaliações

- Project File On E-CommerceDocumento33 páginasProject File On E-CommerceHimanshu HAinda não há avaliações

- Avanse App Form PDFDocumento4 páginasAvanse App Form PDFSuresh DhanasekarAinda não há avaliações

- Epb 7 M ACBZ47 TSCs LDocumento8 páginasEpb 7 M ACBZ47 TSCs LSolomon PasulaAinda não há avaliações

- Ashaba Collins Internship ReportDocumento23 páginasAshaba Collins Internship ReportBonane AgnesAinda não há avaliações

- Essentials of Banking Law and PracticeDocumento31 páginasEssentials of Banking Law and PracticeAmit_PuzariAinda não há avaliações

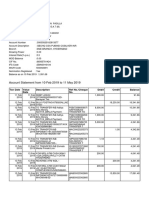

- Account Statement PDFDocumento12 páginasAccount Statement PDFAnkitAinda não há avaliações

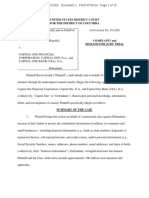

- Capital One LawsuitDocumento15 páginasCapital One LawsuitErin Fuchs100% (1)

- Fraud MagazineDocumento76 páginasFraud MagazineMaria Teresa Pedraza TenorioAinda não há avaliações

- Inbound 7745858442301742093Documento510 páginasInbound 7745858442301742093Fely EllosoAinda não há avaliações

- McKinsey Global Payments Map 2017Documento24 páginasMcKinsey Global Payments Map 2017Senka AnđelkovićAinda não há avaliações

- Iponan, Cagayan de Oro City Grade 11 Organization & ManagementDocumento3 páginasIponan, Cagayan de Oro City Grade 11 Organization & ManagementJarven SaguinAinda não há avaliações

- B105 101619525Documento7 páginasB105 101619525api-3817464Ainda não há avaliações

- BNPL Model PDFDocumento19 páginasBNPL Model PDFSunnyAinda não há avaliações

- Retail Banking - Product BrochureDocumento8 páginasRetail Banking - Product Brochurejitendra0721Ainda não há avaliações

- Interhigh - Reddam House Berkshire Limited - COA - Annual - v3 0Documento7 páginasInterhigh - Reddam House Berkshire Limited - COA - Annual - v3 0Leticia GodoyAinda não há avaliações

- Advt - No.4-2023 To 18-2023-Final - 281023Documento17 páginasAdvt - No.4-2023 To 18-2023-Final - 281023ihimanshusharma7Ainda não há avaliações

- Account Statement PDFDocumento2 páginasAccount Statement PDFfaisal rabbaniAinda não há avaliações

- Pantaleon V American ExpressDocumento25 páginasPantaleon V American ExpressPaul PsyAinda não há avaliações