Você também pode gostar

- Proposal To Lease Commercial SpaceDocumento2 páginasProposal To Lease Commercial SpaceMunashe Kombora75% (4)

- What is Financial Accounting and BookkeepingNo EverandWhat is Financial Accounting and BookkeepingNota: 4 de 5 estrelas4/5 (10)

- John Hempton Fairfax Financial V SAC Unsealed Emails & CommunicationsDocumento118 páginasJohn Hempton Fairfax Financial V SAC Unsealed Emails & CommunicationsGeronimo BobAinda não há avaliações

- Acctg 10 Midterm Lesson Part .1Documento21 páginasAcctg 10 Midterm Lesson Part .1NANAinda não há avaliações

- Accounting For Branch Operation - BakerDocumento36 páginasAccounting For Branch Operation - BakerSumon Shahariar89% (9)

- Ias 2Documento4 páginasIas 2mnhammadAinda não há avaliações

- A Study On Claims ManagementDocumento77 páginasA Study On Claims Managementarjunmba119624100% (2)

- Accounting For Branches Combined Financial Statements: ©the Mcgraw Hill Companies, Inc. 2006 Mcgraw Hill/IrwinDocumento43 páginasAccounting For Branches Combined Financial Statements: ©the Mcgraw Hill Companies, Inc. 2006 Mcgraw Hill/IrwinMarina LaurenAinda não há avaliações

- Chap 4Documento43 páginasChap 4Ramez Ahmed100% (2)

- ch4 PDFDocumento43 páginasch4 PDFAliaa HosamAinda não há avaliações

- Chapter 3Documento20 páginasChapter 3abebe kumelaAinda não há avaliações

- Advance Chapter OneDocumento15 páginasAdvance Chapter OneAhmedAinda não há avaliações

- Accounting For Branches and Combined FSDocumento112 páginasAccounting For Branches and Combined FSMuhammad Fahad100% (2)

- Adv ch-2Documento16 páginasAdv ch-2Prof. Dr. Anbalagan ChinniahAinda não há avaliações

- Chapter Two Accounting For Sales Agency and Principal Head Office and Branch 2.1. Distinction Between Sales Agency and BranchDocumento19 páginasChapter Two Accounting For Sales Agency and Principal Head Office and Branch 2.1. Distinction Between Sales Agency and Branchliyneh mebrahituAinda não há avaliações

- Advance Chapter 4Documento17 páginasAdvance Chapter 4abel habtamuAinda não há avaliações

- Accounting For Branches and Combined FSDocumento112 páginasAccounting For Branches and Combined FSEcka Tubay100% (1)

- Chapter 4Documento14 páginasChapter 4Solomon AbebeAinda não há avaliações

- Accounting For Branches and Combined FSDocumento112 páginasAccounting For Branches and Combined FSyuaningtyasnvAinda não há avaliações

- Essentials of Financial Accounting - ST (SEM 3Documento10 páginasEssentials of Financial Accounting - ST (SEM 3Harshit RajAinda não há avaliações

- Unit Two: Branch AccountingDocumento17 páginasUnit Two: Branch Accountingtemedebere100% (2)

- Accounting For Branches and Combined FSDocumento112 páginasAccounting For Branches and Combined FSAbrish MelakuAinda não há avaliações

- Appendix 1A: The Basics of Branch/Division AccountingDocumento10 páginasAppendix 1A: The Basics of Branch/Division AccountingdomingasAinda não há avaliações

- CH 12 Branch AccountingDocumento34 páginasCH 12 Branch AccountingKamel HassounAinda não há avaliações

- Chapter 3Documento40 páginasChapter 3HkAinda não há avaliações

- Branch Accountin GDocumento126 páginasBranch Accountin Gsamuel debebeAinda não há avaliações

- ADVANCE Chapter 2Documento8 páginasADVANCE Chapter 2Fasiko AsmaroAinda não há avaliações

- Chapter 4 Branch Accounting@editedDocumento18 páginasChapter 4 Branch Accounting@editedsamuel debebeAinda não há avaliações

- Agency of SaleDocumento30 páginasAgency of SaleYalew WondmnewAinda não há avaliações

- Electronic Supplement To Ch10Documento33 páginasElectronic Supplement To Ch10Ristya Rina P50% (2)

- Chapter 4 Branch AccountingDocumento31 páginasChapter 4 Branch AccountingAkkamaAinda não há avaliações

- Chapter 04 Modern Advanced AccountingDocumento31 páginasChapter 04 Modern Advanced AccountingPhoebe Lim81% (21)

- Advanced FA I&IIDocumento99 páginasAdvanced FA I&IItame kibruAinda não há avaliações

- Home Office Chap. 1Documento20 páginasHome Office Chap. 1Rei GaculaAinda não há avaliações

- Home Office & Branch Lecture NotesDocumento32 páginasHome Office & Branch Lecture NotesDrehfcieAinda não há avaliações

- A 064239896Documento12 páginasA 064239896lordaiztrandAinda não há avaliações

- Branch AccountDocumento20 páginasBranch AccountGamer BoyAinda não há avaliações

- Chapter 4 Accounting For Branches Combined Financial Statements Highlights of The Chapter PDFDocumento12 páginasChapter 4 Accounting For Branches Combined Financial Statements Highlights of The Chapter PDFCarlo VillanAinda não há avaliações

- Chapter 4 Branch AccountingDocumento17 páginasChapter 4 Branch Accountingkefyalew TAinda não há avaliações

- Branch Accounting HandoutDocumento31 páginasBranch Accounting Handoutdemeketeme2013Ainda não há avaliações

- Unit One: Branch AccountingDocumento91 páginasUnit One: Branch AccountingawlachewAinda não há avaliações

- ACC132 Home Office and Branch AccountingDocumento50 páginasACC132 Home Office and Branch AccountingAbbie Sajonia Dolleno95% (20)

- Home Branch Accounting QuzzierDocumento9 páginasHome Branch Accounting QuzzierYander Marl BautistaAinda não há avaliações

- Advance Ch2Documento127 páginasAdvance Ch2zekariyas melleseAinda não há avaliações

- Branch Accounting: D - A R I C V UDocumento25 páginasBranch Accounting: D - A R I C V UDr. Avijit RoychoudhuryAinda não há avaliações

- BUS COM NotesDocumento15 páginasBUS COM NotesJanielle NaveAinda não há avaliações

- Prelim-Quiz 1Documento6 páginasPrelim-Quiz 1Nhel AlvaroAinda não há avaliações

- Advanced FA All Chapters Teaching MaterialDocumento58 páginasAdvanced FA All Chapters Teaching MaterialKirub WerqeAinda não há avaliações

- Chapter 1 Branch Accounting LEcDocumento16 páginasChapter 1 Branch Accounting LEcDawit AmahaAinda não há avaliações

- Chapter One: Accounting For Agency &principal, Branch &head OfficeDocumento25 páginasChapter One: Accounting For Agency &principal, Branch &head OfficeDawit Amaha0% (1)

- Accounting For BranchesDocumento53 páginasAccounting For Branchesalemayehu100% (2)

- ADV I Chapter 3 2009Documento17 páginasADV I Chapter 3 2009temedebere100% (1)

- HOBO Accounting BeamsDocumento34 páginasHOBO Accounting BeamsAmr Ramadhan100% (1)

- Larsen Modern Advanced Accounting TenthDocumento43 páginasLarsen Modern Advanced Accounting TenthNoura OmaarAinda não há avaliações

- Branch AcctDocumento20 páginasBranch Acctasnfkas100% (1)

- HOBA - General Procedures-DLSAUDocumento25 páginasHOBA - General Procedures-DLSAUJasmine LimAinda não há avaliações

- Afa-Ii CH-3Documento38 páginasAfa-Ii CH-3Benol MekonnenAinda não há avaliações

- Module - Accounting For Business CombinationDocumento16 páginasModule - Accounting For Business CombinationRJ Kristine DaqueAinda não há avaliações

- Bookkeeping And Accountancy Made Simple: For Owner Managed Businesses, Students And Young EntrepreneursNo EverandBookkeeping And Accountancy Made Simple: For Owner Managed Businesses, Students And Young EntrepreneursAinda não há avaliações

- Summary of Tycho Press's Accounting for Small Business OwnersNo EverandSummary of Tycho Press's Accounting for Small Business OwnersAinda não há avaliações

- Financial Accounting - Want to Become Financial Accountant in 30 Days?No EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Nota: 5 de 5 estrelas5/5 (1)

- Your Amazing Itty Bitty® Book of QuickBooks® TerminologyNo EverandYour Amazing Itty Bitty® Book of QuickBooks® TerminologyAinda não há avaliações

- Example, Straight Line DepreciationDocumento12 páginasExample, Straight Line DepreciationKhadija Karim100% (2)

- MARSHALL 3RD BOOK - Tragics MistakesDocumento55 páginasMARSHALL 3RD BOOK - Tragics MistakesChris Pearson100% (3)

- Sohrabi 2019Documento42 páginasSohrabi 2019Brayan TillaguangoAinda não há avaliações

- Non - Life Insurance - 6Documento29 páginasNon - Life Insurance - 6Legese TusseAinda não há avaliações

- Fraud in Banking SectorDocumento30 páginasFraud in Banking SectorRavleen Kaur100% (1)

- Indian Income Tax Return Acknowledgement 2020-21: Esappo445Q Mohan Prathap PandianDocumento4 páginasIndian Income Tax Return Acknowledgement 2020-21: Esappo445Q Mohan Prathap PandianVignesh KanagarajAinda não há avaliações

- Form No. 16: Part ADocumento8 páginasForm No. 16: Part AParikshit ModiAinda não há avaliações

- Engineering Economy1Documento13 páginasEngineering Economy1Roselyn MatienzoAinda não há avaliações

- Startup Accelerator Rankings Methodology & Companion Report - Kellogg School of Management NorthwesternDocumento4 páginasStartup Accelerator Rankings Methodology & Companion Report - Kellogg School of Management NorthwesternFrank Gruber50% (2)

- Complete Annual Report 2006Documento70 páginasComplete Annual Report 2006sunny_fzAinda não há avaliações

- Special Purpose Vehicle (SPV)Documento10 páginasSpecial Purpose Vehicle (SPV)Daksh TayalAinda não há avaliações

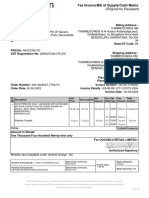

- InvoiceDocumento2 páginasInvoiceTHIMMEGOWDA H MAinda não há avaliações

- This Study Resource Was: Philippine School of Business AdministrationDocumento6 páginasThis Study Resource Was: Philippine School of Business AdministrationGab IgnacioAinda não há avaliações

- Beauhurst Crowdfunding Index Q1 2017Documento5 páginasBeauhurst Crowdfunding Index Q1 2017CrowdfundInsiderAinda não há avaliações

- 0450 m18 in 22Documento4 páginas0450 m18 in 22yoshAinda não há avaliações

- 1000 Assets: Account # Account NameDocumento24 páginas1000 Assets: Account # Account NameGomv ConsAinda não há avaliações

- Notice To Loan RepaymentDocumento2 páginasNotice To Loan RepaymentDebasish NathAinda não há avaliações

- Credit RatingDocumento24 páginasCredit RatingpsnithyaAinda não há avaliações

- Central Bank-Monetary Policy ReviewDocumento6 páginasCentral Bank-Monetary Policy ReviewAda DeranaAinda não há avaliações

- Suppose The Government Borrows 20 Billion More Next Year ThanDocumento2 páginasSuppose The Government Borrows 20 Billion More Next Year ThanMiroslav GegoskiAinda não há avaliações

- SG ITAD Ruling No. 019-03Documento4 páginasSG ITAD Ruling No. 019-03Paul Angelo TombocAinda não há avaliações

- FABS-SM-Module-04 - Internal Audit - 2021Documento54 páginasFABS-SM-Module-04 - Internal Audit - 2021pawanAinda não há avaliações

- Cash Management-Models: Baumol Model Miller-Orr Model Orgler's ModelDocumento5 páginasCash Management-Models: Baumol Model Miller-Orr Model Orgler's ModelnarayanAinda não há avaliações

- Sales Invoice: Customer InformationDocumento1 páginaSales Invoice: Customer InformationRaghavendra S DAinda não há avaliações

- Chapter 4 - AssigmentDocumento2 páginasChapter 4 - AssigmentKryzzel Anne JonAinda não há avaliações

- Actuarial Valuation LifeDocumento22 páginasActuarial Valuation Lifenitin_007100% (1)