Você também pode gostar

- Npa Analysis of DataDocumento7 páginasNpa Analysis of DataSaroj SinghAinda não há avaliações

- Main Project PDFDocumento56 páginasMain Project PDFNaira Puneet BhatiaAinda não há avaliações

- South India Surgical CompanyDocumento18 páginasSouth India Surgical CompanyDeric deric donAinda não há avaliações

- Credit Appraisal Project PinkyDocumento68 páginasCredit Appraisal Project PinkyArisha ChoudharyAinda não há avaliações

- SynopsisDocumento7 páginasSynopsisAnchalAinda não há avaliações

- Designing Capital StructureDocumento13 páginasDesigning Capital StructuresiddharthdileepkamatAinda não há avaliações

- of Icici BankDocumento32 páginasof Icici BankSandesh Kamble50% (2)

- Statutory AuditDocumento20 páginasStatutory Auditkalpesh mhatreAinda não há avaliações

- 10.methods of Cost VariabilityDocumento14 páginas10.methods of Cost VariabilityNeel Gupta100% (1)

- Tally FeaturesDocumento69 páginasTally FeaturesSudhakar Ganjikunta0% (1)

- Capstone Project Report On The Topic: Lovely Profesional UniversityDocumento70 páginasCapstone Project Report On The Topic: Lovely Profesional UniversityrajmalaleAinda não há avaliações

- Non Performing Assets in Allahabad Bank MBA Banking ProjectsDocumento68 páginasNon Performing Assets in Allahabad Bank MBA Banking Projectsmallikarjun nayak50% (2)

- Project On Bank AuditDocumento33 páginasProject On Bank AuditShubham utekarAinda não há avaliações

- Accouting, Tax Management & Audit Vouchering UNDER CA ReportDocumento95 páginasAccouting, Tax Management & Audit Vouchering UNDER CA ReportsalmanAinda não há avaliações

- Ratio Analysis Tirupati Cotton Mills LTDDocumento102 páginasRatio Analysis Tirupati Cotton Mills LTDHarish Babu Gundla PalliAinda não há avaliações

- Study On Non Performing AssetsDocumento6 páginasStudy On Non Performing AssetsHarshal RavankarAinda não há avaliações

- Pre Merger and Post Merger Position of ICICI BankDocumento44 páginasPre Merger and Post Merger Position of ICICI BankKrutika sutar0% (1)

- Assignment of Management of Working Capital: TopicDocumento13 páginasAssignment of Management of Working Capital: TopicDavinder Singh Banss0% (1)

- Capital Market in India and Identification of IndexDocumento17 páginasCapital Market in India and Identification of Indexmahesh19689Ainda não há avaliações

- Numerator and Denominator ManagementDocumento2 páginasNumerator and Denominator ManagementDisha Kushal Badlani100% (1)

- Project On Retail BankingDocumento44 páginasProject On Retail BankingabhinaykasareAinda não há avaliações

- Ekta Joshi Bajaj-AllianzDocumento56 páginasEkta Joshi Bajaj-AllianzRahul SoganiAinda não há avaliações

- Cipla Business AnalysisDocumento40 páginasCipla Business AnalysisAboli JunagadeAinda não há avaliações

- A Study On Management of Non Performing Assets in District Central Cooperative Bank PDFDocumento5 páginasA Study On Management of Non Performing Assets in District Central Cooperative Bank PDFDevikaAinda não há avaliações

- Financial Analysis - Kotak Mahindra BankDocumento43 páginasFinancial Analysis - Kotak Mahindra BankKishan ReddyAinda não há avaliações

- Exide Life Insurance Final ReportDocumento59 páginasExide Life Insurance Final ReportSahanaAinda não há avaliações

- Banking Insurance and Financial Services: Unit 1: Introduction To BANKING (25%)Documento13 páginasBanking Insurance and Financial Services: Unit 1: Introduction To BANKING (25%)sunगीत मजे्seAinda não há avaliações

- CMA Assignment-1 - Group5Documento9 páginasCMA Assignment-1 - Group5Swostik RoutAinda não há avaliações

- Dividend Theory Chap 17Documento18 páginasDividend Theory Chap 17Nihar KuchrooAinda não há avaliações

- Harpreet Singh Project Report On NPADocumento85 páginasHarpreet Singh Project Report On NPAHarpreet SinghAinda não há avaliações

- CP Damini Jyoti PDFDocumento90 páginasCP Damini Jyoti PDFjyoti dabhi100% (1)

- Bank Loan Project ReportDocumento2 páginasBank Loan Project ReportNirupa Krishna100% (1)

- Study of Trends in Quick Service Restaurants: January 2016Documento9 páginasStudy of Trends in Quick Service Restaurants: January 2016Mansi GoelAinda não há avaliações

- Problems On Hire Purchase and LeasingDocumento5 páginasProblems On Hire Purchase and Leasingprashanth mvAinda não há avaliações

- Financial Performance AnalysisDocumento106 páginasFinancial Performance AnalysisVasu GongadaAinda não há avaliações

- 7 P's of ICICI BANKDocumento13 páginas7 P's of ICICI BANKSumit VishwakarmaAinda não há avaliações

- What Is A CMA Report PDFDocumento2 páginasWhat Is A CMA Report PDFभगवा समर्थकAinda não há avaliações

- A Study On Liquidity Analysis of Tekishub Consulting ServicesDocumento14 páginasA Study On Liquidity Analysis of Tekishub Consulting ServicesTalla madhuri SreeAinda não há avaliações

- Assignment 1 PGDMDocumento6 páginasAssignment 1 PGDMMahesh Satapathy0% (1)

- AFM Question Bank For 16MBA13 SchemeDocumento10 páginasAFM Question Bank For 16MBA13 SchemeChandan Dn Gowda100% (1)

- To Study The Mergers and Acquisitions in Banking SectorDocumento42 páginasTo Study The Mergers and Acquisitions in Banking SectorAayush UpadhyayAinda não há avaliações

- A Compartive Study On Problems and Prospect of Tax System of Nepal 2016Documento98 páginasA Compartive Study On Problems and Prospect of Tax System of Nepal 2016Saroj BhusalAinda não há avaliações

- A Study On "Investment Pattern and Preference of Retail Investors" Tata Capital PVT LTDDocumento55 páginasA Study On "Investment Pattern and Preference of Retail Investors" Tata Capital PVT LTDaurorashiva1100% (1)

- Mobile Banking SynopsisDocumento4 páginasMobile Banking Synopsisujwaljaiswal33% (3)

- Gail India Ltd. ReportDocumento8 páginasGail India Ltd. Reportsakshi gulatiAinda não há avaliações

- BLACKBOOK (Standard Costing and Variance Analysis)Documento15 páginasBLACKBOOK (Standard Costing and Variance Analysis)Rashi Desai100% (1)

- Financial Statement Analysis of ICICI Bank and A Comparative Study With Axis BankDocumento7 páginasFinancial Statement Analysis of ICICI Bank and A Comparative Study With Axis Banksridharkar06100% (1)

- Financial Analysis of Crompton Greaves - R.priyaDocumento82 páginasFinancial Analysis of Crompton Greaves - R.priyaVigneshAinda não há avaliações

- Process of Issue of Commercial PapersDocumento14 páginasProcess of Issue of Commercial PapersApoorv Gupta100% (1)

- Fishbowl Inventory White PaperDocumento6 páginasFishbowl Inventory White PaperanjocargaAinda não há avaliações

- Strengths in The SWOT Analysis of ICICI BankDocumento2 páginasStrengths in The SWOT Analysis of ICICI BankSudipa RouthAinda não há avaliações

- Cians Analytics Job Description: Senior AnalystDocumento1 páginaCians Analytics Job Description: Senior Analysttanmay agrawalAinda não há avaliações

- Chapter 1 PDFDocumento20 páginasChapter 1 PDFANILAinda não há avaliações

- Final Report of Shree CmsDocumento117 páginasFinal Report of Shree CmsPuneet DagaAinda não há avaliações

- 16 - IND AS 108 - Operating Segment Final (R)Documento18 páginas16 - IND AS 108 - Operating Segment Final (R)S Bharhath kumarAinda não há avaliações

- Npa 119610079679343 5Documento46 páginasNpa 119610079679343 5Teju AshuAinda não há avaliações

- Causes of NPADocumento7 páginasCauses of NPAsggovardhan0% (1)

- Benchmarking: Practices and Tools For Achieving International Standards in Banking Sector To Overcome The Economic CrisisDocumento29 páginasBenchmarking: Practices and Tools For Achieving International Standards in Banking Sector To Overcome The Economic Crisissadik953Ainda não há avaliações

- Research Paper SampleDocumento12 páginasResearch Paper SampleVishesh SharmaAinda não há avaliações

- Perfappsys in Indian OrganizationsDocumento35 páginasPerfappsys in Indian OrganizationsStuti Sharma GaurAinda não há avaliações

- Developing Performance Standards-DRADocumento18 páginasDeveloping Performance Standards-DRAStuti Sharma GaurAinda não há avaliações

- Potential AppraisalDocumento13 páginasPotential AppraisalStuti Sharma GaurAinda não há avaliações

- NET EXAM Paper 1Documento27 páginasNET EXAM Paper 1shahid ahmed laskar100% (4)

- Ethical and Legal IssuesDocumento48 páginasEthical and Legal IssuesStuti Sharma GaurAinda não há avaliações

- Strategic Planning in Performance ManagementDocumento28 páginasStrategic Planning in Performance ManagementStuti Sharma GaurAinda não há avaliações

- Implementing Performance Management SystemDocumento20 páginasImplementing Performance Management SystemStuti Sharma GaurAinda não há avaliações

- CounselingDocumento18 páginasCounselingJithin KrishnanAinda não há avaliações

- Competency MappingDocumento12 páginasCompetency Mappingarchana2089100% (1)

- FeedbackDocumento40 páginasFeedbackStuti Sharma GaurAinda não há avaliações

- Strategic Planning in Performance ManagementDocumento28 páginasStrategic Planning in Performance ManagementStuti Sharma GaurAinda não há avaliações

- Training & Development: Training As A Management Skill / Training and Developing Your StaffDocumento36 páginasTraining & Development: Training As A Management Skill / Training and Developing Your StaffVijay AnandAinda não há avaliações

- Metrics of PerformanceDocumento42 páginasMetrics of PerformanceStuti Sharma GaurAinda não há avaliações

- Implementing Performance Management SystemDocumento20 páginasImplementing Performance Management SystemStuti Sharma GaurAinda não há avaliações

- Performance AppraisalDocumento19 páginasPerformance AppraisalStuti Sharma GaurAinda não há avaliações

- Coaching For PerformanceDocumento29 páginasCoaching For PerformanceStuti Sharma GaurAinda não há avaliações

- Coaching and MentoringDocumento7 páginasCoaching and MentoringStuti Sharma GaurAinda não há avaliações

- Job DescriptionDocumento21 páginasJob DescriptionStuti Sharma Gaur100% (1)

- Developing Performance Standards-DRADocumento18 páginasDeveloping Performance Standards-DRAStuti Sharma GaurAinda não há avaliações

- Entry Modes of International MarketDocumento118 páginasEntry Modes of International MarketStuti Sharma GaurAinda não há avaliações

- Data Mining OverviewDocumento43 páginasData Mining OverviewStuti Sharma GaurAinda não há avaliações

- Vertical 1Documento19 páginasVertical 1Stuti Sharma GaurAinda não há avaliações

- An Overview of Intellectual Property PrreeetDocumento85 páginasAn Overview of Intellectual Property PrreeetTarun SehgalAinda não há avaliações

- Role of Sme in The Economic Development of India: Prepared By:-Shaivalini Sharma Bpibs, Mba (Iiird Semester) 02911403911Documento21 páginasRole of Sme in The Economic Development of India: Prepared By:-Shaivalini Sharma Bpibs, Mba (Iiird Semester) 02911403911Hari Kishan LalAinda não há avaliações

- Tender Pricing StrategyDocumento35 páginasTender Pricing StrategyWan Hakim Wan Yaacob0% (1)

- Serv QualDocumento7 páginasServ QualVinu VijayanAinda não há avaliações

- EntrepreneurshipDocumento1 páginaEntrepreneurshipStuti Sharma GaurAinda não há avaliações

- MKTG MGMT Process FinalDocumento29 páginasMKTG MGMT Process FinalStuti Sharma GaurAinda não há avaliações

- Understanding The Target AudienceDocumento4 páginasUnderstanding The Target AudienceStuti Sharma GaurAinda não há avaliações

- Rajni Final ProjectDocumento59 páginasRajni Final Projectpuneetbansal14Ainda não há avaliações

- Estatement PDFDocumento5 páginasEstatement PDFTena Chamberlin100% (1)

- Delhi Bank People 1Documento56 páginasDelhi Bank People 1doon devbhoomi realtorsAinda não há avaliações

- Collocations With MoneyDocumento3 páginasCollocations With MoneyMariaAinda não há avaliações

- TD Business Premier Checking: Account SummaryDocumento3 páginasTD Business Premier Checking: Account SummaryJohn Bean100% (4)

- Bank Reconciliation Statement Notes-2Documento5 páginasBank Reconciliation Statement Notes-2Joel EastAinda não há avaliações

- Indian Bank Reply Notice - Advocate BalajiDocumento1 páginaIndian Bank Reply Notice - Advocate BalajiBala_999067% (3)

- PAN of All Banks in IndiaDocumento21 páginasPAN of All Banks in Indiakumar45caAinda não há avaliações

- Annexure D BG Application FormDocumento4 páginasAnnexure D BG Application FormDIPAJYOTI DEAinda não há avaliações

- RC Mapping EDCDocumento5 páginasRC Mapping EDCDhio Reza PrasetyoAinda não há avaliações

- What Is Investment BankingDocumento89 páginasWhat Is Investment BankingNarendra Chhetri100% (1)

- Chapter 7 Choosing A Source of Credit The Costs of Credit AlternativesDocumento40 páginasChapter 7 Choosing A Source of Credit The Costs of Credit Alternativesgyanprakashdeb302Ainda não há avaliações

- CBL Performance AnalysisDocumento7 páginasCBL Performance AnalysisJannatun NayeemaAinda não há avaliações

- Solution Manual For Economics of Money Banking and Financial Markets 10 e 10th Edition Frederic S MishkinDocumento7 páginasSolution Manual For Economics of Money Banking and Financial Markets 10 e 10th Edition Frederic S MishkinShirley WilliamsAinda não há avaliações

- Micro FinanceDocumento28 páginasMicro FinanceBharat Sai Kiran KAinda não há avaliações

- Standard Charge Sheet: Nabil Bank LimitedDocumento26 páginasStandard Charge Sheet: Nabil Bank LimitedAnonymous ameerAinda não há avaliações

- Foreign CurrencyDocumento4 páginasForeign CurrencyDyheeAinda não há avaliações

- Banking and Non-Banking Financial InstitutionsDocumento3 páginasBanking and Non-Banking Financial InstitutionsAbdulrauf AmeenAinda não há avaliações

- AIRTEL Tariff Guide Poster A1Documento1 páginaAIRTEL Tariff Guide Poster A1BarbaraAinda não há avaliações

- MDC Res No. 03 2012Documento2 páginasMDC Res No. 03 2012Mabuhay MuniciAinda não há avaliações

- Crystal Report Viewer 1Documento2 páginasCrystal Report Viewer 1David Lemayian SalatonAinda não há avaliações

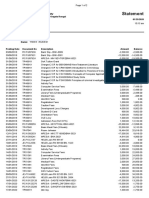

- Date Description Type of Expenses Payment Amount (CAD) Type of Expenses Actual Plan Dif % ExpensesDocumento1 páginaDate Description Type of Expenses Payment Amount (CAD) Type of Expenses Actual Plan Dif % ExpensesMarcus Vinícius SilvérioAinda não há avaliações

- Nationalization and Privatization of Commercial BanksDocumento24 páginasNationalization and Privatization of Commercial BanksAli JumaniAinda não há avaliações

- 059e848e-4e72-4cef-bc84-f78739f3f03bDocumento9 páginas059e848e-4e72-4cef-bc84-f78739f3f03bBhargavAinda não há avaliações

- DBBL StatementDocumento1 páginaDBBL StatementKazi Foyez Ahmed75% (16)

- i-DATAWORK S DetailsDocumento4 páginasi-DATAWORK S DetailssaiAinda não há avaliações

- Mba-III-strategic Credit Management (14mbafm306) - Question PaperDocumento2 páginasMba-III-strategic Credit Management (14mbafm306) - Question PaperNaren Samy100% (1)

- IFM CHDocumento53 páginasIFM CHMarIam AnsariAinda não há avaliações

- SBI Surender FormDocumento2 páginasSBI Surender FormNarayan KardileAinda não há avaliações

- Lacc Wire Transfer Acc.Documento1 páginaLacc Wire Transfer Acc.Maxim BudanAinda não há avaliações