Você também pode gostar

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5795)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (345)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- Blueprint For ProsperityDocumento31 páginasBlueprint For ProsperityNémeth Dávid100% (1)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- Foreign Market Entry StrategiesDocumento21 páginasForeign Market Entry StrategiesPrakash Kumar.s100% (4)

- W9-990 Tax Form 2016 MEDLIFE (2016-2017) PDFDocumento1 páginaW9-990 Tax Form 2016 MEDLIFE (2016-2017) PDFAnonymous 6ZE5pGAinda não há avaliações

- DRIVATIVES Options Call & Put KKDocumento134 páginasDRIVATIVES Options Call & Put KKAjay Raj ShuklaAinda não há avaliações

- Civil Procedure CasesDocumento4 páginasCivil Procedure CaseslchieSAinda não há avaliações

- Definingvalueandmeasuringhr 12997516872189 Phpapp01Documento45 páginasDefiningvalueandmeasuringhr 12997516872189 Phpapp01amizahdAinda não há avaliações

- Business Case For MDMDocumento18 páginasBusiness Case For MDMvinay10356Ainda não há avaliações

- Pool Asset ManagementDocumento10 páginasPool Asset ManagementpawanAinda não há avaliações

- Bob Iger vs. Bob Chapek - Inside The Disney Coup - WSJDocumento13 páginasBob Iger vs. Bob Chapek - Inside The Disney Coup - WSJNicolas SarkozyAinda não há avaliações

- SEBI's Role in Capital MarketDocumento57 páginasSEBI's Role in Capital MarketSagar Agarwal100% (9)

- Dipu MedicalDocumento1 páginaDipu MedicalPranjit BhuyanAinda não há avaliações

- TZBT LRQCMG ONg DwoDocumento6 páginasTZBT LRQCMG ONg DwoPranjit BhuyanAinda não há avaliações

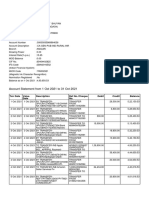

- Account Statement From 1 Nov 2021 To 30 Nov 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocumento4 páginasAccount Statement From 1 Nov 2021 To 30 Nov 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalancePranjit BhuyanAinda não há avaliações

- DiversificationDocumento2 páginasDiversificationPranjit BhuyanAinda não há avaliações

- Investment ManagementDocumento38 páginasInvestment ManagementPranjit BhuyanAinda não há avaliações

- Management Information SystemDocumento98 páginasManagement Information SystemPranjit BhuyanAinda não há avaliações

- Project ON Life Insurance Corporati ONDocumento34 páginasProject ON Life Insurance Corporati ONVirendra JhaAinda não há avaliações

- Raymond Presentation FinalDocumento23 páginasRaymond Presentation FinalAbizer KachwalaAinda não há avaliações

- 1 The Black-Scholes Formula For A European Call or Put: 1.1 Evaluation of European OptionsDocumento15 páginas1 The Black-Scholes Formula For A European Call or Put: 1.1 Evaluation of European Optionshenry37302Ainda não há avaliações

- CP Craplan ApproveDocumento50 páginasCP Craplan ApproveArchit210794Ainda não há avaliações

- NBS Bank Limited IPO Prospectus PDFDocumento119 páginasNBS Bank Limited IPO Prospectus PDFKristi DuranAinda não há avaliações

- Capital BudgetingDocumento12 páginasCapital Budgetingdebjyoti_das_6100% (1)

- Financial Management (Keshav Kasyap)Documento5 páginasFinancial Management (Keshav Kasyap)keshav kashyapAinda não há avaliações

- Ebit Eps Approach1Documento9 páginasEbit Eps Approach1Shikhar MehraAinda não há avaliações

- Group 7 - Homework Chapter 2 - Project SelectionDocumento10 páginasGroup 7 - Homework Chapter 2 - Project SelectionThuỷ VươngAinda não há avaliações

- 01 - Forex-Question BankDocumento52 páginas01 - Forex-Question BankSs DonthiAinda não há avaliações

- Ducati Realease Investindustrial 20120418Documento2 páginasDucati Realease Investindustrial 20120418cherikokAinda não há avaliações

- An Study On Commercial Banks of Ethiopia: Determinants of Nonperforming Loan: EmpiricalDocumento109 páginasAn Study On Commercial Banks of Ethiopia: Determinants of Nonperforming Loan: EmpiricalMAHLET ZEWDEAinda não há avaliações

- 07363769410070872Documento15 páginas07363769410070872Palak AgarwalAinda não há avaliações

- Notes - Chapter 4Documento6 páginasNotes - Chapter 4OneishaL.HughesAinda não há avaliações

- Governmental Entities: Introduction and General Fund AccountingDocumento99 páginasGovernmental Entities: Introduction and General Fund AccountingSamah Refa'tAinda não há avaliações

- MAHANGILA Group 2 (Tax Avenues)Documento15 páginasMAHANGILA Group 2 (Tax Avenues)Eben KinaboAinda não há avaliações

- SMCH 05Documento73 páginasSMCH 05FratFool100% (1)

- Senate Hearing, 110TH Congress - Examining The Effectiveness of U.S. Efforts To Combat Waste, Fraud, Abuse, and Corruption in IraqDocumento283 páginasSenate Hearing, 110TH Congress - Examining The Effectiveness of U.S. Efforts To Combat Waste, Fraud, Abuse, and Corruption in IraqScribd Government DocsAinda não há avaliações

- C C C !" # # $C% & #'C%Documento12 páginasC C C !" # # $C% & #'C%Sneha ShahAinda não há avaliações

- Ultratech Cement Working TemplateDocumento42 páginasUltratech Cement Working TemplateBcomE AAinda não há avaliações