Você também pode gostar

- Developing A Web-Based Information Management SystemDocumento29 páginasDeveloping A Web-Based Information Management SystemamirzieAinda não há avaliações

- QR Code Use in Smart Rooms Cleaning Management SystemDocumento4 páginasQR Code Use in Smart Rooms Cleaning Management SystemInternational Journal of Innovative Science and Research TechnologyAinda não há avaliações

- Generate BNB QR CodeDocumento1 páginaGenerate BNB QR CodeQR CryptoAinda não há avaliações

- Seminar On Automated Teller MachineDocumento15 páginasSeminar On Automated Teller MachineSaad AliAinda não há avaliações

- Spiral Model and Waterfall ModelDocumento4 páginasSpiral Model and Waterfall ModelSonakshi DasAinda não há avaliações

- Technology Chapter 1 3 1Documento21 páginasTechnology Chapter 1 3 1Marvin CincoAinda não há avaliações

- Chapter 1 Sample ThesisDocumento6 páginasChapter 1 Sample ThesisIan Ignacio AgngarayngayAinda não há avaliações

- Queuing System Using Smart Card or Barcode Technology PDF DocumentationDocumento2 páginasQueuing System Using Smart Card or Barcode Technology PDF Documentationshiellou JabongaAinda não há avaliações

- Smart RFID Based Library SystemDocumento85 páginasSmart RFID Based Library SystemsharifAinda não há avaliações

- ATM Software Testing Case StudyDocumento2 páginasATM Software Testing Case StudyDebisankar JenaAinda não há avaliações

- Android Based Enrolment SystemDocumento17 páginasAndroid Based Enrolment SystemlavanderAinda não há avaliações

- Proposal On Design and Implementation of A Computerized VISITOR MANAGEMENT SYSTEM (A Case Study of Giver'sDocumento5 páginasProposal On Design and Implementation of A Computerized VISITOR MANAGEMENT SYSTEM (A Case Study of Giver'sgolden abidemAinda não há avaliações

- BAHRIA UNIVERSITY (Karachi Campus) : Human Computer Interaction (SEN-320)Documento9 páginasBAHRIA UNIVERSITY (Karachi Campus) : Human Computer Interaction (SEN-320)Najaf NaqviAinda não há avaliações

- Fingerprint Based Patient Information SystemDocumento4 páginasFingerprint Based Patient Information SystemInternational Journal of Innovative Science and Research Technology100% (2)

- Module 5 - MainDocumento14 páginasModule 5 - MainLian qqAinda não há avaliações

- Module 08 - Basic Network ConfigurationDocumento12 páginasModule 08 - Basic Network ConfigurationĐặng Đức100% (1)

- Sfatm Chapter 2Documento16 páginasSfatm Chapter 2api-233324921Ainda não há avaliações

- Chapter 02 - Your TurnDocumento6 páginasChapter 02 - Your TurnIsaac SindigaAinda não há avaliações

- Khawajamohiuddin 2654 13637 5/HCI Assignment02Documento1 páginaKhawajamohiuddin 2654 13637 5/HCI Assignment02Khurram AliAinda não há avaliações

- Capstone DoKonsulta Pagandahan Diestro Cifra 3rd RoutingDocumento10 páginasCapstone DoKonsulta Pagandahan Diestro Cifra 3rd RoutingAlleyAinda não há avaliações

- HW6Documento26 páginasHW6Zaynab SadaAinda não há avaliações

- Banking On ATM Card Using C LanguageDocumento114 páginasBanking On ATM Card Using C LanguageDivya SmileAinda não há avaliações

- Project Proposal Template (Andriod)Documento4 páginasProject Proposal Template (Andriod)Anonymous QZxJGDymQAinda não há avaliações

- Home SecurityDocumento17 páginasHome SecurityConnie Marie MagnoAinda não há avaliações

- Introduction To Computers Module PDFDocumento218 páginasIntroduction To Computers Module PDFTinashe ChikariAinda não há avaliações

- C++ FunctionsDocumento33 páginasC++ FunctionsAlina AlinuztzaAinda não há avaliações

- ITEC54 - System Integration and Architecture - IntroductionDocumento6 páginasITEC54 - System Integration and Architecture - IntroductionRsAinda não há avaliações

- Problem Statement of Student Registration SystemDocumento1 páginaProblem Statement of Student Registration SystemPallavi BhartiAinda não há avaliações

- JSP-based Pet Adoption System: 2019 International Conference On Virtual Reality and Intelligent Systems (ICVRIS)Documento4 páginasJSP-based Pet Adoption System: 2019 International Conference On Virtual Reality and Intelligent Systems (ICVRIS)David SeptiantoAinda não há avaliações

- Thesis Chapter I - ACM FormatDocumento1 páginaThesis Chapter I - ACM FormatRyan Podiotan Adlao Sapitanan100% (1)

- Automated Patient and Doctor Handling SystemDocumento5 páginasAutomated Patient and Doctor Handling SystemInternational Journal of Innovative Science and Research Technology100% (1)

- Web-Based Requisition and Bidding SystemDocumento45 páginasWeb-Based Requisition and Bidding SystemTeremaeAinda não há avaliações

- Synopsis of The Project Proposal For School Library ManagementDocumento13 páginasSynopsis of The Project Proposal For School Library ManagementBiran Limbu100% (1)

- Desktop Application For Library Management SystemDocumento22 páginasDesktop Application For Library Management SystemharryAinda não há avaliações

- Medicine Remınder System PDFDocumento58 páginasMedicine Remınder System PDFdemirbaAinda não há avaliações

- Cynthia's Complete Project PDFDocumento61 páginasCynthia's Complete Project PDFnuelz4aAinda não há avaliações

- Online Clinic Management SystemDocumento25 páginasOnline Clinic Management SystemSUBHODIP CHOWDHURYAinda não há avaliações

- Types of Buses in Computer ArchitectureDocumento2 páginasTypes of Buses in Computer ArchitectureOMKAR KUMARAinda não há avaliações

- Passport Automation SystemDocumento5 páginasPassport Automation Systemvaagfrnds100% (1)

- A QR Code Technology For Centralized Inventory Management SystemDocumento8 páginasA QR Code Technology For Centralized Inventory Management Systemsiddhesh ghosalkarAinda não há avaliações

- Attendance Monitoring SystemDocumento4 páginasAttendance Monitoring Systemnatasha90aAinda não há avaliações

- Student Online Voting SystemDocumento8 páginasStudent Online Voting SystemGwhizz BoenAinda não há avaliações

- Dynamic QR Code: AO2000, ACF5000, ACX, EL3000, EL3060Documento10 páginasDynamic QR Code: AO2000, ACF5000, ACX, EL3000, EL3060Rajesh KumarAinda não há avaliações

- Salon de Samuel Online Reservation System 1. Background of StudyDocumento8 páginasSalon de Samuel Online Reservation System 1. Background of StudyabelAinda não há avaliações

- Label LCC For Low Context and HCC For High Context CultureDocumento2 páginasLabel LCC For Low Context and HCC For High Context CultureElsie TabangcuraAinda não há avaliações

- HDL. London: Pearson Education.: Course SyllabusDocumento2 páginasHDL. London: Pearson Education.: Course Syllabusdjun033Ainda não há avaliações

- The Role of Computer in Enhancing BankingDocumento10 páginasThe Role of Computer in Enhancing Bankinghibbuh100% (1)

- Automated System in BankingDocumento67 páginasAutomated System in BankingRaj RamAinda não há avaliações

- Cashiering System PDFDocumento8 páginasCashiering System PDFChristian David Comilang CarpioAinda não há avaliações

- Introduction To Programming 1 (JEDI)Documento289 páginasIntroduction To Programming 1 (JEDI)Erika Mae PalaciosAinda não há avaliações

- College Canteen SynopsisDocumento3 páginasCollege Canteen SynopsisPraful Bhoir100% (1)

- Ticketing SystemDocumento37 páginasTicketing SystemIsiahTanEdquiban0% (1)

- Online Counseling SystemDocumento18 páginasOnline Counseling SystemblackgatAinda não há avaliações

- Security Policy OutlineDocumento3 páginasSecurity Policy OutlinehomenetworkAinda não há avaliações

- Passport SystemDocumento42 páginasPassport Systemsssttt19930% (1)

- Application LetterDocumento6 páginasApplication LetterMcNeilRanocoPalcoAinda não há avaliações

- Automated Faculty Evaluation SystemDocumento5 páginasAutomated Faculty Evaluation SystemVeronica GavanAinda não há avaliações

- Topic: Sub: Financial Management Submitted To: Prof. Mehta: Internet BankingDocumento49 páginasTopic: Sub: Financial Management Submitted To: Prof. Mehta: Internet BankingsoniyarahateAinda não há avaliações

- T-5 Banking TechnologyDocumento18 páginasT-5 Banking TechnologyNamanAinda não há avaliações

- CH 2 - E-Banking ServicesDocumento20 páginasCH 2 - E-Banking Serviceschintan vadgamaAinda não há avaliações

- AC1101 Lesson 3 Discussion QuestionsDocumento7 páginasAC1101 Lesson 3 Discussion QuestionsMTAinda não há avaliações

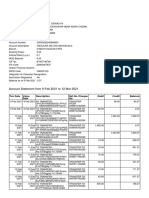

- Account Statement From 9 Feb 2021 To 12 Mar 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocumento5 páginasAccount Statement From 9 Feb 2021 To 12 Mar 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceABHINAV DEWALIYAAinda não há avaliações

- AFB-Short Notes by Murugan - Bonds (Finance) - Present ValueDocumento123 páginasAFB-Short Notes by Murugan - Bonds (Finance) - Present ValueJITENDRA KUMAR AVINASHIAinda não há avaliações

- Ampeloquio AC3 AFAR SemiFinalsDocumento11 páginasAmpeloquio AC3 AFAR SemiFinalsAmpeloquio Macky B.Ainda não há avaliações

- L1 - Bond Run 01-20-2011Documento20 páginasL1 - Bond Run 01-20-2011chinocatAinda não há avaliações

- Endorsement Schedule: LC0000000619 Intermediary Code Name M/S.Policybazaar Insurance Brokers Private LimitedDocumento1 páginaEndorsement Schedule: LC0000000619 Intermediary Code Name M/S.Policybazaar Insurance Brokers Private LimitedPrakhar ShuklaAinda não há avaliações

- Fedai Daily Quiz Questions Archives - Bank Accounts: Correct Answer: 2 Correct Answer: 2Documento22 páginasFedai Daily Quiz Questions Archives - Bank Accounts: Correct Answer: 2 Correct Answer: 2Somdutt Gujjar100% (2)

- 20012ipcc Paper5 Vol2 Cp5Documento28 páginas20012ipcc Paper5 Vol2 Cp5Muthu RamanAinda não há avaliações

- Right of Redemption and ForeclosureDocumento4 páginasRight of Redemption and ForeclosureNavaneeth NeonAinda não há avaliações

- IDFC FIRST Bank Limited Sixth Annual Report FY 2019 20Documento273 páginasIDFC FIRST Bank Limited Sixth Annual Report FY 2019 20Nihal YnAinda não há avaliações

- Finance Salary Survey 2023Documento13 páginasFinance Salary Survey 2023Goran AndreevskiAinda não há avaliações

- Indian Overseas BankDocumento3 páginasIndian Overseas Bankramarm3Ainda não há avaliações

- Abc Unit 3 PDFDocumento7 páginasAbc Unit 3 PDFLuckygirl JyothiAinda não há avaliações

- Final Year Project Chapter 2Documento5 páginasFinal Year Project Chapter 2Vincent JaiAinda não há avaliações

- Notice: Casualty and Nonperformance Certificates: Landmark Freight, Inc., Et Al.Documento2 páginasNotice: Casualty and Nonperformance Certificates: Landmark Freight, Inc., Et Al.Justia.comAinda não há avaliações

- Funda Manual Chapter 5 ExercisesDocumento8 páginasFunda Manual Chapter 5 ExercisesRimuruAinda não há avaliações

- Timelines: 4 Working Days: Consolidating Bank Account Within HDFC Bank Consolidating Bank Account - Other BankDocumento4 páginasTimelines: 4 Working Days: Consolidating Bank Account Within HDFC Bank Consolidating Bank Account - Other Bankfeel the cosmosAinda não há avaliações

- Perfomance BTW NBC and CRDB 2010Documento7 páginasPerfomance BTW NBC and CRDB 2010Moud KhalfaniAinda não há avaliações

- Hedge Fund BackersDocumento6 páginasHedge Fund Backers1c796e65b8a4c8Ainda não há avaliações

- 61089bos49694 Ipc Nov2019 gp1Documento93 páginas61089bos49694 Ipc Nov2019 gp1iswerya n.sAinda não há avaliações

- Annual Report - Norinchukin BankDocumento180 páginasAnnual Report - Norinchukin BankSenthil KumaranAinda não há avaliações

- Audit and AssuranceDocumento222 páginasAudit and AssuranceQudsia ZulfiqarAinda não há avaliações

- As Level Accounting Notes.Documento75 páginasAs Level Accounting Notes.SameerAinda não há avaliações

- Accounting For Liabilities: Learning ObjectivesDocumento39 páginasAccounting For Liabilities: Learning ObjectivesJune KooAinda não há avaliações

- Goodwill Glob Accounting For Decision Making 5.54 & 5.55 AnswerDocumento4 páginasGoodwill Glob Accounting For Decision Making 5.54 & 5.55 AnswerJay ShaunAinda não há avaliações

- Vinod Kumar Gupta Mini Project MBA 2nd SemesterDocumento95 páginasVinod Kumar Gupta Mini Project MBA 2nd SemesterVinod GuptaAinda não há avaliações

- Westpac Feb4Documento2 páginasWestpac Feb4რაქსშ საჰა100% (1)

- Role of Regional Rural Banks in The Economic Development of Rural Areas in India: A StudyDocumento11 páginasRole of Regional Rural Banks in The Economic Development of Rural Areas in India: A StudyNAGAVENIAinda não há avaliações

- Financial Analysis NestleDocumento3 páginasFinancial Analysis NestleArjun AnandAinda não há avaliações

- Final Report KasbDocumento70 páginasFinal Report KasbtrueliarerAinda não há avaliações