Você também pode gostar

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Diversification:: Chapter TitleDocumento91 páginasDiversification:: Chapter TitlefaiqsattarAinda não há avaliações

- Chapter #06 Challenge Questions Question #31 Part ADocumento4 páginasChapter #06 Challenge Questions Question #31 Part AfaiqsattarAinda não há avaliações

- Finance and The Financial Manager: Principles of Corporate FinanceDocumento10 páginasFinance and The Financial Manager: Principles of Corporate FinancefaiqsattarAinda não há avaliações

- PS1Documento5 páginasPS1faiqsattarAinda não há avaliações

- GaugesDocumento3 páginasGaugesfaiqsattarAinda não há avaliações

- Title MarketingDocumento1 páginaTitle MarketingfaiqsattarAinda não há avaliações

- Values and Their MeaningDocumento1 páginaValues and Their MeaningfaiqsattarAinda não há avaliações

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5795)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (345)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- Off-Balance Banking Activities and Risk Management For Financial InstitutionsDocumento29 páginasOff-Balance Banking Activities and Risk Management For Financial InstitutionsSahiba MaingiAinda não há avaliações

- 2Q Profits Up 24% On Strong Sales and Opex Savings: Puregold Price Club, IncDocumento7 páginas2Q Profits Up 24% On Strong Sales and Opex Savings: Puregold Price Club, Incacd1355Ainda não há avaliações

- New Book Oficial EnglishDocumento97 páginasNew Book Oficial EnglishAbolaji MuazAinda não há avaliações

- Chapter 8 Managing Transaction RisksDocumento22 páginasChapter 8 Managing Transaction Risksmatthew kobulnickAinda não há avaliações

- Methods & Orgs: Diagram of T-AccountsDocumento7 páginasMethods & Orgs: Diagram of T-AccountsZena ChiiAinda não há avaliações

- Financial Acumen - Goods & Services SampleDocumento13 páginasFinancial Acumen - Goods & Services SampleDavid M231412312100% (1)

- Euromoney Financial Training Calendar 2014Documento12 páginasEuromoney Financial Training Calendar 2014api-239673366100% (1)

- Strategic Analysis of Indian Life Insurance IndustryDocumento40 páginasStrategic Analysis of Indian Life Insurance IndustryPunit RaithathaAinda não há avaliações

- REPSOL Strategic Plan 2018Documento54 páginasREPSOL Strategic Plan 2018Adolfo BecerraAinda não há avaliações

- SNL Interactive - ArticleDocumento2 páginasSNL Interactive - ArticleAmin BisharaAinda não há avaliações

- Panache TravelDocumento33 páginasPanache TravelDevon Vernon100% (1)

- Chapter 1 To 6 Multiple Choice SolutionsDocumento44 páginasChapter 1 To 6 Multiple Choice SolutionsReenal67% (3)

- Chapter 9 Stocks and Their ValuationDocumento24 páginasChapter 9 Stocks and Their ValuationHammad KamranAinda não há avaliações

- ICAI Ready Referencer 2020Documento100 páginasICAI Ready Referencer 2020ajitAinda não há avaliações

- 12 Abm B Survey QuestionnairesDocumento2 páginas12 Abm B Survey QuestionnairesPinky Dela Cruz AballeAinda não há avaliações

- Lesson 2 Bank Discount and Promissory NoteDocumento3 páginasLesson 2 Bank Discount and Promissory NoteSERALDYN SAMSONAinda não há avaliações

- Business Unit Performance Measurement: Mcgraw-Hill/IrwinDocumento17 páginasBusiness Unit Performance Measurement: Mcgraw-Hill/Irwinimran_chaudhryAinda não há avaliações

- Sail Fundamental and TechnicalDocumento68 páginasSail Fundamental and Technicalkedar25hAinda não há avaliações

- Imt 57Documento9 páginasImt 57Pallavi VirmaniAinda não há avaliações

- EURJPY M15v PDFDocumento20 páginasEURJPY M15v PDFSafwan bin ZolkipliAinda não há avaliações

- Simple Forex StrategiesDocumento4 páginasSimple Forex Strategieszeina32Ainda não há avaliações

- Ad-As Worksheet 4Documento8 páginasAd-As Worksheet 4opdillhoAinda não há avaliações

- Ratio Calculator 1Documento10 páginasRatio Calculator 1Anahisa QuintanillaAinda não há avaliações

- Practitioner's Guide To Cost of Capital & WACC Calculation: EY Switzerland Valuation Best PracticeDocumento25 páginasPractitioner's Guide To Cost of Capital & WACC Calculation: EY Switzerland Valuation Best PracticeМаксим ЧернышевAinda não há avaliações

- Minor Research Paper FINAL 1Documento30 páginasMinor Research Paper FINAL 1Deep ChoudharyAinda não há avaliações

- 7 CMA FormatDocumento22 páginas7 CMA Formatzahoor80100% (2)

- Autobahn Insight - Equity Pre-TradeDocumento23 páginasAutobahn Insight - Equity Pre-TradePrasanth MatheshAinda não há avaliações

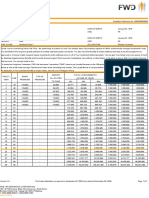

- Set For Life 7pay Sales IllustrationDocumento7 páginasSet For Life 7pay Sales IllustrationRyanAinda não há avaliações

- Multinational Financial Management 10th Edition Shapiro Solutions ManualDocumento35 páginasMultinational Financial Management 10th Edition Shapiro Solutions Manualdoughnut.synocilj084s100% (23)

- Bus - Valuation - StudentDocumento5 páginasBus - Valuation - StudentMilan TilvaAinda não há avaliações