Você também pode gostar

- Housing: Housing Finances in IndiaDocumento43 páginasHousing: Housing Finances in Indiaprasahnthrk07Ainda não há avaliações

- Housing Finance A Comparative Study of SBI and HDFC BankDocumento3 páginasHousing Finance A Comparative Study of SBI and HDFC BankEditor IJTSRDAinda não há avaliações

- In-Depth Study of Housing Finance SectorDocumento134 páginasIn-Depth Study of Housing Finance SectorSnehraj AmburleAinda não há avaliações

- Comparative Study On Housing Loans in India FinanceDocumento4 páginasComparative Study On Housing Loans in India FinanceNaresh HariyaniAinda não há avaliações

- Mine Black Book ProjectDocumento47 páginasMine Black Book ProjectHemal VyasAinda não há avaliações

- Customer Satisfaction Towards Lic Housing FinancDocumento69 páginasCustomer Satisfaction Towards Lic Housing Financboss_144569224100% (1)

- Comparative Study of Housing Loan Financial Conditions of SBI and HDFC BanksDocumento4 páginasComparative Study of Housing Loan Financial Conditions of SBI and HDFC BanksEditor IJTSRDAinda não há avaliações

- CENTRAL BANK OF INDIA PPT (Harshitha) 1Documento27 páginasCENTRAL BANK OF INDIA PPT (Harshitha) 1Harshitha Uchil0% (1)

- Fundamental Analysis of Banking Sector in IndiaDocumento17 páginasFundamental Analysis of Banking Sector in IndiaGauri BiyaniAinda não há avaliações

- Banking at HDFCDocumento68 páginasBanking at HDFCramAinda não há avaliações

- Icici Home LoansDocumento43 páginasIcici Home Loanskashyappawan007Ainda não há avaliações

- Service Quality OF HDFC BANKDocumento47 páginasService Quality OF HDFC BANKSubhendu GhoshAinda não há avaliações

- Comparative Study of Home Loans of PNB and Sbi BankDocumento113 páginasComparative Study of Home Loans of PNB and Sbi BankMakarand SatamAinda não há avaliações

- Indian Contract Act 1872Documento25 páginasIndian Contract Act 1872sjkushwaha21100% (1)

- ProjectDocumento50 páginasProjectPavan KumarAinda não há avaliações

- Final Semester Project Synopsis: Submitted To Mrs. Krunali PetkarDocumento6 páginasFinal Semester Project Synopsis: Submitted To Mrs. Krunali PetkarNitesh RajbharAinda não há avaliações

- KSFC ProjectDocumento26 páginasKSFC ProjectsrinAinda não há avaliações

- Project Report GIMDocumento66 páginasProject Report GIMVarsha ValsanAinda não há avaliações

- National Policies of HousingDocumento15 páginasNational Policies of HousingVernika Agrawal100% (1)

- Impact of FDI On Indian Economy: Term Paper On Financial SystemDocumento19 páginasImpact of FDI On Indian Economy: Term Paper On Financial SystempintuAinda não há avaliações

- Affordable Housing DossierDocumento9 páginasAffordable Housing DossierTaraAinda não há avaliações

- Dissertation Report On: Buying Behaviour For FMCGDocumento56 páginasDissertation Report On: Buying Behaviour For FMCGKrishn SharmaAinda não há avaliações

- New Non Banking Financial InstitutionsDocumento18 páginasNew Non Banking Financial InstitutionsGarima SinghAinda não há avaliações

- Credit Risk ManagementDocumento86 páginasCredit Risk ManagementSagar Paul'g100% (1)

- Indian Banking StructureDocumento5 páginasIndian Banking StructureKarthik NadarAinda não há avaliações

- SynopsisDocumento8 páginasSynopsisnehasingh121Ainda não há avaliações

- Hudco: (Housing and Urban Development Corporation)Documento18 páginasHudco: (Housing and Urban Development Corporation)Darshan BAinda não há avaliações

- An In-Depth Study of Indian Consumer Durable IndustryDocumento18 páginasAn In-Depth Study of Indian Consumer Durable Industrysaraswat2009Ainda não há avaliações

- Final Project On Mutual Funds in HDFC AmcDocumento59 páginasFinal Project On Mutual Funds in HDFC AmcSarangAgarwal100% (1)

- Standerd ChartedDocumento58 páginasStanderd ChartedashishgargAinda não há avaliações

- A Major Project ON: "Comparison of Home Loan Scheme of Different Banks"Documento81 páginasA Major Project ON: "Comparison of Home Loan Scheme of Different Banks"ganesh joshiAinda não há avaliações

- Comparative Study Between Private Sectors Bank and Public Sector BanksDocumento36 páginasComparative Study Between Private Sectors Bank and Public Sector BanksjudeAinda não há avaliações

- Presentation VishalDocumento16 páginasPresentation Vishalshubham jagtap100% (1)

- Swot & PestelDocumento4 páginasSwot & PestelUrvashi Arora100% (1)

- Indiabulls Group Presentation - 111113Documento37 páginasIndiabulls Group Presentation - 111113Ritesh VarmaAinda não há avaliações

- RRSDocumento21 páginasRRSHardik ChaudhariAinda não há avaliações

- Marwari College, Ranchi: D R - K - A - N - S H A H D E ODocumento4 páginasMarwari College, Ranchi: D R - K - A - N - S H A H D E OAshish Lakra100% (2)

- Further Scope of The Study Regarding Investment BankingDocumento3 páginasFurther Scope of The Study Regarding Investment BankingMehedi HassanAinda não há avaliações

- Pestle AnalysisDocumento3 páginasPestle AnalysisRiya SinghAinda não há avaliações

- Kotak Mahindra Bank 121121123739 Phpapp02Documento112 páginasKotak Mahindra Bank 121121123739 Phpapp02RahulSinghAinda não há avaliações

- Pradhan Mantri Awas Yojna 2019 (PMAY) प्रधानमंत्री आवास योजना - 2019 स्कीम की पूरी जानकारीDocumento20 páginasPradhan Mantri Awas Yojna 2019 (PMAY) प्रधानमंत्री आवास योजना - 2019 स्कीम की पूरी जानकारीAbinash MandilwarAinda não há avaliações

- Ankita Final Report On RDCDocumento97 páginasAnkita Final Report On RDCMayank SarpadadiyaAinda não há avaliações

- Neighbourhood ConceptDocumento7 páginasNeighbourhood ConceptSasmita GuruAinda não há avaliações

- Home LoansDocumento40 páginasHome LoansPrashant K. SinghAinda não há avaliações

- Deteriroration of StructuresDocumento11 páginasDeteriroration of StructuresArjunRathodAinda não há avaliações

- SBIDocumento26 páginasSBIsujata11Ainda não há avaliações

- Lic Housing Finance-1Documento44 páginasLic Housing Finance-1Abdul RasheedAinda não há avaliações

- Indian EconomyDocumento6 páginasIndian EconomyAzra Fatma50% (2)

- A Study On Deposit Mobilization With Reference To Indian Overseas Bank, Velachery byDocumento44 páginasA Study On Deposit Mobilization With Reference To Indian Overseas Bank, Velachery byvinoth_17588Ainda não há avaliações

- Housing Finance SystemsDocumento45 páginasHousing Finance SystemsPriyanka100% (1)

- And Long Term" Which Is Accomplished During The Training Bank of Baroda, SME LOANDocumento246 páginasAnd Long Term" Which Is Accomplished During The Training Bank of Baroda, SME LOANkanchanmbmAinda não há avaliações

- Comparative Study of Education Loan Between Sbi and IciciDocumento88 páginasComparative Study of Education Loan Between Sbi and IciciAvtaar SinghAinda não há avaliações

- Banking IndustryDocumento6 páginasBanking IndustryRaiyan KhanAinda não há avaliações

- Introduction To Indian Banking IndustryDocumento20 páginasIntroduction To Indian Banking IndustrypatilujwAinda não há avaliações

- Comprehensive Study On Financial Analysis of HDFC Bank: Prepared byDocumento38 páginasComprehensive Study On Financial Analysis of HDFC Bank: Prepared byshrutilatherAinda não há avaliações

- Shraddha ProjectDocumento70 páginasShraddha ProjectAkshay Harekar50% (2)

- Housing FinanceDocumento18 páginasHousing FinanceKaushal KumarAinda não há avaliações

- Housing Finance: Submitted By: Submitted ToDocumento20 páginasHousing Finance: Submitted By: Submitted ToAayush KoolwalAinda não há avaliações

- Top Housing Finance Companies in IndiaDocumento7 páginasTop Housing Finance Companies in Indiaboss786Ainda não há avaliações

- Housing Finance: Presented by Sulekha Beri I.D.NO .43847Documento46 páginasHousing Finance: Presented by Sulekha Beri I.D.NO .43847mehakdadwalAinda não há avaliações

- The Tata Trusts Are at The Heart of A Unique Business Model, and Custodians of A Tradition of Philanthropy That Touches and Changes Countless LivesDocumento8 páginasThe Tata Trusts Are at The Heart of A Unique Business Model, and Custodians of A Tradition of Philanthropy That Touches and Changes Countless LivesSanket AiyaAinda não há avaliações

- Telecom IndustryDocumento10 páginasTelecom IndustrySumitra MohantyAinda não há avaliações

- 2010 Govt Statistics TourismDocumento338 páginas2010 Govt Statistics TourismPragnendra RahevarAinda não há avaliações

- Cost Sheet of Laxmi Soap FactoryDocumento12 páginasCost Sheet of Laxmi Soap FactorySanket Aiya60% (5)

- Cost Sheet of Laxmi Soap FactoryDocumento12 páginasCost Sheet of Laxmi Soap FactorySanket Aiya60% (5)

- Fiscal Deficit InfoDocumento12 páginasFiscal Deficit InfoSanket AiyaAinda não há avaliações

- Fiscal Deficit InfoDocumento12 páginasFiscal Deficit InfoSanket AiyaAinda não há avaliações

- Module 4 - Week 9 - RD21 - StudentDocumento16 páginasModule 4 - Week 9 - RD21 - StudentNikku SinghAinda não há avaliações

- B&A ProfileDocumento4 páginasB&A ProfileHittMan BajgainAinda não há avaliações

- Brightwell CashPickup 33TF078444391Documento2 páginasBrightwell CashPickup 33TF078444391Edz carl AberiaAinda não há avaliações

- SOP Purchasing ManualDocumento220 páginasSOP Purchasing ManualFissha100% (1)

- Akanksha Verma - Impact of Bom On Retail Banking and Customer Satisfaction at Bank of MaharastraDocumento60 páginasAkanksha Verma - Impact of Bom On Retail Banking and Customer Satisfaction at Bank of MaharastraSTAR PRINTINGAinda não há avaliações

- Chapter 2 Healthcare Delivery and EconomicsDocumento3 páginasChapter 2 Healthcare Delivery and EconomicsTee WoodAinda não há avaliações

- Internship of Summer Training ON Study of Opd Services in A Hospital Submitted By:-Salony Saha REGISTRATION NO.:-1476020 (FROM-1 July To 31Th August)Documento14 páginasInternship of Summer Training ON Study of Opd Services in A Hospital Submitted By:-Salony Saha REGISTRATION NO.:-1476020 (FROM-1 July To 31Th August)yugalkishorAinda não há avaliações

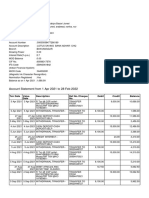

- Account Statement From 1 Apr 2021 To 28 Feb 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocumento2 páginasAccount Statement From 1 Apr 2021 To 28 Feb 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceAPPLE MARINEAinda não há avaliações

- Chapter 5&6-URGENCY & SAFETY TRANSMISSIONDocumento15 páginasChapter 5&6-URGENCY & SAFETY TRANSMISSIONmendesAinda não há avaliações

- Postcard Marketing SecretsDocumento21 páginasPostcard Marketing SecretsPrince WilliamsAinda não há avaliações

- F3 Questions Update For AFD-1Documento57 páginasF3 Questions Update For AFD-1Shahab ShafiAinda não há avaliações

- Arjun TicDocumento1 páginaArjun TicNishant RaiAinda não há avaliações

- Test I - Multiple Choice - TheoryDocumento6 páginasTest I - Multiple Choice - Theorycute meAinda não há avaliações

- Terms & Conditions - Insta Jumbo Loan: Please Note ThatDocumento3 páginasTerms & Conditions - Insta Jumbo Loan: Please Note ThatZaed QasmiAinda não há avaliações

- Qib Form DWDocumento1 páginaQib Form DWHARISHAinda não há avaliações

- 3 BBDocumento2 páginas3 BBKomgit ChantachoteAinda não há avaliações

- UNIT 5 Practice Aplication - Doc - NiDocumento11 páginasUNIT 5 Practice Aplication - Doc - NiClaire VicenteAinda não há avaliações

- Resume Rev 2Documento2 páginasResume Rev 2Kimberly HoltAinda não há avaliações

- MM-2 Presentation Digital MarketingDocumento7 páginasMM-2 Presentation Digital MarketingGypsy KingAinda não há avaliações

- Bank Promotion Exam Recollected Questions Part 8Documento15 páginasBank Promotion Exam Recollected Questions Part 8sandeepmor789Ainda não há avaliações

- Accounts Payable Interview Questions in R12Documento10 páginasAccounts Payable Interview Questions in R12Pradyumna KumarAinda não há avaliações

- Amazon Future Group CaseDocumento2 páginasAmazon Future Group CaseSurojit PaulAinda não há avaliações

- Anshul Dogra Resume-1Documento3 páginasAnshul Dogra Resume-1Rohan JiAinda não há avaliações

- (MCQ) Computer Communication Networks - LMT2Documento14 páginas(MCQ) Computer Communication Networks - LMT2raghad mejeedAinda não há avaliações

- RafDoc - A-0004824553Documento4 páginasRafDoc - A-0004824553Adilius ManualAinda não há avaliações

- The Healthcare System in GhanaDocumento1 páginaThe Healthcare System in GhanaDave UlanAinda não há avaliações

- Group 1 - International Accounting Comparative Accounting The Americas and AsiaDocumento23 páginasGroup 1 - International Accounting Comparative Accounting The Americas and AsiaAlmaliyana BasyaibanAinda não há avaliações

- tOURS & tRAVELSDocumento57 páginastOURS & tRAVELSMithun Nair M100% (1)

- Diploma in Accountancy Dec 2022 Exam Session QaDocumento219 páginasDiploma in Accountancy Dec 2022 Exam Session QaWalusungu A Lungu BandaAinda não há avaliações

- Redemption Form CoreDocumento1 páginaRedemption Form CoreJan Marie SingcaAinda não há avaliações