Você também pode gostar

- Indian Capital MarketpptDocumento40 páginasIndian Capital MarketpptShivani NidhiAinda não há avaliações

- Capital MarketDocumento39 páginasCapital MarketAjit Sarwade0% (1)

- Chapter - 2Documento91 páginasChapter - 2Chetan BagriAinda não há avaliações

- 43 Indian - Capital - MarketDocumento40 páginas43 Indian - Capital - MarketNiladri MondalAinda não há avaliações

- Indian Capital MarketDocumento40 páginasIndian Capital MarketSaurabh G100% (10)

- Indian Money Market & Capital Market: Presented byDocumento20 páginasIndian Money Market & Capital Market: Presented byManthan KulkarniAinda não há avaliações

- Capital MarketsDocumento40 páginasCapital MarketsItronix MohaliAinda não há avaliações

- Indian Capital MarketDocumento40 páginasIndian Capital MarketLoesh WaranAinda não há avaliações

- Sapm Unit 2 Part 1Documento43 páginasSapm Unit 2 Part 1Sushma KumarAinda não há avaliações

- Introduction To Financial SystemDocumento23 páginasIntroduction To Financial SystemNeeshu AgarwalAinda não há avaliações

- Introduction To Financial Institutions and Markets: - Primary MarketDocumento68 páginasIntroduction To Financial Institutions and Markets: - Primary MarketHemant GohilAinda não há avaliações

- BSEDocumento25 páginasBSEanon_35679790650% (2)

- Online Trading Services of HDFC Securities Limited: by Chitta Rama KrishnaDocumento74 páginasOnline Trading Services of HDFC Securities Limited: by Chitta Rama KrishnaChitta RamakrishnaAinda não há avaliações

- Capital Market: Overview & OperationsDocumento37 páginasCapital Market: Overview & OperationsEldho VargheseAinda não há avaliações

- Stock Exchange Reforms in India 1221566663857333 9Documento11 páginasStock Exchange Reforms in India 1221566663857333 9Jimmy MuthukattilAinda não há avaliações

- Capital MarketDocumento11 páginasCapital MarketNitin MirajkarAinda não há avaliações

- Ch.1 Money MarketDocumento32 páginasCh.1 Money MarketjaludaxAinda não há avaliações

- Impact of Reforms in Capital Market On Indian Capital MarketDocumento30 páginasImpact of Reforms in Capital Market On Indian Capital MarketNiketu Shah0% (1)

- Module 3.1 Secondary MarketDocumento54 páginasModule 3.1 Secondary MarketsateeshjorliAinda não há avaliações

- Capital Markets & Money MarketsDocumento52 páginasCapital Markets & Money Marketsynkamat100% (6)

- Indian Capital MarketDocumento19 páginasIndian Capital MarketdollieAinda não há avaliações

- Indian Fin. SystemDocumento66 páginasIndian Fin. SystemshahankeetAinda não há avaliações

- Capital MarketDocumento16 páginasCapital Marketdeepika90236100% (1)

- Stock Market - FunctionsDocumento11 páginasStock Market - FunctionsAditi KhandelwalAinda não há avaliações

- IFS Module 6Documento32 páginasIFS Module 6Akhil PrasadAinda não há avaliações

- Stock MarketDocumento29 páginasStock MarketSarabjeet Kaur Sohi0% (1)

- OF Capital Markets: by Priya Kansal Assistant Professor Jaipuria Institute of ManagementDocumento42 páginasOF Capital Markets: by Priya Kansal Assistant Professor Jaipuria Institute of ManagementBhawanath JhaAinda não há avaliações

- L5 Exchange and IndexDocumento27 páginasL5 Exchange and Indexnarendran ramanAinda não há avaliações

- Security MarketDocumento30 páginasSecurity Marketashish_k_srivastavaAinda não há avaliações

- Reforms and Recent Changes in Derivatives MarketsDocumento19 páginasReforms and Recent Changes in Derivatives MarketsprathibakbAinda não há avaliações

- Chapter 3 Securities MarketDocumento50 páginasChapter 3 Securities Marketsharktale2828100% (1)

- Original Cse 1Documento31 páginasOriginal Cse 1api-3825789100% (1)

- 5capital & Money MarketsDocumento59 páginas5capital & Money MarketsSaurav TyagiAinda não há avaliações

- Securities Market: The BattlefieldDocumento26 páginasSecurities Market: The Battlefieldpriyarajan26Ainda não há avaliações

- NSE BSE ListingDocumento33 páginasNSE BSE ListingMaithreyi JntuAinda não há avaliações

- Bombay Stockex ChangeDocumento47 páginasBombay Stockex ChangeKmdarif DoulaAinda não há avaliações

- Perfect Competition Case Study On Stock ExchangeDocumento29 páginasPerfect Competition Case Study On Stock Exchangegagan3211100% (1)

- Finance Specilization: Asst. Professors, MBA Department, Bhagawan Mahavir College of Management, SuratDocumento85 páginasFinance Specilization: Asst. Professors, MBA Department, Bhagawan Mahavir College of Management, Suratsakshirelan87Ainda não há avaliações

- Mod 4 1Documento29 páginasMod 4 1David JohnAinda não há avaliações

- Trading and Settlement ProcedureDocumento41 páginasTrading and Settlement ProcedureAshray BhandaryAinda não há avaliações

- Indian Financial SystemDocumento52 páginasIndian Financial SystemHardik ShahAinda não há avaliações

- Primary MarketDocumento25 páginasPrimary Marketkunaldaga78Ainda não há avaliações

- Synopsis Edited Seema (IGNOU)Documento11 páginasSynopsis Edited Seema (IGNOU)Ankur Chopra0% (1)

- Chapter - 1Documento12 páginasChapter - 1SsAinda não há avaliações

- Securities Market InfrastructureDocumento12 páginasSecurities Market InfrastructureMonica MercadoAinda não há avaliações

- Venkat Financial MarketsDocumento30 páginasVenkat Financial MarketsVenkat GVAinda não há avaliações

- Overview of Cambodia Securities MarketDocumento53 páginasOverview of Cambodia Securities MarketthethAinda não há avaliações

- Macro Economic Environment: Submitted byDocumento35 páginasMacro Economic Environment: Submitted byAditya YadavAinda não há avaliações

- The Indian Stock MarketDocumento47 páginasThe Indian Stock MarketManvendra ChaudharyAinda não há avaliações

- Fm302 Management+of+Financial+ServicesDocumento83 páginasFm302 Management+of+Financial+ServicesVinayrajAinda não há avaliações

- Debt Market in India - Key Issues & Policy RecommendationsDocumento17 páginasDebt Market in India - Key Issues & Policy Recommendationsreep_12Ainda não há avaliações

- The Financial System, Investing and Brief OverviewDocumento36 páginasThe Financial System, Investing and Brief OverviewshaRUKHAinda não há avaliações

- Ipology: The Science of the Initial Public OfferingNo EverandIpology: The Science of the Initial Public OfferingNota: 5 de 5 estrelas5/5 (1)

- A Practical Approach to the Study of Indian Capital MarketsNo EverandA Practical Approach to the Study of Indian Capital MarketsAinda não há avaliações

- High-Frequency Trading: A Practical Guide to Algorithmic Strategies and Trading SystemsNo EverandHigh-Frequency Trading: A Practical Guide to Algorithmic Strategies and Trading SystemsNota: 2 de 5 estrelas2/5 (1)

- Bull's Eye- A stock market investment guide for beginnersNo EverandBull's Eye- A stock market investment guide for beginnersAinda não há avaliações

- The Investment Industry for IT Practitioners: An Introductory GuideNo EverandThe Investment Industry for IT Practitioners: An Introductory GuideAinda não há avaliações

- Mastering the Market: A Comprehensive Guide to Successful Stock InvestingNo EverandMastering the Market: A Comprehensive Guide to Successful Stock InvestingAinda não há avaliações

- Elss 1 PDFDocumento26 páginasElss 1 PDFrachealllAinda não há avaliações

- Accounts of Banking CompaniesDocumento24 páginasAccounts of Banking CompaniesrachealllAinda não há avaliações

- Retail EnvironmentDocumento15 páginasRetail EnvironmentrachealllAinda não há avaliações

- Retail Communication ProgramDocumento10 páginasRetail Communication ProgramrachealllAinda não há avaliações

- Advantages of Performance AppraisalDocumento4 páginasAdvantages of Performance AppraisalrachealllAinda não há avaliações

- The Indian Retail Industry 2019Documento19 páginasThe Indian Retail Industry 2019rachealllAinda não há avaliações

- Relevance of Personal SellingDocumento8 páginasRelevance of Personal SellingrachealllAinda não há avaliações

- Job Enlargement N EnrichmentDocumento14 páginasJob Enlargement N EnrichmentrachealllAinda não há avaliações

- Advantages of Performance AppraisalDocumento4 páginasAdvantages of Performance AppraisalrachealllAinda não há avaliações

- Merits of Personal SellingDocumento9 páginasMerits of Personal Sellingrachealll0% (1)

- Problems Encoutered in An InterviewDocumento4 páginasProblems Encoutered in An InterviewrachealllAinda não há avaliações

- Lea Se Fin Anc IngDocumento22 páginasLea Se Fin Anc IngrachealllAinda não há avaliações

- Advantages of Performance AppraisalDocumento4 páginasAdvantages of Performance AppraisalrachealllAinda não há avaliações

- Relevance of Personal SellingDocumento8 páginasRelevance of Personal SellingrachealllAinda não há avaliações

- Final Accounts and Financial StatementsDocumento27 páginasFinal Accounts and Financial StatementsrachealllAinda não há avaliações

- Personal Selling Meaning & ObjectivesDocumento9 páginasPersonal Selling Meaning & ObjectivesrachealllAinda não há avaliações

- Demerits of Personal SellingDocumento11 páginasDemerits of Personal SellingrachealllAinda não há avaliações

- Retailpricing 091003142320 Phpapp01Documento15 páginasRetailpricing 091003142320 Phpapp01Dinesh MechAinda não há avaliações

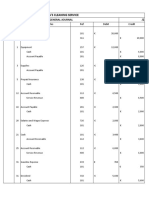

- Clearing & Settlement PDFDocumento24 páginasClearing & Settlement PDFGourav GoyelAinda não há avaliações

- CompensationpracticesDocumento46 páginasCompensationpracticesrachealllAinda não há avaliações

- Theories of Leadership: Prof - KhagendraDocumento43 páginasTheories of Leadership: Prof - KhagendrarachealllAinda não há avaliações

- Employee Participation N EmpowermentDocumento12 páginasEmployee Participation N EmpowermentrachealllAinda não há avaliações

- Tradeunions 2Documento26 páginasTradeunions 2rachealllAinda não há avaliações

- Personal Selling Meaning & ObjectivesDocumento9 páginasPersonal Selling Meaning & ObjectivesrachealllAinda não há avaliações

- InventoryDocumento3 páginasInventoryrachealllAinda não há avaliações

- 1 Introduction To StaffingDocumento57 páginas1 Introduction To StaffingrachealllAinda não há avaliações

- The Time Value of MoneyDocumento66 páginasThe Time Value of MoneyrachealllAinda não há avaliações

- 1 Introduction To StaffingDocumento57 páginas1 Introduction To StaffingrachealllAinda não há avaliações

- Overview and Preparation: Professor Raymond WestonDocumento46 páginasOverview and Preparation: Professor Raymond WestonrachealllAinda não há avaliações

- Session 5 - Hiring and RecruitingDocumento35 páginasSession 5 - Hiring and RecruitingrachealllAinda não há avaliações

- Anya's Cleaning ServiceDocumento22 páginasAnya's Cleaning ServiceArya HerdiansyahAinda não há avaliações

- CAFC - Accountancy - Revision NotesDocumento19 páginasCAFC - Accountancy - Revision Notesrmercy323Ainda não há avaliações

- Charles Schwab CorporationDocumento50 páginasCharles Schwab CorporationAjitesh AbhishekAinda não há avaliações

- Synopsis of Customer Acquisition and Retention StrategyDocumento9 páginasSynopsis of Customer Acquisition and Retention StrategyGopi Krishnan.nAinda não há avaliações

- Basic Economics Task Performance (Prelims)Documento1 páginaBasic Economics Task Performance (Prelims)godwill oliva0% (1)

- Job-Description-Management Trainee - HRDocumento2 páginasJob-Description-Management Trainee - HRatika_ja_218563Ainda não há avaliações

- Investor Presentation - April 2021: Asx AnnouncementDocumento28 páginasInvestor Presentation - April 2021: Asx AnnouncementALAinda não há avaliações

- Full-Text HTML XML Download As PDFDocumento17 páginasFull-Text HTML XML Download As PDFMARICAR TADURANAinda não há avaliações

- Entrepreneurial Finance 4th Edition Leach Test BankDocumento12 páginasEntrepreneurial Finance 4th Edition Leach Test BankDanielWilliamskpsrq100% (16)

- Ijcrt 192976Documento17 páginasIjcrt 192976Kshitiz BhardwajAinda não há avaliações

- Chapter 9 SolutionsDocumento41 páginasChapter 9 SolutionsRodAinda não há avaliações

- Home Office, Agency and Branch AccountingDocumento17 páginasHome Office, Agency and Branch AccountingRain LerogAinda não há avaliações

- Uts Asistensi Pengantar Akuntansi 2Documento5 páginasUts Asistensi Pengantar Akuntansi 2Falhan AuliaAinda não há avaliações

- Principles of Marketing Chapter 4 Developing The Marketing MixDocumento9 páginasPrinciples of Marketing Chapter 4 Developing The Marketing MixAnghelica Eunice88% (8)

- EPSM Unit 8 Presentation.Documento5 páginasEPSM Unit 8 Presentation.zeeshan saleemAinda não há avaliações

- Oscm Test BankDocumento594 páginasOscm Test BankTrang VânAinda não há avaliações

- PM2 - The Marketing ProcessDocumento41 páginasPM2 - The Marketing ProcessRHam VariasAinda não há avaliações

- International Product PlanningDocumento38 páginasInternational Product Planningsamrulezzz100% (16)

- The Effects of Earnings Management and Audit Quality On Cost of Equity Capital - Empirical Evidence From IndonesiaDocumento8 páginasThe Effects of Earnings Management and Audit Quality On Cost of Equity Capital - Empirical Evidence From IndonesiaRISKA DAMAYANTI AkuntansiAinda não há avaliações

- Samishti Infotech Private Limited Trial Balance: As of March 31, 2019Documento4 páginasSamishti Infotech Private Limited Trial Balance: As of March 31, 2019Mohammad IrfanAinda não há avaliações

- International Macroeconomics: Slides For Chapter 8: International Capital Market IntegrationDocumento54 páginasInternational Macroeconomics: Slides For Chapter 8: International Capital Market IntegrationM Kaderi KibriaAinda não há avaliações

- Contribution MarginDocumento6 páginasContribution Marginajeng.saraswatiAinda não há avaliações

- Strategic Management Chapter-10Documento22 páginasStrategic Management Chapter-10Towhidul HoqueAinda não há avaliações

- OTC Exchange of IndiaDocumento17 páginasOTC Exchange of IndiaJigar_Dedhia_8946Ainda não há avaliações

- Fabm2 - Q2 - M10Documento13 páginasFabm2 - Q2 - M10Ryza Mae AbabaoAinda não há avaliações

- Aman Chitkara - Assignment - (IMC)Documento30 páginasAman Chitkara - Assignment - (IMC)Rishabh KhichiAinda não há avaliações

- TFM Session Five FX ManagementDocumento64 páginasTFM Session Five FX ManagementmankeraAinda não há avaliações

- Solutions For Economics Review QuestionsDocumento28 páginasSolutions For Economics Review QuestionsDoris Acheng67% (3)

- 2.01 Characteristics of Economic SystemsDocumento1 página2.01 Characteristics of Economic SystemsAsif Mahmood50% (4)

- Asl EwdDocumento24 páginasAsl EwdRicardo MbAinda não há avaliações