Você também pode gostar

- 5 Force ModelDocumento2 páginas5 Force Model9986212378Ainda não há avaliações

- Decision Making in POMDocumento2 páginasDecision Making in POM9986212378Ainda não há avaliações

- Seven Quality ToolsDocumento64 páginasSeven Quality Tools9986212378Ainda não há avaliações

- 3D PrintingDocumento26 páginas3D Printing9986212378Ainda não há avaliações

- Stock Holding Corporation of India LTD, BangaloreDocumento17 páginasStock Holding Corporation of India LTD, Bangalore9986212378Ainda não há avaliações

- Buying Center RolesDocumento14 páginasBuying Center Roles9986212378Ainda não há avaliações

- Reliance Money: A Reliance Capital CompanyDocumento34 páginasReliance Money: A Reliance Capital Company9986212378Ainda não há avaliações

- Consumer Behaviour in Services: Key FactorDocumento15 páginasConsumer Behaviour in Services: Key Factor9986212378Ainda não há avaliações

- The Nature of Industrial BuyingDocumento40 páginasThe Nature of Industrial Buying99862123780% (1)

- Dimensions of Industrial MarketingDocumento45 páginasDimensions of Industrial Marketing9986212378100% (2)

- Marketing ImplicationsDocumento6 páginasMarketing Implications9986212378100% (1)

- EFFIE 2002 Case StudiesDocumento16 páginasEFFIE 2002 Case Studies9986212378100% (1)

- Public RelationsDocumento1 páginaPublic Relations9986212378Ainda não há avaliações

- Financial ManagementDocumento13 páginasFinancial Management9986212378Ainda não há avaliações

- Customer Expectations of ServiceDocumento13 páginasCustomer Expectations of Service9986212378Ainda não há avaliações

- Portfolio Performance MeasuresDocumento26 páginasPortfolio Performance Measures9986212378Ainda não há avaliações

- Reliance Money: A Reliance Capital CompanyDocumento34 páginasReliance Money: A Reliance Capital Company9986212378Ainda não há avaliações

- Fund Based ServicesDocumento6 páginasFund Based Services9986212378Ainda não há avaliações

- Cost Accounting: Pricing PolicyDocumento10 páginasCost Accounting: Pricing Policy9986212378Ainda não há avaliações

- Cost Control and Cost ReductionDocumento11 páginasCost Control and Cost Reduction9986212378Ainda não há avaliações

- Cost Accounting: Basic Nature and ConceptsDocumento28 páginasCost Accounting: Basic Nature and Concepts9986212378Ainda não há avaliações

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- NIF 2011 Financial StatermentsDocumento33 páginasNIF 2011 Financial StatermentsWeAreNIFAinda não há avaliações

- Abbreviation DefinitionDocumento14 páginasAbbreviation DefinitionsaluruAinda não há avaliações

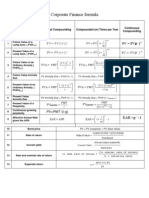

- Corporate Finance FormulasDocumento3 páginasCorporate Finance FormulasMustafa Yavuzcan83% (12)

- The Time Value of MoneyDocumento8 páginasThe Time Value of MoneyHaley James Scott0% (1)

- Quiz - Accounting For VHWO (Ver. 7)Documento9 páginasQuiz - Accounting For VHWO (Ver. 7)Von Andrei MedinaAinda não há avaliações

- Chap 10 CS ValuationDocumento84 páginasChap 10 CS ValuationBushra JavedAinda não há avaliações

- WSP Levered DCF Model VFDocumento5 páginasWSP Levered DCF Model VFBlahAinda não há avaliações

- Gin BilogDocumento14 páginasGin BilogHans Pierre AlfonsoAinda não há avaliações

- Financial FunctionsDocumento7 páginasFinancial FunctionsRavi Kumar KamparaAinda não há avaliações

- Module in General Mathematics Grade 11 Second Quarter, Week 3 To Week 4Documento39 páginasModule in General Mathematics Grade 11 Second Quarter, Week 3 To Week 4Hanseuuu100% (1)

- Batch 17 1st Preboard (P1) No AnswerDocumento6 páginasBatch 17 1st Preboard (P1) No AnswerAngelica manaoisAinda não há avaliações

- Exam FM Practice Exam 1 Answer KeyDocumento71 páginasExam FM Practice Exam 1 Answer Keynad_natt100% (1)

- Recitation 1 HandoutDocumento4 páginasRecitation 1 HandoutBuenaventura Mestanza MoriAinda não há avaliações

- Capital Budgeting Test Bank Part 2Documento167 páginasCapital Budgeting Test Bank Part 2AnnaAinda não há avaliações

- MAD AssignmentDocumento4 páginasMAD AssignmentSWETHA LAGISETTIAinda não há avaliações

- Fnce 100 Final Cheat SheetDocumento3 páginasFnce 100 Final Cheat Sheethung TranAinda não há avaliações

- Math 1090 Project Future Present Value With Periodic PaymentsDocumento6 páginasMath 1090 Project Future Present Value With Periodic Paymentsapi-270422704100% (1)

- Bonds Payable MillanDocumento7 páginasBonds Payable MillanFLORES, Reymart L.Ainda não há avaliações

- Flat Interest RateDocumento4 páginasFlat Interest Ratekeo linAinda não há avaliações

- CH 17Documento44 páginasCH 17Kyle Pilgrim80% (5)

- Intertemporal Choice & Asset MarketsDocumento25 páginasIntertemporal Choice & Asset MarketsifeanyiAinda não há avaliações

- CH 14Documento8 páginasCH 14antonydonAinda não há avaliações

- Financial Management - Bond ValuationDocumento17 páginasFinancial Management - Bond ValuationNoelia Mc DonaldAinda não há avaliações

- MGT 3078 Exam 1Documento2 páginasMGT 3078 Exam 18009438387Ainda não há avaliações

- DD 2656 (Mar 2022)Documento9 páginasDD 2656 (Mar 2022)Catalina PachecoAinda não há avaliações

- Time Value of MoneyDocumento25 páginasTime Value of MoneyAnand RaoAinda não há avaliações

- Revised Syllabus Mba ProgrammesDocumento132 páginasRevised Syllabus Mba ProgrammesANJANA MATHEWS100% (1)

- First Exam (ch.1-5) PDFDocumento43 páginasFirst Exam (ch.1-5) PDFOmar HosnyAinda não há avaliações

- Finance Summary PDFDocumento112 páginasFinance Summary PDFNabilah armyAinda não há avaliações

- IFRS 16 Leases Part 2 LessorDocumento56 páginasIFRS 16 Leases Part 2 LessorAnonymous SOclwwSAinda não há avaliações