Você também pode gostar

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5795)

- Market Indexes Must Confirm Each OtherDocumento9 páginasMarket Indexes Must Confirm Each Otheranish1012Ainda não há avaliações

- BCG and Ge MatrixDocumento17 páginasBCG and Ge Matrixanish1012Ainda não há avaliações

- Zer0 Based BudgetDocumento1 páginaZer0 Based Budgetanish1012Ainda não há avaliações

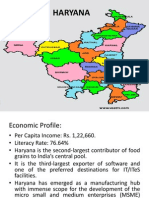

- HaryanaDocumento4 páginasHaryanaanish1012Ainda não há avaliações

- Date: 28 Sep 2013 Mr. R. Natrajan Fortune Limited, Andheri (W), MumbaiDocumento2 páginasDate: 28 Sep 2013 Mr. R. Natrajan Fortune Limited, Andheri (W), Mumbaianish1012Ainda não há avaliações

- Trimurti Foodtech PVT Ltd.Documento12 páginasTrimurti Foodtech PVT Ltd.anish1012Ainda não há avaliações

- Ambush MarketingDocumento18 páginasAmbush Marketinganish1012Ainda não há avaliações

- Best Influencer Marketing CampaignDocumento9 páginasBest Influencer Marketing Campaignanish1012Ainda não há avaliações

- Nikita Chawla (06) - Pranav BhagatDocumento6 páginasNikita Chawla (06) - Pranav Bhagatanish1012Ainda não há avaliações

- Business Mathematics AssignmentDocumento5 páginasBusiness Mathematics Assignmentanish1012Ainda não há avaliações

- Presentation On Transmission MediumDocumento19 páginasPresentation On Transmission Mediumanish1012100% (1)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- Duration and ConvexityDocumento21 páginasDuration and ConvexityStanislav LazarovAinda não há avaliações

- Chapter 10: Equity Valuation & AnalysisDocumento22 páginasChapter 10: Equity Valuation & AnalysisMumbo JumboAinda não há avaliações

- Resume Swap Markets 15-1 Background: 15-1a Use of Swaps For HedgingDocumento9 páginasResume Swap Markets 15-1 Background: 15-1a Use of Swaps For HedgingAbdul Aziz FaqihAinda não há avaliações

- Investment AttributesDocumento4 páginasInvestment AttributesNiranjan PhuyalAinda não há avaliações

- Franklin TempletonDocumento8 páginasFranklin TempletonPrashanta KhaitanAinda não há avaliações

- Overview of Financial Services in IndiaDocumento2 páginasOverview of Financial Services in IndiaRahulRaheja100% (1)

- Mortgage and PledgeDocumento158 páginasMortgage and PledgeBeatrice TehAinda não há avaliações

- Investors' Protection in India: Regulatory Framework and Investors' Rights, Obligations & GrievancesDocumento33 páginasInvestors' Protection in India: Regulatory Framework and Investors' Rights, Obligations & GrievancesHarshSuryavanshiAinda não há avaliações

- Cohen Finance Workbook FALL 2013Documento124 páginasCohen Finance Workbook FALL 2013Nayef AbdullahAinda não há avaliações

- Organisation Study - Anu Solar - Ravi PDFDocumento55 páginasOrganisation Study - Anu Solar - Ravi PDFManikantta SwamyAinda não há avaliações

- Ifrs-8 Operating SegmentsDocumento8 páginasIfrs-8 Operating SegmentsniichauhanAinda não há avaliações

- Profit Center AccountingDocumento55 páginasProfit Center AccountingBala RanganathAinda não há avaliações

- Ge 10Documento4 páginasGe 10Lisa LvqiuAinda não há avaliações

- Threshold Heteroskedastic Models: Jean-Michel ZakoianDocumento25 páginasThreshold Heteroskedastic Models: Jean-Michel ZakoianLuis Bautista0% (1)

- ZDA Spotlight: April 2010Documento7 páginasZDA Spotlight: April 2010Chola MukangaAinda não há avaliações

- Corporation ReviewerDocumento22 páginasCorporation Reviewerevlyn aplacaAinda não há avaliações

- Assignment 3: Part 1: Mutual Funds (20 Marks)Documento2 páginasAssignment 3: Part 1: Mutual Funds (20 Marks)Julia KristelAinda não há avaliações

- Internship Report TemplateDocumento2 páginasInternship Report TemplateBilal FakharAinda não há avaliações

- Kieso - IFRS - ch04 - IFRS (Income Statement)Documento73 páginasKieso - IFRS - ch04 - IFRS (Income Statement)Muzi RahayuAinda não há avaliações

- Rajkot District Co-Op. BankDocumento90 páginasRajkot District Co-Op. BankJay Zatakia67% (3)

- Single Factor and CAPMDocumento56 páginasSingle Factor and CAPMpyaarelal100% (1)

- Ipo Bid Form SampleDocumento2 páginasIpo Bid Form SampleRP groupAinda não há avaliações

- Synopsis GurpratapDocumento16 páginasSynopsis GurpratapGurpratap GillAinda não há avaliações

- CPA BEC Financial RatiosDocumento24 páginasCPA BEC Financial Ratiospambia200050% (2)

- ICICI Bank Board Approves Sale of 9.0% Stake in ICICI Lombard General Insurance Company To Fairfax Financial Holdings (Company Update)Documento2 páginasICICI Bank Board Approves Sale of 9.0% Stake in ICICI Lombard General Insurance Company To Fairfax Financial Holdings (Company Update)Shyam SunderAinda não há avaliações

- Aboitiz Power CorporationDocumento10 páginasAboitiz Power CorporationrobertAinda não há avaliações

- Planning and ForecastingDocumento16 páginasPlanning and ForecastingAinun Nisa NAinda não há avaliações

- CE On Intercompany Transactions PDFDocumento3 páginasCE On Intercompany Transactions PDFMarcus ReyesAinda não há avaliações

- Chap 013Documento30 páginasChap 013ducacapupu100% (1)