Você também pode gostar

- Fmi 2Documento41 páginasFmi 2Lebbe PuthaAinda não há avaliações

- Chapter 2 - Overview of Financial System (Autosaved)Documento56 páginasChapter 2 - Overview of Financial System (Autosaved)michellebaileylindsaAinda não há avaliações

- Overview of The Financial SystemDocumento61 páginasOverview of The Financial SystemIndira PriyadarsiniAinda não há avaliações

- Zohra 69 4325 1 M02 MISH1520 06 PPW C02Documento54 páginasZohra 69 4325 1 M02 MISH1520 06 PPW C02Aadil Hassan ShaikhAinda não há avaliações

- Overview of The Financial SystemDocumento63 páginasOverview of The Financial Systemhabiba ahmed100% (1)

- Overview of The Financial SystemDocumento53 páginasOverview of The Financial SystemE OzanAinda não há avaliações

- The Financial Market Environment: All Rights ReservedDocumento30 páginasThe Financial Market Environment: All Rights ReservedSajjad RavinAinda não há avaliações

- Fin 254 CH 2Documento38 páginasFin 254 CH 2Crap WeaselAinda não há avaliações

- Overview of The Financial SystemDocumento42 páginasOverview of The Financial SystemIkhsan Uiandra Putra SitorusAinda não há avaliações

- CH 2 Financial Market EnvironmentDocumento17 páginasCH 2 Financial Market EnvironmentAkash KarAinda não há avaliações

- Financial Imst &mark Unit - 2Documento57 páginasFinancial Imst &mark Unit - 2KalkayeAinda não há avaliações

- Gitman pmf13 ppt02Documento47 páginasGitman pmf13 ppt02marydraftAinda não há avaliações

- Overview of The Financial System: All Rights ReservedDocumento44 páginasOverview of The Financial System: All Rights ReservedAfaq AhmedAinda não há avaliações

- The Financial Market Environment: All Rights ReservedDocumento31 páginasThe Financial Market Environment: All Rights ReservedMahiAinda não há avaliações

- Chap. 2. Financial MarketsDocumento40 páginasChap. 2. Financial MarketsMichaelAngeloBattungAinda não há avaliações

- The Financial Market EnvironmentDocumento45 páginasThe Financial Market EnvironmentThenappan Ganesen100% (1)

- Keown Pearson 8eDocumento50 páginasKeown Pearson 8eAngelaLing100% (1)

- Week 1 Chapter 2Documento36 páginasWeek 1 Chapter 2Dương Thanh HuyềnAinda não há avaliações

- 8513 PresentationDocumento14 páginas8513 PresentationNoaman AkbarAinda não há avaliações

- The Financial Market EnvironmentDocumento50 páginasThe Financial Market EnvironmentLorrie Jean De GuzmanAinda não há avaliações

- Principles of Managerial Finance: Fifteenth EditionDocumento62 páginasPrinciples of Managerial Finance: Fifteenth EditionTanya PribylevaAinda não há avaliações

- Lectures 1-2 (Chapter 2)Documento25 páginasLectures 1-2 (Chapter 2)陳宇琳Ainda não há avaliações

- Pasig Catholic College: Financial Markets Chap. 2. Overview of The Financial SystemDocumento51 páginasPasig Catholic College: Financial Markets Chap. 2. Overview of The Financial SystemVictorioLazaroAinda não há avaliações

- Chapt 2 Financial Market EnvironmentDocumento20 páginasChapt 2 Financial Market Environmentimran_nazir448687Ainda não há avaliações

- International Finance & Financial MarketsDocumento39 páginasInternational Finance & Financial MarketsShaheena SanaAinda não há avaliações

- Mishkin PPT Ch02Documento17 páginasMishkin PPT Ch02atulkirar100% (1)

- Gitman pmf13 ppt02Documento49 páginasGitman pmf13 ppt02Khoa NguyễnAinda não há avaliações

- 1 - CH 2 Gitman 14eDocumento42 páginas1 - CH 2 Gitman 14eannisawulandariAinda não há avaliações

- The Financial Market EnvironmentDocumento18 páginasThe Financial Market Environmentlayan123456Ainda não há avaliações

- M02 Gitman50803X 14 MF C02Documento51 páginasM02 Gitman50803X 14 MF C02louise carinoAinda não há avaliações

- Mishkin FMI9ge PPT C02Documento35 páginasMishkin FMI9ge PPT C02dxgcyb4kwpAinda não há avaliações

- LN02 Keown33019306 08 LN02 GEDocumento52 páginasLN02 Keown33019306 08 LN02 GEEnny HaryantiAinda não há avaliações

- The Financial Market EnvironmentDocumento47 páginasThe Financial Market EnvironmentasimAinda não há avaliações

- Ch02 Financial Mkts and Institutions - MishkinEakins 2018-ENGDocumento58 páginasCh02 Financial Mkts and Institutions - MishkinEakins 2018-ENGHoàng Đỗ VănAinda não há avaliações

- Financial Markets and InstrumentDocumento30 páginasFinancial Markets and InstrumentAbdul Fattaah Bakhsh 1837065Ainda não há avaliações

- Financial Institutions NotesDocumento12 páginasFinancial Institutions NotesSherif ElSheemyAinda não há avaliações

- Chapter 2 The Financial Market EnvironmentDocumento35 páginasChapter 2 The Financial Market EnvironmentJames Kok67% (3)

- LN02Titman 449327 12 LN02Documento48 páginasLN02Titman 449327 12 LN02Nasrudin Insaf Bin Jaafarali100% (1)

- Chapter 2 NotesDocumento30 páginasChapter 2 NotesMaathir Al ShukailiAinda não há avaliações

- M02 Titman 2544318 11 FinMgt C02Documento55 páginasM02 Titman 2544318 11 FinMgt C02Abed AttariAinda não há avaliações

- Contemporary Financial Management 14th Edition Moyer Solutions ManualDocumento35 páginasContemporary Financial Management 14th Edition Moyer Solutions Manualexedentzigzag.96ewc96% (23)

- Lecture No. 1: Introduction: Fna 8111: Financial Institutions and MarketsDocumento33 páginasLecture No. 1: Introduction: Fna 8111: Financial Institutions and MarketsNimco CumarAinda não há avaliações

- Topic 2 - Long Term FinDocumento25 páginasTopic 2 - Long Term FinAina KhairunnisaAinda não há avaliações

- M02 Titman 2544318 11 FinMgt C02Documento57 páginasM02 Titman 2544318 11 FinMgt C02kennethfarnumAinda não há avaliações

- Investments - Background and Issues: Mcgraw-Hill/IrwinDocumento34 páginasInvestments - Background and Issues: Mcgraw-Hill/IrwinMosabAbuKhaterAinda não há avaliações

- EEB 2.2. Capital MarketDocumento37 páginasEEB 2.2. Capital Marketkaranj321Ainda não há avaliações

- Financial System GuideDocumento24 páginasFinancial System GuideShochrulAinda não há avaliações

- FINMARDocumento28 páginasFINMARrou ziaAinda não há avaliações

- Why Study Financial Markets? Financial Markets, Such As Bond and Stock Markets, Are Crucial in Our EconomyDocumento27 páginasWhy Study Financial Markets? Financial Markets, Such As Bond and Stock Markets, Are Crucial in Our EconomyShaheena SanaAinda não há avaliações

- CH - 02 Overview of The Financial SystemDocumento35 páginasCH - 02 Overview of The Financial SystemmahadiparvezAinda não há avaliações

- FINA3010 Lecture 1 PDFDocumento58 páginasFINA3010 Lecture 1 PDFKoon Sing ChanAinda não há avaliações

- CHAPTER 2 Financial Markets and InstitutionsDocumento37 páginasCHAPTER 2 Financial Markets and InstitutionsJessalyn CabaelAinda não há avaliações

- Lecture 2Documento33 páginasLecture 2Nursyahidah SafwanaAinda não há avaliações

- Gitman Pmf13 Ppt02 GEDocumento15 páginasGitman Pmf13 Ppt02 GEzaid.r.m.s.2004Ainda não há avaliações

- Lec 2 FM NumlDocumento22 páginasLec 2 FM Numlpal 8311Ainda não há avaliações

- Introduction To Financial MarketDocumento30 páginasIntroduction To Financial Marketmaria evangelistaAinda não há avaliações

- Equity Investment for CFA level 1: CFA level 1, #2No EverandEquity Investment for CFA level 1: CFA level 1, #2Nota: 5 de 5 estrelas5/5 (1)

- Financial Markets Fundamentals: Why, how and what Products are traded on Financial Markets. Understand the Emotions that drive TradingNo EverandFinancial Markets Fundamentals: Why, how and what Products are traded on Financial Markets. Understand the Emotions that drive TradingAinda não há avaliações

- Free PPT Templates for Presentation TitlesDocumento2 páginasFree PPT Templates for Presentation Titlesshahidul0Ainda não há avaliações

- Free PPT Templates: InsertDocumento2 páginasFree PPT Templates: Insertshahidul0Ainda não há avaliações

- Free PPT Templates: Insert The Title of Your Presentation HereDocumento2 páginasFree PPT Templates: Insert The Title of Your Presentation Hereshahidul0Ainda não há avaliações

- Free PPT Templates: Insert The Sub Title of Your PresentationDocumento14 páginasFree PPT Templates: Insert The Sub Title of Your Presentationshahidul0Ainda não há avaliações

- Slide ModeloDocumento48 páginasSlide ModeloIago Moura100% (1)

- Free PPT Templates for PresentationsDocumento2 páginasFree PPT Templates for Presentationsshahidul0Ainda não há avaliações

- Free PPT Templates: Insert The Title of Your Presentation HereDocumento3 páginasFree PPT Templates: Insert The Title of Your Presentation Hereshahidul0Ainda não há avaliações

- Free PPT Templates Infographic Style PresentationDocumento48 páginasFree PPT Templates Infographic Style PresentationMahasariAinda não há avaliações

- Free PPT Templates: Insert The Title of Your Presentation HereDocumento3 páginasFree PPT Templates: Insert The Title of Your Presentation Hereshahidul0Ainda não há avaliações

- Modern Infographic PowerPoint TemplateDocumento2 páginasModern Infographic PowerPoint Templateshahidul0Ainda não há avaliações

- Section Break: Insert Your Subtitle HereDocumento41 páginasSection Break: Insert Your Subtitle Hereshahidul0Ainda não há avaliações

- Business Style 2Documento9 páginasBusiness Style 2shahidul0Ainda não há avaliações

- Free PPT templates for any presentationDocumento2 páginasFree PPT templates for any presentationshahidul0Ainda não há avaliações

- Free PPT Templates: Insert The Sub Title of Your PresentationDocumento48 páginasFree PPT Templates: Insert The Sub Title of Your Presentationshahidul0Ainda não há avaliações

- Effective PresentationsDocumento4 páginasEffective Presentationsshahidul0Ainda não há avaliações

- PresentationDocumento1 páginaPresentationshahidul0Ainda não há avaliações

- Presentation On ElementDocumento6 páginasPresentation On Elementshahidul0Ainda não há avaliações

- POWERFUL PresentationDocumento3 páginasPOWERFUL Presentationshahidul0Ainda não há avaliações

- Business StyleDocumento10 páginasBusiness Styleshahidul0Ainda não há avaliações

- PresentationDocumento1 páginaPresentationshahidul0Ainda não há avaliações

- TeamDocumento4 páginasTeamshahidul0Ainda não há avaliações

- Click To Edit Master Title StyleDocumento4 páginasClick To Edit Master Title Styleshahidul0Ainda não há avaliações

- FlyingDocumento5 páginasFlyingshahidul0Ainda não há avaliações

- Strengths Weaknesses: - Edit Text Here - Edit Text Here - Edit Text Here - Edit Text HereDocumento1 páginaStrengths Weaknesses: - Edit Text Here - Edit Text Here - Edit Text Here - Edit Text Hereshahidul0Ainda não há avaliações

- Click To Edit Master Subtitle StyleDocumento8 páginasClick To Edit Master Subtitle Styleshahidul0Ainda não há avaliações

- Flow ChartDocumento2 páginasFlow Chartshahidul0Ainda não há avaliações

- Click To Edit Master Subtitle StyleDocumento4 páginasClick To Edit Master Subtitle Styleshahidul0Ainda não há avaliações

- Internship ReportDocumento11 páginasInternship Reportshahidul0Ainda não há avaliações

- Strategy of Challenger, Leader and FollowerDocumento26 páginasStrategy of Challenger, Leader and Followergohelgohel100% (2)

- Preparing Financial StatementsDocumento18 páginasPreparing Financial StatementsAUDITOR97Ainda não há avaliações

- Demand Analysis Question BankDocumento3 páginasDemand Analysis Question BanknisajamesAinda não há avaliações

- +supply Chain Course DescriptionsDocumento1 página+supply Chain Course DescriptionsPalashShahAinda não há avaliações

- Sales Forecasting Techniques ExplainedDocumento20 páginasSales Forecasting Techniques ExplainedLAUWA LUM DAUAinda não há avaliações

- ISO Quant and ISO CostDocumento14 páginasISO Quant and ISO CostMahesh Surve100% (1)

- Review QuestionsDocumento4 páginasReview Questionsnguyen ngoc lanAinda não há avaliações

- Target Market Analysis for Balibay JewelryDocumento11 páginasTarget Market Analysis for Balibay Jewelryrival ocmAinda não há avaliações

- Job Design in Service SectorDocumento2 páginasJob Design in Service SectorSweelin Tan100% (1)

- Seven Essential COmponents To A Marketting PlanDocumento1 páginaSeven Essential COmponents To A Marketting PlanGeneTearBodgesAinda não há avaliações

- CLV - CalculationDocumento10 páginasCLV - CalculationUtkarsh PandeyAinda não há avaliações

- Current Issues in Marketing (Teaching Plan)Documento5 páginasCurrent Issues in Marketing (Teaching Plan)Eric KongAinda não há avaliações

- (B207A) Shaping Business OpportunityDocumento6 páginas(B207A) Shaping Business OpportunityUtkarsh SharmaAinda não há avaliações

- Final CadburyDocumento18 páginasFinal CadburyChristieAinda não há avaliações

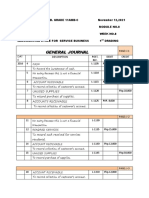

- Accounting Cycle for a Service BusinessDocumento5 páginasAccounting Cycle for a Service BusinessKristel Mae PayotAinda não há avaliações

- KAMMPIL Inc. 2022 Financial Statements Audit Representation LetterDocumento10 páginasKAMMPIL Inc. 2022 Financial Statements Audit Representation LetterJOHN MARK ARGUELLESAinda não há avaliações

- Joint Venture - Practice ProblemsDocumento9 páginasJoint Venture - Practice ProblemsrnbharathirajaAinda não há avaliações

- Acctg For LTCC - IllustrationsDocumento13 páginasAcctg For LTCC - IllustrationsGalang, Princess T.Ainda não há avaliações

- Sales Average InventoryDocumento7 páginasSales Average InventorysikderaminulAinda não há avaliações

- (CaseSt1) Balance Sheet, Short 2020 PBDocumento11 páginas(CaseSt1) Balance Sheet, Short 2020 PBtitu patriciuAinda não há avaliações

- List of Process For BBP Preparation (PP, SD, MM and FI)Documento22 páginasList of Process For BBP Preparation (PP, SD, MM and FI)Debi GhoshAinda não há avaliações

- An Organisation Study At": Internship Report ON by Prajwal A S Submitted ToDocumento18 páginasAn Organisation Study At": Internship Report ON by Prajwal A S Submitted ToPRAJWAL A SAinda não há avaliações

- I W e T e I M P: Aidil Hanafi Amirrudin, Nur Syuhadah Kamaruddin, Nurshahirah Salehuddin, Suraiya IbrahimDocumento15 páginasI W e T e I M P: Aidil Hanafi Amirrudin, Nur Syuhadah Kamaruddin, Nurshahirah Salehuddin, Suraiya IbrahimJoselyn CerveraAinda não há avaliações

- Motivation Letter For MechatronicsDocumento1 páginaMotivation Letter For MechatronicsMuhammad Zaka Ud Din60% (5)

- Hikery Business PlanDocumento24 páginasHikery Business PlanAzhan RabbaniAinda não há avaliações

- Solutions - Chapter 7Documento18 páginasSolutions - Chapter 7Dre ThathipAinda não há avaliações

- Multiple Choice Questions: Concept Check QuizDocumento8 páginasMultiple Choice Questions: Concept Check QuizReza KhatamiAinda não há avaliações

- 1 Main Capital Quarterly LetterDocumento10 páginas1 Main Capital Quarterly LetterYog MehtaAinda não há avaliações

- 1465815374Documento22 páginas1465815374NeemaAinda não há avaliações

- Diploma in Accountancy Qa March 2022Documento217 páginasDiploma in Accountancy Qa March 2022Chanda LufunguloAinda não há avaliações