Você também pode gostar

- Value Chain Management Capability A Complete Guide - 2020 EditionNo EverandValue Chain Management Capability A Complete Guide - 2020 EditionAinda não há avaliações

- Activity-Based CostingDocumento24 páginasActivity-Based CostingAmrit PatnaikAinda não há avaliações

- Differential AnalysisDocumento6 páginasDifferential AnalysisGina Mantos GocotanoAinda não há avaliações

- Cost and Cost Classifications PDFDocumento5 páginasCost and Cost Classifications PDFnkznhrgAinda não há avaliações

- Job-Order Costing System ExplainedDocumento46 páginasJob-Order Costing System Explainednicero555Ainda não há avaliações

- Group Accounts - Cashflow Statement-1Documento19 páginasGroup Accounts - Cashflow Statement-1antony omondiAinda não há avaliações

- ch06, Accounting PrinciplesDocumento66 páginasch06, Accounting PrinciplesH.R. RobinAinda não há avaliações

- I. Product Costs and Service Costs: Absorption CostingDocumento12 páginasI. Product Costs and Service Costs: Absorption CostingLinyVatAinda não há avaliações

- Activity-Based Cost Management For Design and Development StageDocumento15 páginasActivity-Based Cost Management For Design and Development Stagebimbi purbaAinda não há avaliações

- Additional Aspects of Costing SystemsDocumento28 páginasAdditional Aspects of Costing SystemsKağan GrrgnAinda não há avaliações

- Cost Volume Profit AnalysisDocumento16 páginasCost Volume Profit AnalysisAMITS1014Ainda não há avaliações

- Module 2 Sub Mod 2 Standard Costing and Material Variance FinalDocumento31 páginasModule 2 Sub Mod 2 Standard Costing and Material Variance Finalmaheshbendigeri5945Ainda não há avaliações

- Lecture 11 - Investment PropertyDocumento17 páginasLecture 11 - Investment PropertyYogeswari RavindranAinda não há avaliações

- 03 Cost BehaviourDocumento24 páginas03 Cost BehaviourArindam DasAinda não há avaliações

- Absorption Costing Vs Variable CostingDocumento2 páginasAbsorption Costing Vs Variable Costingneway gobachew100% (1)

- Balanced Scorecard and Benchmarking StrategiesDocumento12 páginasBalanced Scorecard and Benchmarking StrategiesGaurav Sharma100% (1)

- Final Ratio Analysis (2) - 2Documento4 páginasFinal Ratio Analysis (2) - 2anjuAinda não há avaliações

- Short-Run Decision Making and CVP AnalysisDocumento43 páginasShort-Run Decision Making and CVP AnalysisHy Tang100% (1)

- Absorption Costing (Or Full Costing) and Marginal CostingDocumento11 páginasAbsorption Costing (Or Full Costing) and Marginal CostingCharsi Unprofessional BhaiAinda não há avaliações

- Digital Transformation in Companies - Challenges and Success FactorsDocumento16 páginasDigital Transformation in Companies - Challenges and Success FactorsUliana Baka100% (1)

- Makerere University College of Business and Management Studies Master of Business AdministrationDocumento15 páginasMakerere University College of Business and Management Studies Master of Business AdministrationDamulira DavidAinda não há avaliações

- Consolidated Financial StatementsDocumento7 páginasConsolidated Financial StatementsParvez NahidAinda não há avaliações

- Management Accounting Chap 003Documento67 páginasManagement Accounting Chap 003kenha2000Ainda não há avaliações

- Characteristics of Organizational Change: Organizational Development Finals ReviewerDocumento4 páginasCharacteristics of Organizational Change: Organizational Development Finals ReviewerMarvin OngAinda não há avaliações

- Investment AppraisalDocumento8 páginasInvestment AppraisaldeepkandelAinda não há avaliações

- ch03, Accounting PrinciplesDocumento78 páginasch03, Accounting PrinciplesH.R. Robin100% (2)

- SMChap 007Documento86 páginasSMChap 007Huishan Zheng100% (5)

- Investment Analysis and Portfolio Management: Frank K. Reilly & Keith C. BrownDocumento122 páginasInvestment Analysis and Portfolio Management: Frank K. Reilly & Keith C. BrownWhy you want to knowAinda não há avaliações

- As 26 Intangible AssetsDocumento45 páginasAs 26 Intangible Assetsjoseph davidAinda não há avaliações

- C.1. Purpose of BudgetingDocumento11 páginasC.1. Purpose of BudgetingTiyas KurniaAinda não há avaliações

- Process-Costing Systems: Answers To Review QuestionsDocumento51 páginasProcess-Costing Systems: Answers To Review QuestionsMark RevarezAinda não há avaliações

- Distinguish Between Marginal Costing and Absorption CostingDocumento10 páginasDistinguish Between Marginal Costing and Absorption Costingmohamed Suhuraab50% (2)

- Tools and Techniques of Cost ReductionDocumento27 páginasTools and Techniques of Cost Reductionপ্রিয়াঙ্কুর ধর100% (2)

- Topic 6 Business IncomeDocumento37 páginasTopic 6 Business IncomeMuhamad Safwan ZulkifliAinda não há avaliações

- Target Costing Presentation FinalDocumento57 páginasTarget Costing Presentation FinalMr Dampha100% (1)

- Marginal CostingDocumento30 páginasMarginal Costinganon_3722476140% (1)

- Topic 7 - Absorption & Marginal CostingDocumento8 páginasTopic 7 - Absorption & Marginal CostingMuhammad Alif100% (5)

- Cost Accounting Book of 3rd Sem Mba at Bec DomsDocumento174 páginasCost Accounting Book of 3rd Sem Mba at Bec DomsBabasab Patil (Karrisatte)100% (1)

- Chapter 9 - Inventory Costing and Capacity AnalysisDocumento40 páginasChapter 9 - Inventory Costing and Capacity AnalysisBrian SantsAinda não há avaliações

- Difference Between Absorption Costing and Marginal CostingDocumento4 páginasDifference Between Absorption Costing and Marginal CostingIndu GuptaAinda não há avaliações

- Maf5102 Fa Cat 2 2018Documento4 páginasMaf5102 Fa Cat 2 2018Muya KihumbaAinda não há avaliações

- Cost Accounting, Job Costing & Batch CostingDocumento10 páginasCost Accounting, Job Costing & Batch Costing✬ SHANZA MALIK ✬Ainda não há avaliações

- Break-Even Analysis/Cvp AnalysisDocumento41 páginasBreak-Even Analysis/Cvp AnalysisMehwish ziadAinda não há avaliações

- Managerial Accounting Hilton 6e Chapter 4 Solution PDFDocumento68 páginasManagerial Accounting Hilton 6e Chapter 4 Solution PDFNoor QamarAinda não há avaliações

- Assignment 1 PDFDocumento2 páginasAssignment 1 PDFHARIAinda não há avaliações

- BUS 5116 Portfolio Assignment WK 8Documento6 páginasBUS 5116 Portfolio Assignment WK 8TaiwokAinda não há avaliações

- Ch09 Inventory Costing and Capacity AnalysisDocumento13 páginasCh09 Inventory Costing and Capacity AnalysisChaituAinda não há avaliações

- Accounting Principles SolutionsDocumento15 páginasAccounting Principles SolutionsShi Pyeit Sone Kyaw0% (1)

- Measuring Performance With Financial and Non-Financial MetricsDocumento13 páginasMeasuring Performance With Financial and Non-Financial MetricsAyesha SohailAinda não há avaliações

- NotesDocumento155 páginasNotesZainab Syeda100% (1)

- Absorption Costing Vs Marginal CostingDocumento5 páginasAbsorption Costing Vs Marginal Costingsani02Ainda não há avaliações

- Differential Cost Analysis PDFDocumento4 páginasDifferential Cost Analysis PDFVivienne Lei BolosAinda não há avaliações

- The Role of Finacial ManagementDocumento25 páginasThe Role of Finacial Managementnitinvohra_capricorn100% (1)

- Capital Budgeting KSBDocumento59 páginasCapital Budgeting KSBSamridhi KukrejaAinda não há avaliações

- L28 29 Non Financial Measures of Performance EvaluationDocumento11 páginasL28 29 Non Financial Measures of Performance Evaluationapi-3820619100% (1)

- ABC Costing Lecture NotesDocumento12 páginasABC Costing Lecture NotesMickel AlexanderAinda não há avaliações

- Activity Based CostingDocumento52 páginasActivity Based CostingAfrina AfsarAinda não há avaliações

- Study Objectives: Activity-Based CostingDocumento48 páginasStudy Objectives: Activity-Based Costingsueern100% (1)

- Study Objectives Study ObjectivesDocumento59 páginasStudy Objectives Study ObjectivesAiza S. Maca-umbosAinda não há avaliações

- Activity Based Costing: By: Kasahun N. (M.SC.)Documento20 páginasActivity Based Costing: By: Kasahun N. (M.SC.)Mulugeta WoldeAinda não há avaliações

- The Trans-Pacific Partnership (Trade of Goods)Documento6 páginasThe Trans-Pacific Partnership (Trade of Goods)Daniel John Cañares LegaspiAinda não há avaliações

- Candidates For Internship Program For 1st Term AY 2015-2016Documento1 páginaCandidates For Internship Program For 1st Term AY 2015-2016Daniel John Cañares LegaspiAinda não há avaliações

- Gen Banking LawDocumento11 páginasGen Banking LawDaniel John Cañares LegaspiAinda não há avaliações

- Bank Secrecy LawDocumento2 páginasBank Secrecy LawDaniel John Cañares LegaspiAinda não há avaliações

- IntelDocumento11 páginasIntelDaniel John Cañares LegaspiAinda não há avaliações

- Table of Contents - Tech DraftDocumento2 páginasTable of Contents - Tech DraftDaniel John Cañares LegaspiAinda não há avaliações

- Certificate of Recognition: Charrevie M. TingsonDocumento2 páginasCertificate of Recognition: Charrevie M. TingsonDaniel John Cañares LegaspiAinda não há avaliações

- PCAOB Auditing Standards Chapter 5Documento35 páginasPCAOB Auditing Standards Chapter 5Daniel John Cañares Legaspi100% (1)

- BEHASCIDocumento2 páginasBEHASCIDaniel John Cañares LegaspiAinda não há avaliações

- Santa Rosa Science and Technology High School Values Education ExamDocumento1 páginaSanta Rosa Science and Technology High School Values Education ExamPrinces Paula Mendoza BalanayAinda não há avaliações

- City University of PasayDocumento2 páginasCity University of PasayDaniel John Cañares LegaspiAinda não há avaliações

- SOE Week Sportsfest 2014 Schedule November 24-28Documento2 páginasSOE Week Sportsfest 2014 Schedule November 24-28Daniel John Cañares LegaspiAinda não há avaliações

- Scatter Plot: 10000 F (X) 7.6826983136x 2 - 10550.0630855715x + 10546.0342910681 R 0.9999999728Documento6 páginasScatter Plot: 10000 F (X) 7.6826983136x 2 - 10550.0630855715x + 10546.0342910681 R 0.9999999728Daniel John Cañares LegaspiAinda não há avaliações

- Stra ManDocumento137 páginasStra ManDaniel John Cañares LegaspiAinda não há avaliações

- Introduction of The CompanyDocumento7 páginasIntroduction of The CompanyDaniel John Cañares LegaspiAinda não há avaliações

- Data DictionaryDocumento4 páginasData DictionaryDaniel John Cañares LegaspiAinda não há avaliações

- Chapter 3. Decision Analysis Section 3.1. Decision Trees With Conditional ProbabilitiesDocumento12 páginasChapter 3. Decision Analysis Section 3.1. Decision Trees With Conditional ProbabilitiesDaniel John Cañares LegaspiAinda não há avaliações

- Phoenix Wright Ace Attorney Trials and TribulationDocumento54 páginasPhoenix Wright Ace Attorney Trials and TribulationjinzoningenAinda não há avaliações

- CentralizeDocumento2 páginasCentralizeDaniel John Cañares LegaspiAinda não há avaliações

- Partnership ReviewerDocumento21 páginasPartnership ReviewerDaniel John Cañares Legaspi100% (1)

- Prinmar SurveyDocumento1 páginaPrinmar SurveyDaniel John Cañares LegaspiAinda não há avaliações

- October 2014 CPALE TopnotchersDocumento2 páginasOctober 2014 CPALE TopnotchersRockacerAinda não há avaliações

- Resume FormatDocumento2 páginasResume FormatJessicaGonzalesAinda não há avaliações

- PhotoshootDocumento1 páginaPhotoshootDaniel John Cañares LegaspiAinda não há avaliações

- Del Mundo Q and ADocumento2 páginasDel Mundo Q and ADaniel John Cañares LegaspiAinda não há avaliações

- 23 Marcon, Louise Margarette 24 Millar, AllyssaDocumento2 páginas23 Marcon, Louise Margarette 24 Millar, AllyssaDaniel John Cañares LegaspiAinda não há avaliações

- Rgf-Glossary of Terms-Chapter 14-Withholding TaxesDocumento1 páginaRgf-Glossary of Terms-Chapter 14-Withholding TaxesanggandakonohAinda não há avaliações

- Chapter 6Documento2 páginasChapter 6Daniel John Cañares LegaspiAinda não há avaliações

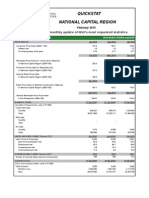

- Quickstat National Capital Region: A Monthly Update of NSO's Most Requested StatisticsDocumento3 páginasQuickstat National Capital Region: A Monthly Update of NSO's Most Requested StatisticsDaniel John Cañares LegaspiAinda não há avaliações

- ABC MemoDocumento4 páginasABC MemoPriyanshi PatelAinda não há avaliações

- BACT 302 Activity Based CostingDocumento25 páginasBACT 302 Activity Based CostingLetsah BrightAinda não há avaliações

- Chapter 4 The 3 Es of Operation Al ExcellenceDocumento13 páginasChapter 4 The 3 Es of Operation Al ExcellenceJimmy Ong Ah HuatAinda não há avaliações

- f5 Smart NotesDocumento98 páginasf5 Smart Notessakhiahmadyar100% (1)

- Exam 2 Practice QuestionDocumento3 páginasExam 2 Practice QuestionJaceAinda não há avaliações

- Group Case Study 1 - ABC Sietron Furniture SDN BHDDocumento18 páginasGroup Case Study 1 - ABC Sietron Furniture SDN BHDizzarulshazwanAinda não há avaliações

- Budgeting Chapter Explains Key ConceptsDocumento20 páginasBudgeting Chapter Explains Key ConceptsSunny Kumar10Ainda não há avaliações

- Pillsbury: Customer Driven ReengineeringDocumento20 páginasPillsbury: Customer Driven ReengineeringAakashRaval100% (1)

- Management Accounting Practices of Philippine SMEsDocumento21 páginasManagement Accounting Practices of Philippine SMEspamela dequillamorteAinda não há avaliações

- Process-Oriented Costing System Optimizes Siemens Motor Works ProfitsDocumento5 páginasProcess-Oriented Costing System Optimizes Siemens Motor Works ProfitsNikhil Jindal100% (1)

- Chapter 2: Management Accounting and The Business EnvironmentDocumento2 páginasChapter 2: Management Accounting and The Business EnvironmentEmma Mariz Garcia100% (1)

- Manusia LemahDocumento8 páginasManusia LemahKhoirul MubinAinda não há avaliações

- ACCAF5 - Qbank2017 - by First Intuition Downloaded FromDocumento384 páginasACCAF5 - Qbank2017 - by First Intuition Downloaded FromAbdul Jabbar Al-Shaer100% (4)

- CH 12 ABC Costing ExampleDocumento33 páginasCH 12 ABC Costing ExampleSweetu Nancy100% (1)

- Chapter 10: Fundamentals of Cost ManagementDocumento13 páginasChapter 10: Fundamentals of Cost ManagementaweysAinda não há avaliações

- Lecture 3 Costing and Costing TechniquesDocumento43 páginasLecture 3 Costing and Costing TechniquesehsanAinda não há avaliações

- Blocher 9e Chap001Documento34 páginasBlocher 9e Chap001adamagha703Ainda não há avaliações

- Chapter 6 - A London BoroughDocumento8 páginasChapter 6 - A London BoroughCharm RegultoAinda não há avaliações

- Case Concerning Volume-Based Costing Versus Activity-Based CostingDocumento2 páginasCase Concerning Volume-Based Costing Versus Activity-Based CostingNahid Hussain AdriAinda não há avaliações

- FIKRISHA RESEARCH Final Project (Repaired)Documento45 páginasFIKRISHA RESEARCH Final Project (Repaired)Eng-Mukhtaar CatooshAinda não há avaliações

- Chapter 14Documento25 páginasChapter 14ibraAinda não há avaliações

- Abc QustionsDocumento5 páginasAbc QustionsWynie AreolaAinda não há avaliações

- Activity Based Costing ExampleDocumento7 páginasActivity Based Costing ExamplePrasanna DanguiAinda não há avaliações

- Wilkerson CompanyDocumento26 páginasWilkerson CompanyChris Vincent50% (2)

- Activity Based CostingDocumento17 páginasActivity Based CostingArpit GargAinda não há avaliações

- ABM Cost Management Tools Chapter ReviewDocumento51 páginasABM Cost Management Tools Chapter ReviewVivekRaptorAinda não há avaliações

- Highly Competitive Warehouse ManagemetDocumento251 páginasHighly Competitive Warehouse Managemetjimdacalano191150% (2)

- Activity Based Costing SystemDocumento18 páginasActivity Based Costing SystemMAXA FASHIONAinda não há avaliações

- Managerial Accounting Assignment PDFDocumento4 páginasManagerial Accounting Assignment PDFanteneh tesfawAinda não há avaliações