Você também pode gostar

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- Chapter5 CasestudyDocumento4 páginasChapter5 CasestudyArbindchaudharyAinda não há avaliações

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- SAP S4 HANA Finance - Financial and Management Accounting - Upskilling For SAP ERP Financials Experts - Jun 2021Documento12 páginasSAP S4 HANA Finance - Financial and Management Accounting - Upskilling For SAP ERP Financials Experts - Jun 2021shoeb kanpurwala0% (1)

- SM ch08Documento17 páginasSM ch08muzzammil17Ainda não há avaliações

- SM ch03Documento18 páginasSM ch03muzzammil17Ainda não há avaliações

- SM ch02Documento15 páginasSM ch02muzzammil17Ainda não há avaliações

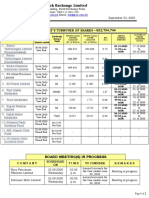

- Chi Stock Exchange Limited: Placement of Companies in The Defaulters' Segment and Suspension of Trading in Their SharesDocumento1 páginaChi Stock Exchange Limited: Placement of Companies in The Defaulters' Segment and Suspension of Trading in Their Sharesmuzzammil17Ainda não há avaliações

- Today'S Turnover of Shares - 582,794,744: CompanyDocumento2 páginasToday'S Turnover of Shares - 582,794,744: Companymuzzammil17Ainda não há avaliações

- Survey Questionnaire About Reading NewspaperDocumento2 páginasSurvey Questionnaire About Reading Newspapermuzzammil17Ainda não há avaliações

- Business Research Methods: Theory BuildingDocumento19 páginasBusiness Research Methods: Theory Buildingmuzzammil17Ainda não há avaliações

- Bài Học Từ Vựng Theo Chủ Điểm: Education: VocabularyDocumento5 páginasBài Học Từ Vựng Theo Chủ Điểm: Education: VocabularykatieAinda não há avaliações

- Phase 1 - Theme-Based Authentic Performance and Assessment - Determining Meaningful TransfersDocumento17 páginasPhase 1 - Theme-Based Authentic Performance and Assessment - Determining Meaningful TransfersCarl CorreosAinda não há avaliações

- Your Journey: I.Pre-TestDocumento14 páginasYour Journey: I.Pre-TestmikkaellaAinda não há avaliações

- SubconsciousDocumento24 páginasSubconsciousOVVCMOULIAinda não há avaliações

- Ecocriticism Essay - The Search For NatureDocumento7 páginasEcocriticism Essay - The Search For NatureemmyjayneAinda não há avaliações

- Module2 PPST1 4 2Documento32 páginasModule2 PPST1 4 2Jhonabie Suligan Cadeliña100% (2)

- Latonya's Teaching StatementDocumento2 páginasLatonya's Teaching Statementlatonya millienAinda não há avaliações

- MGT501Documento125 páginasMGT501chi100% (2)

- Chapter 1Documento8 páginasChapter 1juvelieanngambanAinda não há avaliações

- Work Immersion Portfolio Based On Deped-1Documento51 páginasWork Immersion Portfolio Based On Deped-1funelasrhiza4Ainda não há avaliações

- Fit SigmaDocumento9 páginasFit SigmaIbrahim MohammedAinda não há avaliações

- The Lamppost: Important DatesDocumento8 páginasThe Lamppost: Important DatesleconteschoolAinda não há avaliações

- Iphp11 Q4 M2Documento9 páginasIphp11 Q4 M2Sarai Hagar Baccay GuzmanAinda não há avaliações

- 4 Steps Every Successful Game and VR Experience Needs To Go ThroughDocumento2 páginas4 Steps Every Successful Game and VR Experience Needs To Go ThroughKerri-Ann PRINCEAinda não há avaliações

- Kalasalingam University: 2006 - 2010 BatchDocumento18 páginasKalasalingam University: 2006 - 2010 Batchharish_1984Ainda não há avaliações

- Select A TimeDocumento9 páginasSelect A TimeMuthu RamanAinda não há avaliações

- Introducing New Market OfferingsDocumento30 páginasIntroducing New Market OfferingsMr. Saravana KumarAinda não há avaliações

- NSG 300c Rs ClinicalevaluationtoolDocumento9 páginasNSG 300c Rs Clinicalevaluationtoolapi-496082612Ainda não há avaliações

- Abundis Mendivil Sofía Getting Things DoneDocumento6 páginasAbundis Mendivil Sofía Getting Things DoneSof AMAinda não há avaliações

- Analysing The Concept of Performance Appraisal System On Employees DevelopmentDocumento9 páginasAnalysing The Concept of Performance Appraisal System On Employees DevelopmentKarthikeya Rao PonugotiAinda não há avaliações

- Lesson Plan 1 2Documento6 páginasLesson Plan 1 2api-299108629Ainda não há avaliações

- Important Works For Drum Set As A Multiple Percussion InstrumentDocumento139 páginasImportant Works For Drum Set As A Multiple Percussion Instrumentshemlx100% (1)

- Alexis Kugelmans ResumeDocumento1 páginaAlexis Kugelmans Resumeapi-740455952Ainda não há avaliações

- Template For Opcrf of School Heads 1Documento29 páginasTemplate For Opcrf of School Heads 1Mark San Andres100% (1)

- EED 8 Course OutlineDocumento2 páginasEED 8 Course OutlineLeonnee Jane Cirpo100% (1)

- Modalexercises PDFDocumento1 páginaModalexercises PDFGergadroAlmib0% (1)

- Chapter 1 Entrepreneurs: The Driving Force Behind Small BusinessDocumento22 páginasChapter 1 Entrepreneurs: The Driving Force Behind Small BusinessAhmad AnoutiAinda não há avaliações

- Stayhungrystayfoolish ArticleDocumento5 páginasStayhungrystayfoolish Articleapi-239117703Ainda não há avaliações