Você também pode gostar

- Introduction To Public IssueDocumento15 páginasIntroduction To Public IssuePappu ChoudharyAinda não há avaliações

- 9 MCQ On Third Party Products With Ans.Documento4 páginas9 MCQ On Third Party Products With Ans.Nitin MalikAinda não há avaliações

- Your Results For - Multiple ChoiceDocumento3 páginasYour Results For - Multiple ChoiceSeema KujurAinda não há avaliações

- Question Bank Business LawDocumento2 páginasQuestion Bank Business LawNeha BhatiaAinda não há avaliações

- Vouching of Building N Bill PayableDocumento10 páginasVouching of Building N Bill PayableMohammed BilalAinda não há avaliações

- Operations Research MCQ PDFDocumento17 páginasOperations Research MCQ PDFDipak Mahalik100% (1)

- Inflation AccountingDocumento34 páginasInflation AccountingUnbeatable 9503Ainda não há avaliações

- BWRR3143 - Chapter 4 - Ins ContractsDocumento32 páginasBWRR3143 - Chapter 4 - Ins ContractsWingFatt KhooAinda não há avaliações

- Companies Act 1956 Notes PDFDocumento73 páginasCompanies Act 1956 Notes PDFsanresAinda não há avaliações

- Corporate Law Case StudiesDocumento2 páginasCorporate Law Case Studiesshaurya Jain100% (1)

- 23 Issue, Forfeiture and Reissue of Shares PDFDocumento13 páginas23 Issue, Forfeiture and Reissue of Shares PDFsureshdevidasAinda não há avaliações

- Ext 601 TheoryDocumento40 páginasExt 601 Theorysandeep gp100% (1)

- REDEMPTION OF SHARES & DEBENTURES MCQsDocumento7 páginasREDEMPTION OF SHARES & DEBENTURES MCQsChetan StoresAinda não há avaliações

- Business Regulatory Framework Set 2Documento2 páginasBusiness Regulatory Framework Set 2Titus Clement100% (1)

- Chapter 9: Legal Challenges of Entrepreneurial Ventures: True/FalseDocumento6 páginasChapter 9: Legal Challenges of Entrepreneurial Ventures: True/Falseelizabeth bernalesAinda não há avaliações

- Business Law BBA: 206-B Bba 4 SEM Question Bank: Unit-1Documento2 páginasBusiness Law BBA: 206-B Bba 4 SEM Question Bank: Unit-1monikaAinda não há avaliações

- IPCC - 33e - Differences & True or False Statements in Indian Contract ActDocumento58 páginasIPCC - 33e - Differences & True or False Statements in Indian Contract Actmohan100% (3)

- Tandon Committee Report On Working CapitalDocumento4 páginasTandon Committee Report On Working CapitalMohitAhujaAinda não há avaliações

- The Empirical School or The Management by Customs SchoolDocumento3 páginasThe Empirical School or The Management by Customs SchoolMaeve AguerroAinda não há avaliações

- Business OrganisationDocumento87 páginasBusiness OrganisationVictor Boateng100% (2)

- AFS MCQsDocumento43 páginasAFS MCQsNayab KhanAinda não há avaliações

- RIMT University: Part-A (Question-1) (MCQ) (All Questions Are Compulsory) 01 12 12 MarksDocumento3 páginasRIMT University: Part-A (Question-1) (MCQ) (All Questions Are Compulsory) 01 12 12 MarksharpominderAinda não há avaliações

- Entrepreneurship and Small Business Management Multiple Choice QuestionsDocumento54 páginasEntrepreneurship and Small Business Management Multiple Choice QuestionsANDUALEM MENGISTEAinda não há avaliações

- BUSINESS LAW and EthicsDocumento2 páginasBUSINESS LAW and EthicsSowjanya TalapakaAinda não há avaliações

- 01 Philosophical FoundationsDocumento21 páginas01 Philosophical FoundationsSharifah Amrina100% (2)

- Business Law McqsDocumento2 páginasBusiness Law McqsHaseeb ShaikhAinda não há avaliações

- Funds Flow Statement MCQs Schedule of Changes in Financial Position Multiple Choice Questions and AnDocumento7 páginasFunds Flow Statement MCQs Schedule of Changes in Financial Position Multiple Choice Questions and Anshuhal Ahmed33% (3)

- PPC Model Exam Question PaperDocumento2 páginasPPC Model Exam Question PapertharunAinda não há avaliações

- Financial Management Mcqs With AnswersDocumento53 páginasFinancial Management Mcqs With Answersviveksharma51Ainda não há avaliações

- Section 2 (4) Section 4 (2) Section 3 (1) Section 1 (3) A-CDocumento5 páginasSection 2 (4) Section 4 (2) Section 3 (1) Section 1 (3) A-CNaqeeb Ur RehmanAinda não há avaliações

- Retail Mcqs 19 20 Batch PDFDocumento26 páginasRetail Mcqs 19 20 Batch PDFShailendra JoshiAinda não há avaliações

- Collective Bargaining Process: Megha .U S3 MbaDocumento8 páginasCollective Bargaining Process: Megha .U S3 MbaMegha UnniAinda não há avaliações

- 17Uco6Mc04 Modern Banking Pratices Question Bank Unit - 1: Introduction To BankingDocumento4 páginas17Uco6Mc04 Modern Banking Pratices Question Bank Unit - 1: Introduction To BankingSimon JosephAinda não há avaliações

- Unit 3 HRM Recruitment Selection MCQDocumento2 páginasUnit 3 HRM Recruitment Selection MCQguddan prajapatiAinda não há avaliações

- Merchant Banking and Financial Services Question PaperDocumento248 páginasMerchant Banking and Financial Services Question Paperexecutivesenthilkumar100% (1)

- MCQ 464Documento10 páginasMCQ 464Tonmoy MajumderAinda não há avaliações

- FD MCQ 2Documento2 páginasFD MCQ 2ruchi agrawal100% (1)

- Define The Term SecurityDocumento8 páginasDefine The Term SecurityMahaboob PashaAinda não há avaliações

- PE2-001 - Nigerian Labour Law (Regu)Documento7 páginasPE2-001 - Nigerian Labour Law (Regu)Tega Nesirosan100% (1)

- Note On Public IssueDocumento9 páginasNote On Public IssueKrish KalraAinda não há avaliações

- EOQ Is A Point Where: Select Correct Option: Ordering CostDocumento5 páginasEOQ Is A Point Where: Select Correct Option: Ordering CostKhurram NadeemAinda não há avaliações

- CT9 Business Awareness Module PDFDocumento4 páginasCT9 Business Awareness Module PDFVignesh SrinivasanAinda não há avaliações

- Audit MCQ by IcaiDocumento24 páginasAudit MCQ by IcaiRahulAinda não há avaliações

- Amalgamation, Absorption, Reconstruction, and General Insurance Company MCQDocumento17 páginasAmalgamation, Absorption, Reconstruction, and General Insurance Company MCQbharat wankhedeAinda não há avaliações

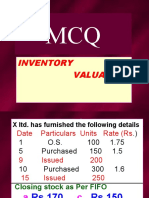

- MCQ Inventory Valuation LBSIMDocumento49 páginasMCQ Inventory Valuation LBSIMSumit SharmaAinda não há avaliações

- Principles of InsuranceDocumento2 páginasPrinciples of Insurancepsawant77Ainda não há avaliações

- Amalgamation, Absorption & External Reconstruction: Chapter-IDocumento9 páginasAmalgamation, Absorption & External Reconstruction: Chapter-Iayushi aggarwalAinda não há avaliações

- Legal Aspects of Business 2 MarksDocumento7 páginasLegal Aspects of Business 2 MarksSivagnanaAinda não há avaliações

- Chapter 26 MCQs On International TaxationDocumento26 páginasChapter 26 MCQs On International TaxationSuranjali Tiwari100% (1)

- Xii Mcqs CH - 6 Retirement of A PartnerDocumento6 páginasXii Mcqs CH - 6 Retirement of A PartnerJoanna GarciaAinda não há avaliações

- It MCQDocumento31 páginasIt MCQbigbulleye6078Ainda não há avaliações

- CRV Goodwill MCQDocumento9 páginasCRV Goodwill MCQMital ParmarAinda não há avaliações

- Debentures ProjectDocumento28 páginasDebentures ProjectMT RA100% (1)

- Questions Paper 399-406Documento8 páginasQuestions Paper 399-406s4sahithAinda não há avaliações

- MCQ'S (Multiple Choice Questions)Documento19 páginasMCQ'S (Multiple Choice Questions)Shubham SinghAinda não há avaliações

- MCQS 8Documento6 páginasMCQS 8Muhammad Usama KhanAinda não há avaliações

- LeasingDocumento6 páginasLeasingSamar MalikAinda não há avaliações

- MRO Procurement Solutions A Complete Guide - 2020 EditionNo EverandMRO Procurement Solutions A Complete Guide - 2020 EditionAinda não há avaliações

- 6 - SwapDocumento29 páginas6 - SwapPratik KhetanAinda não há avaliações

- 6 - SwapDocumento29 páginas6 - SwapnishantAinda não há avaliações

- The Philippine Society: Class StructureDocumento4 páginasThe Philippine Society: Class StructureJaymar Sardz VillarminoAinda não há avaliações

- Problem SetDocumento14 páginasProblem SetVin PheakdeyAinda não há avaliações

- Basic Economic Problem PDFDocumento3 páginasBasic Economic Problem PDFMarvin Angcay AmancioAinda não há avaliações

- Benihana of Tokyo Analysis of CaseDocumento3 páginasBenihana of Tokyo Analysis of CaseAli KhanAinda não há avaliações

- Complete Exhibit 3. Provide The Answers in A Table FormatDocumento5 páginasComplete Exhibit 3. Provide The Answers in A Table FormatSajan Jose100% (2)

- Portuguese Economic Performance 1250-2000Documento17 páginasPortuguese Economic Performance 1250-2000Paula Danielle SilvaAinda não há avaliações

- EU: Quicklime, Slaked Lime and Hydraulic Lime - Market Report. Analysis and Forecast To 2020Documento10 páginasEU: Quicklime, Slaked Lime and Hydraulic Lime - Market Report. Analysis and Forecast To 2020IndexBox MarketingAinda não há avaliações

- E-Marketing Plan For WalmartDocumento10 páginasE-Marketing Plan For WalmartAfrin Sumaiya100% (2)

- Lecture 9. ARIMA ModelsDocumento16 páginasLecture 9. ARIMA ModelsPrarthana PAinda não há avaliações

- Syllabi of B.voc. (Retail Management) 2014-15Documento38 páginasSyllabi of B.voc. (Retail Management) 2014-15Bikalpa BoraAinda não há avaliações

- Econ 2000 Exam 2Documento11 páginasEcon 2000 Exam 2Peyton LawrenceAinda não há avaliações

- The Wealth of NationsDocumento2 páginasThe Wealth of NationsJosé CAinda não há avaliações

- Salient Features of Keynes Theory of Income & EmploymentDocumento8 páginasSalient Features of Keynes Theory of Income & EmploymentHabib urrehmanAinda não há avaliações

- 6 Pricing Understanding and Capturing Customer ValueDocumento27 páginas6 Pricing Understanding and Capturing Customer ValueShadi JabbourAinda não há avaliações

- Design in Search of Roots An Indian Experience Uday AthavankarDocumento16 páginasDesign in Search of Roots An Indian Experience Uday AthavankarPriyanka MokkapatiAinda não há avaliações

- ICT London Kill ZoneDocumento3 páginasICT London Kill Zoneazhar500100% (3)

- REAL 4000 Ch3 HW SolutionsDocumento6 páginasREAL 4000 Ch3 HW SolutionsnunyabiznessAinda não há avaliações

- Eco Prakash PDFDocumento10 páginasEco Prakash PDFPanwar SurajAinda não há avaliações

- Term Paper-02 Business MathematicsDocumento8 páginasTerm Paper-02 Business MathematicsZamiar ShamsAinda não há avaliações

- ECO111 - Individual Assignment 03Documento3 páginasECO111 - Individual Assignment 03Khánh LyAinda não há avaliações

- 50 ArticleText 168 1 10 20200331Documento11 páginas50 ArticleText 168 1 10 20200331FajrinAinda não há avaliações

- Handout Porter's Diamond ModelDocumento2 páginasHandout Porter's Diamond ModelAbraham ZeusAinda não há avaliações

- UT Dallas Syllabus For Ob7300.001.07f Taught by Richard Harrison (Harrison)Documento5 páginasUT Dallas Syllabus For Ob7300.001.07f Taught by Richard Harrison (Harrison)UT Dallas Provost's Technology GroupAinda não há avaliações

- Case 5Documento4 páginasCase 5ad1gamer100% (1)

- Icmap Sma SyllabusDocumento2 páginasIcmap Sma SyllabusAdeel AbbasAinda não há avaliações

- Lecture 12 - Recap (Solutions)Documento19 páginasLecture 12 - Recap (Solutions)Stefano BottariAinda não há avaliações

- Topic 1 Introduction To Financial Markets: Universidad Carlos III Financial EconomicsDocumento19 páginasTopic 1 Introduction To Financial Markets: Universidad Carlos III Financial EconomicsalbroAinda não há avaliações

- CV Tarun Das For Monitoring and Evaluation Expert July 2016Documento9 páginasCV Tarun Das For Monitoring and Evaluation Expert July 2016Professor Tarun DasAinda não há avaliações

- Strategy Implementation at Functional LevelDocumento14 páginasStrategy Implementation at Functional Levelpopat vishal100% (1)

- J. Dimaampao Notes PDFDocumento42 páginasJ. Dimaampao Notes PDFAhmad Deedatt Kalbit100% (1)