Você também pode gostar

- Letter of Credit Appraisal NoteDocumento8 páginasLetter of Credit Appraisal NoteNimitt ChoudharyAinda não há avaliações

- Cutting plastics pollution: Financial measures for a more circular value chainNo EverandCutting plastics pollution: Financial measures for a more circular value chainAinda não há avaliações

- Assessment of Working Capital Finance 95MIKGBVDocumento31 páginasAssessment of Working Capital Finance 95MIKGBVpankaj_xaviers100% (1)

- Assessment of Working Capital LimitDocumento4 páginasAssessment of Working Capital LimitKeshav Malpani100% (8)

- Company: IDFC Project Cost Years 2003 2004 2005 2006 2007 2008 2009 2010 ProjectedDocumento68 páginasCompany: IDFC Project Cost Years 2003 2004 2005 2006 2007 2008 2009 2010 Projectedsumit_sagarAinda não há avaliações

- Working Capital: BY R.K.GuptaDocumento29 páginasWorking Capital: BY R.K.GuptaR.K.GUPTAAinda não há avaliações

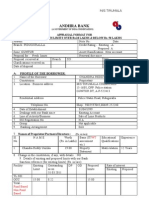

- Andhra Bank: Appraisal Format For Advances With Limits Over Rs.10 Lakhs & Below Rs. 50 LakhsDocumento9 páginasAndhra Bank: Appraisal Format For Advances With Limits Over Rs.10 Lakhs & Below Rs. 50 LakhsSivaramakrishna NeelamAinda não há avaliações

- Assessment of Working CapitalDocumento43 páginasAssessment of Working CapitalAshutosh VermaAinda não há avaliações

- KCC CompleteDocumento94 páginasKCC CompleteRonit HrishikeshAinda não há avaliações

- Non-Banking Finance Companies (NBFCS) : Vivek Sharma Instructor Indian Financial SystemDocumento24 páginasNon-Banking Finance Companies (NBFCS) : Vivek Sharma Instructor Indian Financial Systemviveksharma51Ainda não há avaliações

- Loan CalculatorDocumento15 páginasLoan CalculatorMahrukh ZubairAinda não há avaliações

- XX Credit Appraisal Project FinalDocumento40 páginasXX Credit Appraisal Project FinalDhaval ShahAinda não há avaliações

- PNB Process NoteDocumento36 páginasPNB Process NotePawan BagrechaAinda não há avaliações

- Annexure - Common Loan Application Form With Formats I, II and III-EnglishDocumento12 páginasAnnexure - Common Loan Application Form With Formats I, II and III-EnglishThe LoanWalaAinda não há avaliações

- Kumar Proposal For Enhancement 27-32Documento34 páginasKumar Proposal For Enhancement 27-32Chanderparkash Arora0% (1)

- Registration With SEBI As Merchant Banker and Other MaterialDocumento5 páginasRegistration With SEBI As Merchant Banker and Other Materialapi-3727090100% (3)

- General Guidelines On Loans & Advance: Sachin Katiyar-Chief ManagerDocumento53 páginasGeneral Guidelines On Loans & Advance: Sachin Katiyar-Chief Managersaurabh_shrutiAinda não há avaliações

- MSME SchemesDocumento53 páginasMSME SchemesKalyani BorkarAinda não há avaliações

- Questions: Company BackgroundDocumento5 páginasQuestions: Company BackgroundVia Samantha de AustriaAinda não há avaliações

- Change of Address FormDocumento1 páginaChange of Address FormgenesissinghAinda não há avaliações

- Term Loan Appraisal: A New Manufacturing Unit Wants A Term Loan - Will The Bank Appraise It ?Documento39 páginasTerm Loan Appraisal: A New Manufacturing Unit Wants A Term Loan - Will The Bank Appraise It ?Omkar VedpathakAinda não há avaliações

- Sme WC AssessmentDocumento8 páginasSme WC Assessmentvalinciamarget72Ainda não há avaliações

- Executive SummaryDocumento7 páginasExecutive SummaryHirdayraj Saroj100% (1)

- Maximum Permissible Bank Finance PDFDocumento7 páginasMaximum Permissible Bank Finance PDFitrrustAinda não há avaliações

- Credit Appraisal Process GRP 10Documento18 páginasCredit Appraisal Process GRP 10Priya JagtapAinda não há avaliações

- And Long Term" Which Is Accomplished During The Training Bank of Baroda, SME LOANDocumento246 páginasAnd Long Term" Which Is Accomplished During The Training Bank of Baroda, SME LOANkanchanmbmAinda não há avaliações

- Ubi Process Note of Shourya Virat Trading CompanyDocumento11 páginasUbi Process Note of Shourya Virat Trading CompanyTripurari KumarAinda não há avaliações

- 166-2020 Roi PDFDocumento47 páginas166-2020 Roi PDFANJAN SINGH 3AAinda não há avaliações

- Credit AppraisalDocumento94 páginasCredit AppraisalpratikshaAinda não há avaliações

- Micro, Small & Medium EnterpriseDocumento27 páginasMicro, Small & Medium EnterpriseniyatiAinda não há avaliações

- Uco BankDocumento77 páginasUco BankSankalp PurwarAinda não há avaliações

- Promotion Study Material I To II and II To III-1Documento131 páginasPromotion Study Material I To II and II To III-1Shuvajoy ChakrabortyAinda não há avaliações

- NBFCDocumento32 páginasNBFCPINALAinda não há avaliações

- Credit AppraisalDocumento12 páginasCredit AppraisalAishwarya KrishnanAinda não há avaliações

- Cma For Less Than 1 Crore With CalculationDocumento18 páginasCma For Less Than 1 Crore With CalculationRajkumar NateshanAinda não há avaliações

- "Non-Banking Finance Companies": Presented by Riddhi Ashar Liaquat Ali Manmeet KaurDocumento19 páginas"Non-Banking Finance Companies": Presented by Riddhi Ashar Liaquat Ali Manmeet KaurRohit AggarwalAinda não há avaliações

- BPCL ProjectDocumento50 páginasBPCL ProjectSaurabh Ranjan100% (3)

- Finacle Commands - BankDocumento5 páginasFinacle Commands - BankAmit Malshe0% (1)

- Agenda 15 - Transaction Limits in CBS System For Different Types of TransactionsDocumento13 páginasAgenda 15 - Transaction Limits in CBS System For Different Types of TransactionsJay MeskaAinda não há avaliações

- Commercial Credit Information Report (CCR) - GuideDocumento22 páginasCommercial Credit Information Report (CCR) - Guidecyber ageAinda não há avaliações

- HDFC Bank CAMELS AnalysisDocumento15 páginasHDFC Bank CAMELS Analysisprasanthgeni22Ainda não há avaliações

- Overview of Credit AppraisalDocumento14 páginasOverview of Credit AppraisalAsim MahatoAinda não há avaliações

- Master Circular KCCDocumento16 páginasMaster Circular KCCVaibhav PandeyAinda não há avaliações

- Appraisal Note For Fresh/renewal /enhancement of MSME Loans of Less Than Rs. 100 Lakhs (Total Limit) - Other Than MUDRA LoansDocumento18 páginasAppraisal Note For Fresh/renewal /enhancement of MSME Loans of Less Than Rs. 100 Lakhs (Total Limit) - Other Than MUDRA LoanskiransaradhiAinda não há avaliações

- Project Report For Bank Loan - FormatDocumento1 páginaProject Report For Bank Loan - FormatvidyutAinda não há avaliações

- SBI Credit Appraisal ProcessDocumento123 páginasSBI Credit Appraisal ProcessVinod DhoneAinda não há avaliações

- Comparative Analysis Report On Npa of Pubic & Private Sector BankDocumento10 páginasComparative Analysis Report On Npa of Pubic & Private Sector BankMBA SEM 3 2019Ainda não há avaliações

- Gold Loan LatestDocumento42 páginasGold Loan LatestNirmal RajAinda não há avaliações

- Raj Bank Ratio Analysis PDFDocumento72 páginasRaj Bank Ratio Analysis PDFRonak VaishnavAinda não há avaliações

- Cosmos Co-Operative Bank: Introducation & HistoryDocumento28 páginasCosmos Co-Operative Bank: Introducation & HistoryMahesh DoijodeAinda não há avaliações

- Mcqs Based On Bank'S Circulars During July, 2021Documento8 páginasMcqs Based On Bank'S Circulars During July, 2021Shilpa JhaAinda não há avaliações

- 1710-Dda 31.05.17Documento53 páginas1710-Dda 31.05.17sunilAinda não há avaliações

- Check List LOANDocumento12 páginasCheck List LOANshushanAinda não há avaliações

- Capital Adequacy Presentation 1Documento16 páginasCapital Adequacy Presentation 1Nafiz Imran DiptoAinda não há avaliações

- Project Report-Study On Credit AppraisalDocumento57 páginasProject Report-Study On Credit AppraisalPramod Serma100% (1)

- PgcWorking Capital AssessmentDocumento39 páginasPgcWorking Capital AssessmentTapan Kumar DasAinda não há avaliações

- Working Capital Management: By: Saptarshi MukherjeeDocumento22 páginasWorking Capital Management: By: Saptarshi MukherjeeRitu RajjAinda não há avaliações

- Working Capital Planing and ManagementDocumento9 páginasWorking Capital Planing and ManagementAshish JainAinda não há avaliações

- Appendix 2 Assessment of Working Capital Requirement:: (A) Justification For Estimated / Projected SalesDocumento55 páginasAppendix 2 Assessment of Working Capital Requirement:: (A) Justification For Estimated / Projected SaleskhetaramAinda não há avaliações

- Crimea Case StudyDocumento19 páginasCrimea Case StudyNoyonika DeyAinda não há avaliações

- Office Functions - SDO - OSDS - v2 PDFDocumento6 páginasOffice Functions - SDO - OSDS - v2 PDFtiny aAinda não há avaliações

- Revised AIS Rule Vol I Rule 23Documento7 páginasRevised AIS Rule Vol I Rule 23Shyam MishraAinda não há avaliações

- Graphic Arts Printing and Publishing Award Ma000026 Pay GuideDocumento60 páginasGraphic Arts Printing and Publishing Award Ma000026 Pay GuideJordan MiddletonAinda não há avaliações

- Chan v. ChanDocumento3 páginasChan v. ChanChimney sweepAinda não há avaliações

- Audcise NotesDocumento3 páginasAudcise NotesdfsdAinda não há avaliações

- Invitations & Replies-1Documento14 páginasInvitations & Replies-1ADITYA PRATAPAinda não há avaliações

- America The Story of Us Episode 3 Westward WorksheetDocumento1 páginaAmerica The Story of Us Episode 3 Westward WorksheetHugh Fox III100% (1)

- Shweta Tech RecruiterDocumento2 páginasShweta Tech RecruiterGuar GumAinda não há avaliações

- Ifrs25122 PDFDocumento548 páginasIfrs25122 PDFAmit Kemani100% (1)

- Hiring List FGDocumento6 páginasHiring List FGFaisal Aziz Malghani100% (1)

- A 53Documento15 páginasA 53annavikasAinda não há avaliações

- Astm A391-A391m-07Documento3 páginasAstm A391-A391m-07NadhiraAinda não há avaliações

- Unravelling Taboos-Gender and Sexuality in NamibiaDocumento376 páginasUnravelling Taboos-Gender and Sexuality in NamibiaPetrus Kauluma Shimweefeleni KingyAinda não há avaliações

- Christian Living Module 5Documento10 páginasChristian Living Module 5Hanna Isabelle Malacca GonzalesAinda não há avaliações

- Ringkasan KesDocumento2 páginasRingkasan Kesaz_zafirahAinda não há avaliações

- The Top 11 Small Business Startup Costs To Budget ForDocumento4 páginasThe Top 11 Small Business Startup Costs To Budget ForRamu KakaAinda não há avaliações

- FERC Complaint Request Fast TrackDocumento116 páginasFERC Complaint Request Fast TrackThe PetroglyphAinda não há avaliações

- Helsb Copperbelt Advert 2023 2024Documento1 páginaHelsb Copperbelt Advert 2023 2024kasondekalubaAinda não há avaliações

- Joseph Burstyn, Inc. v. Wilson (1951)Documento6 páginasJoseph Burstyn, Inc. v. Wilson (1951)mpopescuAinda não há avaliações

- Resources Mechanical AESSEAL Guides OEMDocumento147 páginasResources Mechanical AESSEAL Guides OEMhufuents-1100% (2)

- SESSIONAL - PAPER - No 14 2012 PDFDocumento134 páginasSESSIONAL - PAPER - No 14 2012 PDFjohnAinda não há avaliações

- Xat Application Form 2021Documento3 páginasXat Application Form 2021Charlie GoyalAinda não há avaliações

- Saep 134Documento5 páginasSaep 134Demac SaudAinda não há avaliações

- Subject Mark: Education Notification 2020-2021Documento1 páginaSubject Mark: Education Notification 2020-2021ghyjhAinda não há avaliações

- 01 ONG-CHIA-vs-REPUBLICDocumento3 páginas01 ONG-CHIA-vs-REPUBLICMaria Victoria Dela TorreAinda não há avaliações

- God's FaithfulnessDocumento6 páginasGod's FaithfulnessAlbert CondinoAinda não há avaliações

- Military Subjects/Knowledge 11 General OrdersDocumento2 páginasMilitary Subjects/Knowledge 11 General Ordersnicole3esmendaAinda não há avaliações

- PhptoDocumento13 páginasPhptoAshley Jovel De GuzmanAinda não há avaliações

- Redmi Note Bill 1Documento1 páginaRedmi Note Bill 1Mohan Pathak0% (1)