Você também pode gostar

- Megan Jenkins Gemini StatementDocumento2 páginasMegan Jenkins Gemini StatementJonathan Seagull LivingstonAinda não há avaliações

- Information SheetDocumento38 páginasInformation SheetRoy SumugatAinda não há avaliações

- Canadian Payment Systems Modernization-By Srikanth Ex TCSDocumento21 páginasCanadian Payment Systems Modernization-By Srikanth Ex TCSRedSunAinda não há avaliações

- Synopsis Inside JobDocumento1 páginaSynopsis Inside JobmehaksaeedAinda não há avaliações

- 3 BBDocumento2 páginas3 BBKomgit ChantachoteAinda não há avaliações

- Cross Currency Basis - RBS PDFDocumento7 páginasCross Currency Basis - RBS PDFJaz MAinda não há avaliações

- Banking Law NotesDocumento49 páginasBanking Law NotesABINASH NRUSINGHAAinda não há avaliações

- Chapter 1banking and Isurance Calicut UniversirtyDocumento47 páginasChapter 1banking and Isurance Calicut UniversirtyJuManHaqZzAinda não há avaliações

- Chapter 02Documento24 páginasChapter 02JuManHaqZzAinda não há avaliações

- Indian Banking StructureDocumento20 páginasIndian Banking Structureneha16septAinda não há avaliações

- Principles OF Banking - 1Documento36 páginasPrinciples OF Banking - 1Pulkit_Saini_789Ainda não há avaliações

- Unit 6Documento107 páginasUnit 6Avinaash PraveenAinda não há avaliações

- Unit 1Documento57 páginasUnit 1Anurag VarmaAinda não há avaliações

- CBSE Class 11 Accounting-Banking TransactionsDocumento34 páginasCBSE Class 11 Accounting-Banking TransactionsRudraksh PareyAinda não há avaliações

- Banking: Prof. Rahul Mailcontractor Assistant Professor, Jain College of MCA and MBA, BelgaumDocumento69 páginasBanking: Prof. Rahul Mailcontractor Assistant Professor, Jain College of MCA and MBA, BelgaumhakecAinda não há avaliações

- Banking System: An OverviewDocumento22 páginasBanking System: An OverviewPankajAinda não há avaliações

- Banking StructureDocumento11 páginasBanking Structureaditi_espeaksAinda não há avaliações

- Introduction To Indian Banking SystemDocumento78 páginasIntroduction To Indian Banking SystemJessina JoyAinda não há avaliações

- Unit 1 Introduction To BankingDocumento34 páginasUnit 1 Introduction To BankingLalit AyerAinda não há avaliações

- Mrs Ekta Saraswat Assistant Professor (Finance) : Prepared byDocumento69 páginasMrs Ekta Saraswat Assistant Professor (Finance) : Prepared byEkta Saraswat VigAinda não há avaliações

- Banking System in IndiaDocumento4 páginasBanking System in Indiaanirudha.kanhaAinda não há avaliações

- Banking in IndiaDocumento13 páginasBanking in IndiaMurahari NAAinda não há avaliações

- INVESTMENT AND COMPETITION LAW - Unit 2Documento62 páginasINVESTMENT AND COMPETITION LAW - Unit 2saif aliAinda não há avaliações

- Banking Process and Basics of Operations.Documento34 páginasBanking Process and Basics of Operations.amritaa chaurrasiaAinda não há avaliações

- Banking 1Documento69 páginasBanking 1Shaifali GargAinda não há avaliações

- BANKINGDocumento14 páginasBANKINGpinky NathAinda não há avaliações

- Banking Mob 1Documento79 páginasBanking Mob 1Deepak TandonAinda não há avaliações

- BifsDocumento128 páginasBifsSATISH RAJUAinda não há avaliações

- Banking Unit 1Documento69 páginasBanking Unit 1Shaifali ChauhanAinda não há avaliações

- Banking: Prepared by DR Deepak Tandon IMI New DelhiDocumento118 páginasBanking: Prepared by DR Deepak Tandon IMI New Delhidev mhaispurkarAinda não há avaliações

- Principles and Practices of BankingDocumento63 páginasPrinciples and Practices of BankingbasuAinda não há avaliações

- BankDocumento62 páginasBankashishshuklaonlineAinda não há avaliações

- Indian Banking Sector & Nabard, Sidbi, Exim & NHBDocumento32 páginasIndian Banking Sector & Nabard, Sidbi, Exim & NHBramixudinAinda não há avaliações

- Banking ServicesDocumento64 páginasBanking ServicessunsignAinda não há avaliações

- Unit 1 Introduction To BankingDocumento27 páginasUnit 1 Introduction To BankingRandom HeroAinda não há avaliações

- Intoduction To BankingDocumento41 páginasIntoduction To BankingAbhilash ShahAinda não há avaliações

- Devast IncDocumento19 páginasDevast IncPiyush SharmaAinda não há avaliações

- Types of BanksDocumento20 páginasTypes of BanksYog MehtaAinda não há avaliações

- Ufi M 4Documento42 páginasUfi M 4sresthapatel28Ainda não há avaliações

- The Banking IndustryDocumento29 páginasThe Banking IndustryPratik MehtaAinda não há avaliações

- Unit 1 Banking and InsuranceDocumento57 páginasUnit 1 Banking and InsuranceAkankshya Kaushik MishraAinda não há avaliações

- History 2Documento5 páginasHistory 2bickyboom96Ainda não há avaliações

- Bank & Its ClassificationDocumento20 páginasBank & Its ClassificationMansha KakkarAinda não há avaliações

- Lecture TwoDocumento28 páginasLecture TwoHAFIDHI SAIDIAinda não há avaliações

- Financial Institutions & MarketsDocumento62 páginasFinancial Institutions & MarketsSaurav UchilAinda não há avaliações

- Indian Banking System History and StructureDocumento47 páginasIndian Banking System History and StructureRahul SinghAinda não há avaliações

- L7 Financial Intermediaries - Banks & NBFCsDocumento32 páginasL7 Financial Intermediaries - Banks & NBFCssonamsri76Ainda não há avaliações

- Commercial Banking NotesDocumento68 páginasCommercial Banking NotesG NagarajanAinda não há avaliações

- Commercial Bank ManagemntDocumento37 páginasCommercial Bank ManagemntPriya KalaAinda não há avaliações

- Indian Banking Sector: History, Types,& Challenging FactorsDocumento14 páginasIndian Banking Sector: History, Types,& Challenging Factorsrahulims4345980% (1)

- Role of Commercial Banks in IndiaDocumento31 páginasRole of Commercial Banks in IndiaRanzyAinda não há avaliações

- HDFCDocumento61 páginasHDFCpatyal20100% (1)

- Indian Banking .. ..SECTORDocumento30 páginasIndian Banking .. ..SECTORShakshi Arvind GuptaAinda não há avaliações

- Role of Commercial Banks in IndiaDocumento24 páginasRole of Commercial Banks in IndiakanikaAinda não há avaliações

- Structure of Commercial Banking in IndiaDocumento20 páginasStructure of Commercial Banking in IndiaNikhil MunjalAinda não há avaliações

- History of Banking 5Documento19 páginasHistory of Banking 5Ravneet SinghAinda não há avaliações

- Module-4 Types of Bank: Sheetal ThomasDocumento54 páginasModule-4 Types of Bank: Sheetal ThomasSheetal ThomasAinda não há avaliações

- Overview of Banking SystemDocumento45 páginasOverview of Banking SystemShabri MayekarAinda não há avaliações

- What Is: Financial System?Documento13 páginasWhat Is: Financial System?snfrh21Ainda não há avaliações

- Bank LegislationDocumento40 páginasBank LegislationPramil AnandAinda não há avaliações

- Commercial Banking in PakistanDocumento24 páginasCommercial Banking in PakistanMuhammad RadeelAinda não há avaliações

- Interview QuestionDocumento73 páginasInterview Questionaditya0004Ainda não há avaliações

- Banking India: Accepting Deposits for the Purpose of LendingNo EverandBanking India: Accepting Deposits for the Purpose of LendingAinda não há avaliações

- E CRMDocumento4 páginasE CRMChandni Parikh100% (1)

- SMDocumento10 páginasSMChandni ParikhAinda não há avaliações

- BEST (Bus)Documento4 páginasBEST (Bus)Chandni ParikhAinda não há avaliações

- Presentation 2Documento1 páginaPresentation 2AlkaAinda não há avaliações

- Presentation 2Documento1 páginaPresentation 2AlkaAinda não há avaliações

- Presentation 2Documento1 páginaPresentation 2AlkaAinda não há avaliações

- BEST (Bus)Documento4 páginasBEST (Bus)Chandni ParikhAinda não há avaliações

- BS20B004 BS20B029Documento12 páginasBS20B004 BS20B029Ahire Ganesh Ravindra bs20b004Ainda não há avaliações

- Chinese Companies On U.S. Stock Exchanges PDFDocumento12 páginasChinese Companies On U.S. Stock Exchanges PDFBruno MilenoAinda não há avaliações

- Bank Mandiri: 9M21 Review: Strong Earnings Growth ContinuesDocumento8 páginasBank Mandiri: 9M21 Review: Strong Earnings Growth ContinuesdkdehackerAinda não há avaliações

- Colegio de Dagupan Arellano Street, Dagupan City School of Business and Accountancy Preliminary Examination Auditing TheoryDocumento18 páginasColegio de Dagupan Arellano Street, Dagupan City School of Business and Accountancy Preliminary Examination Auditing TheoryFeelingerang MAYoraAinda não há avaliações

- Introduction To AccountingDocumento13 páginasIntroduction To AccountingGrow GlutesAinda não há avaliações

- Statement of Account: Summary of Charges and CreditsDocumento3 páginasStatement of Account: Summary of Charges and CreditsRonnel TattaoAinda não há avaliações

- Book-Keeping Form Three PDFDocumento4 páginasBook-Keeping Form Three PDFdesa ntosAinda não há avaliações

- Tutorial 9 FMTDocumento5 páginasTutorial 9 FMTNguyễn Vĩnh TháiAinda não há avaliações

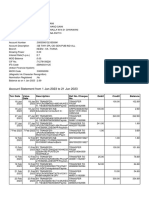

- Account Statement From 1 Jan 2023 To 21 Jun 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocumento6 páginasAccount Statement From 1 Jan 2023 To 21 Jun 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceKumar SunilAinda não há avaliações

- FRI AssignmentDocumento18 páginasFRI AssignmentHaider SaleemAinda não há avaliações

- Lecture No. 2 - Financial Statements & Illustrative ProblemDocumento6 páginasLecture No. 2 - Financial Statements & Illustrative ProblemJA LAYUG100% (1)

- OSX FinancialAccounting ISM Ch12Documento40 páginasOSX FinancialAccounting ISM Ch12eynullabeyliseymurAinda não há avaliações

- Menu Menus NewDocumento238 páginasMenu Menus NewVanitha raoAinda não há avaliações

- SBI Life - Smart Champ Insurance - V03 - Policy Document - Form 594Documento42 páginasSBI Life - Smart Champ Insurance - V03 - Policy Document - Form 594Kia PottsAinda não há avaliações

- CSIS, Innovations in Guarantees For Development, 2019Documento61 páginasCSIS, Innovations in Guarantees For Development, 2019yogesh parajuliAinda não há avaliações

- NF Company IncorporationDocumento29 páginasNF Company Incorporationpirater.ak.47Ainda não há avaliações

- Cost Accounting System: TopicDocumento2 páginasCost Accounting System: Topicsamartha umbareAinda não há avaliações

- 05 Laboratory Exercise 1Documento2 páginas05 Laboratory Exercise 1Praisen JoyAinda não há avaliações

- Money and CreditDocumento14 páginasMoney and CreditRajau RajputanaAinda não há avaliações

- Cabuyao City Executive Summary 2019Documento13 páginasCabuyao City Executive Summary 2019borgygavinaAinda não há avaliações

- Chapter 6 - Principles Products Services of IFDocumento54 páginasChapter 6 - Principles Products Services of IFYaaga DharsiniAinda não há avaliações

- BBB Textile Industries Forensic Audirt ReportDocumento5 páginasBBB Textile Industries Forensic Audirt Reportanita.pariharAinda não há avaliações

- ED FAS On Presentation and Disclsoure in The FS of Takaful Institutions FinalDocumento30 páginasED FAS On Presentation and Disclsoure in The FS of Takaful Institutions FinalIstiaqueAinda não há avaliações