Você também pode gostar

- Income Under The Head Capital Gains' and Its ComputationDocumento12 páginasIncome Under The Head Capital Gains' and Its Computationmanju09535Ainda não há avaliações

- Capital Gains: Dr. Sugandh RawalDocumento41 páginasCapital Gains: Dr. Sugandh RawalAnshu kumarAinda não há avaliações

- Income From Capital Gain by Vishal GoelDocumento57 páginasIncome From Capital Gain by Vishal Goelgoel76vishal100% (1)

- Capital GainDocumento11 páginasCapital GainSiddharth VaswaniAinda não há avaliações

- Capital Gains: Mutual AgreementDocumento3 páginasCapital Gains: Mutual AgreementManas MohapatraAinda não há avaliações

- Short Term and Long Term: by - Chaksh SharmaDocumento17 páginasShort Term and Long Term: by - Chaksh SharmaSushAnt SenAinda não há avaliações

- Capital GainDocumento16 páginasCapital Gainsonibhimsingh100% (2)

- Capital Gains1Documento56 páginasCapital Gains1api-3832224100% (3)

- 27 Capital Gain PCCDocumento44 páginas27 Capital Gain PCCbshah1989Ainda não há avaliações

- Capital Gain Tax in Special Cases: Presented By: Kartik Tripathi (A017), Suhail Desai (A028), Vaibhav Kumar (A030)Documento19 páginasCapital Gain Tax in Special Cases: Presented By: Kartik Tripathi (A017), Suhail Desai (A028), Vaibhav Kumar (A030)Kartik TripathiAinda não há avaliações

- Income Tax ProjectDocumento8 páginasIncome Tax ProjectMs DhoniAinda não há avaliações

- Income Under The Head Capital GainsDocumento15 páginasIncome Under The Head Capital GainsHudson ManuelAinda não há avaliações

- Treatment of Income From Different SourcesDocumento15 páginasTreatment of Income From Different Sourcesdik_gAinda não há avaliações

- Capital GainDocumento38 páginasCapital GainD. Naarayan NandanAinda não há avaliações

- Capital Gains: Chap TerDocumento19 páginasCapital Gains: Chap TerMuskanAinda não há avaliações

- Capital Gains: Presented by Dr. N.K.GuptaDocumento53 páginasCapital Gains: Presented by Dr. N.K.Guptakeshav956Ainda não há avaliações

- Capital Gain: Unit IIIDocumento44 páginasCapital Gain: Unit IIIvikas_is_stupidAinda não há avaliações

- Capital GainDocumento32 páginasCapital GainswajanAinda não há avaliações

- Capital Gains 1Documento46 páginasCapital Gains 1NIRAVAinda não há avaliações

- What Is Capital GainDocumento7 páginasWhat Is Capital GainAli NadafAinda não há avaliações

- Capital Gain - Merged-1Documento5 páginasCapital Gain - Merged-1mohitjakhar38Ainda não há avaliações

- Capital GainsDocumento22 páginasCapital GainsAshish BomzanAinda não há avaliações

- Capital GainsDocumento14 páginasCapital GainsshanmukvardhanAinda não há avaliações

- Capital Gainsppt 180105192411Documento58 páginasCapital Gainsppt 180105192411ozairsaiyedAinda não há avaliações

- Capital GainDocumento13 páginasCapital GainSaurav MedhiAinda não há avaliações

- Capital Gains Sec 45 To 55aDocumento34 páginasCapital Gains Sec 45 To 55aBeing HumaneAinda não há avaliações

- Capital GainsDocumento64 páginasCapital Gains98690Ainda não há avaliações

- Income Under The Head Capital GainsDocumento71 páginasIncome Under The Head Capital GainsAshish SharmaAinda não há avaliações

- Capital Gains 1Documento55 páginasCapital Gains 1apurvaapurvaAinda não há avaliações

- Capital GainDocumento19 páginasCapital GainGAURAV PRAKASHAinda não há avaliações

- Purpose of ValuationDocumento13 páginasPurpose of ValuationRajwinder Singh BansalAinda não há avaliações

- RealEstateTransactions 3rdsepDocumento118 páginasRealEstateTransactions 3rdsepManish GargAinda não há avaliações

- Capita GainsDocumento3 páginasCapita GainsAdeem AshrafiAinda não há avaliações

- Capital Gains TaxDocumento23 páginasCapital Gains TaxAditi KhaitanAinda não há avaliações

- SyovcgiDocumento19 páginasSyovcgiSHIVAM SAHUAinda não há avaliações

- Capital GainDocumento139 páginasCapital GainManoj YadavAinda não há avaliações

- Income Under The Head Capital GainsDocumento4 páginasIncome Under The Head Capital Gains887 shivam guptaAinda não há avaliações

- Valuation Part2Documento52 páginasValuation Part2Ar Neelesh Kant SaxenaAinda não há avaliações

- Capital Gains NotesDocumento3 páginasCapital Gains NotesDhiraj SoniAinda não há avaliações

- Principle of ValuationDocumento76 páginasPrinciple of Valuationnavneet PatilAinda não há avaliações

- Income Tax Assignment ON Capital GainsDocumento11 páginasIncome Tax Assignment ON Capital GainsHimanshu ThukralAinda não há avaliações

- Capital Gain 8th SemDocumento10 páginasCapital Gain 8th SemAuthor SatyaAinda não há avaliações

- Tax Planning With Regard To Capital GainsDocumento25 páginasTax Planning With Regard To Capital GainsKamraan QuadriAinda não há avaliações

- Capital GainsDocumento27 páginasCapital GainsdeepakadhanaAinda não há avaliações

- FAR-4210 Investment Property & Other Fund Investments: - T R S A ResaDocumento4 páginasFAR-4210 Investment Property & Other Fund Investments: - T R S A ResaEllyssa Ann MorenoAinda não há avaliações

- Lesson 3Documento11 páginasLesson 3devravidhan382Ainda não há avaliações

- Capital Gain AY 2022-23 With SolutionsDocumento15 páginasCapital Gain AY 2022-23 With SolutionsKrish Goel100% (1)

- Computation of Capital GainsDocumento25 páginasComputation of Capital GainsRamya GowdaAinda não há avaliações

- Unit 3 - Capital GainsDocumento32 páginasUnit 3 - Capital GainsVaishnaviAinda não há avaliações

- Chapter 7Documento6 páginasChapter 7vishwanathAinda não há avaliações

- CAPITALGAINS 3rdsep PDFDocumento202 páginasCAPITALGAINS 3rdsep PDFPhani Kumar SomarajupalliAinda não há avaliações

- Income From Capital GainDocumento11 páginasIncome From Capital Gainkomil bogharaAinda não há avaliações

- Slides - Capital GainsDocumento15 páginasSlides - Capital Gainsabhishek bhOoTnAAinda não há avaliações

- Far 46 60Documento27 páginasFar 46 60GuadzAinda não há avaliações

- Tax Notes On Capital GainsDocumento15 páginasTax Notes On Capital GainsGarima GarimaAinda não há avaliações

- Acquirer Obtains Control of One or More Businesses.: ConceptDocumento6 páginasAcquirer Obtains Control of One or More Businesses.: ConceptJohn Lexter MacalberAinda não há avaliações

- Securitized Real Estate and 1031 ExchangesNo EverandSecuritized Real Estate and 1031 ExchangesAinda não há avaliações

- Intermediate Accounting 2: a QuickStudy Digital Reference GuideNo EverandIntermediate Accounting 2: a QuickStudy Digital Reference GuideAinda não há avaliações

- Competition Act, 2002Documento47 páginasCompetition Act, 2002themeditator100% (1)

- Bonus Act - 1965 - 1Documento21 páginasBonus Act - 1965 - 1Satyam mishraAinda não há avaliações

- Clubbing of IncomeDocumento14 páginasClubbing of IncomethemeditatorAinda não há avaliações

- Basicinternalauditing 1255043287052 Phpapp02Documento25 páginasBasicinternalauditing 1255043287052 Phpapp02Liew Chee KiongAinda não há avaliações

- Auditing in Computer Environment Presentation 1224128964994975 8Documento90 páginasAuditing in Computer Environment Presentation 1224128964994975 8themeditator100% (1)

- Accounting Standards: in IndiaDocumento4 páginasAccounting Standards: in IndiathemeditatorAinda não há avaliações

- All About TAX in Financial Year 2009Documento44 páginasAll About TAX in Financial Year 2009themeditatorAinda não há avaliações

- Casually Sit Back and Relax and Enjoy Your Income TaxDocumento125 páginasCasually Sit Back and Relax and Enjoy Your Income TaxthemeditatorAinda não há avaliações

- Accounting Standard - 22Documento25 páginasAccounting Standard - 22themeditator100% (1)

- Auditing and Assurance StandardsDocumento13 páginasAuditing and Assurance StandardsthemeditatorAinda não há avaliações

- Shares Securities PPT Rajesh YadavDocumento42 páginasShares Securities PPT Rajesh YadavthemeditatorAinda não há avaliações

- The Fundamentals of Money Market Instruments in IndiaDocumento53 páginasThe Fundamentals of Money Market Instruments in Indiathemeditator100% (4)

- Accounting and Bookkeeping For Business and Management 13 October 1234091669363945 3Documento19 páginasAccounting and Bookkeeping For Business and Management 13 October 1234091669363945 3themeditatorAinda não há avaliações

- CH 14Documento40 páginasCH 14Cris Ann Marie ESPAnOLAAinda não há avaliações

- 會計科目中英對照表Documento4 páginas會計科目中英對照表yuxuan1228.yxwAinda não há avaliações

- Accounting - Text & Cases - 13 Edition Basic Accounting Concepts: The Balance SheetDocumento7 páginasAccounting - Text & Cases - 13 Edition Basic Accounting Concepts: The Balance SheetV Hemanth KumarAinda não há avaliações

- Unit - 5 DepreciationDocumento19 páginasUnit - 5 DepreciationGeethaAinda não há avaliações

- On June 1 of This Year J Larkin Optometrist Established The Larkin Eye Clinic The ClinicsDocumento3 páginasOn June 1 of This Year J Larkin Optometrist Established The Larkin Eye Clinic The ClinicsCharlotteAinda não há avaliações

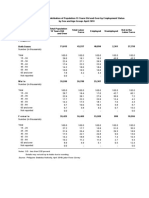

- TABLE 1 Percent Distribution of Population 15 Years Old and Over by Employment Status by Sex and Age Group April 2018Documento19 páginasTABLE 1 Percent Distribution of Population 15 Years Old and Over by Employment Status by Sex and Age Group April 2018RoxanAinda não há avaliações

- Chartered Accountancy Professional Ii (CAP-II) : Education Division The Institute of Chartered Accountants of NepalDocumento81 páginasChartered Accountancy Professional Ii (CAP-II) : Education Division The Institute of Chartered Accountants of NepalPrashant Sagar GautamAinda não há avaliações

- Accounting PrincipleDocumento24 páginasAccounting PrincipleMonirHRAinda não há avaliações

- United Bank Ltd.Documento111 páginasUnited Bank Ltd.Asif Rasool ChannaAinda não há avaliações

- No 3Documento4 páginasNo 3Barbara IgnacioAinda não há avaliações

- Chalk Allowance 2013Documento8 páginasChalk Allowance 2013Jonas Reduta CabacunganAinda não há avaliações

- Investment Office ANRS: Project Profile On The Establishment of Leather Shoe Upper Making PlantDocumento26 páginasInvestment Office ANRS: Project Profile On The Establishment of Leather Shoe Upper Making PlantJohnAinda não há avaliações

- TYtest PaperDocumento2 páginasTYtest PapercnpithadiaAinda não há avaliações

- Answer Key To Fundamentals of Financial Accounting and Reporting CDCDocumento3 páginasAnswer Key To Fundamentals of Financial Accounting and Reporting CDCAprile Margareth HidalgoAinda não há avaliações

- Assignmet For Practice Session StudentsDocumento5 páginasAssignmet For Practice Session StudentsYasir Ahmed Siddiqui0% (1)

- IAS 19 Employment BenefitDocumento18 páginasIAS 19 Employment BenefitSrabon BaruaAinda não há avaliações

- Tax On Idividuals: Practice ProblemsDocumento17 páginasTax On Idividuals: Practice ProblemsLealyn CuestaAinda não há avaliações

- 1 - Accounting Cycle Overview Practice ProblemsDocumento5 páginas1 - Accounting Cycle Overview Practice ProblemsmikeAinda não há avaliações

- FDNACCT - Quiz #1 - Solutions To PS - Set ADocumento2 páginasFDNACCT - Quiz #1 - Solutions To PS - Set AleshamunsayAinda não há avaliações

- Prelim NotesDocumento164 páginasPrelim NotesShaina Monique RangasanAinda não há avaliações

- PG MCA Computer Applications 315 21 Accounting and Financial Management 5777Documento223 páginasPG MCA Computer Applications 315 21 Accounting and Financial Management 5777JOSEPH MATHEW100% (1)

- Shelter PartnershipDocumento3 páginasShelter PartnershipZereen Gail Nievera0% (1)

- 15 - Conclusion and SuggestionDocumento27 páginas15 - Conclusion and SuggestionAjay MatiedaAinda não há avaliações

- PPE Depreciation & ImpairmentDocumento25 páginasPPE Depreciation & ImpairmentSummer Star0% (1)

- Task Force ms13Documento55 páginasTask Force ms13api-615952643Ainda não há avaliações

- IMRADDocumento21 páginasIMRADRosalie RosalesAinda não há avaliações

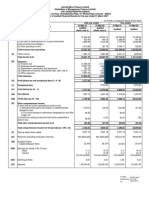

- (In Lakhs, Except Per Equity Share Data) : Digitally Signed Bysvraja VaidyanathanDocumento9 páginas(In Lakhs, Except Per Equity Share Data) : Digitally Signed Bysvraja VaidyanathanAnamika NandiAinda não há avaliações

- Assignment of Fundamental of Accounting IDocumento12 páginasAssignment of Fundamental of Accounting IibsaashekaAinda não há avaliações

- Group 4 Presentation Lect - 04 Overhead AnalysisDocumento25 páginasGroup 4 Presentation Lect - 04 Overhead AnalysisHumphrey OsaigbeAinda não há avaliações

- 210617-1539.1-Sindh Annual Budget Statement For 2021-22 - Volume-IDocumento59 páginas210617-1539.1-Sindh Annual Budget Statement For 2021-22 - Volume-Ishahid aliAinda não há avaliações