Você também pode gostar

- Philippine Accounting Standards 38 (Intangible Assets2)Documento72 páginasPhilippine Accounting Standards 38 (Intangible Assets2)Princess Edreah NuñalAinda não há avaliações

- Lecture Notes Iass 16 EtcDocumento31 páginasLecture Notes Iass 16 Etcmayillahmansaray40Ainda não há avaliações

- C17 - MFRS 116 PpeDocumento15 páginasC17 - MFRS 116 Ppe2022478048Ainda não há avaliações

- Lecture Notes On Revaluation and ImpairmentDocumento6 páginasLecture Notes On Revaluation and Impairmentjudel ArielAinda não há avaliações

- Lecture Notes On Revaluation and Impairment PDFDocumento6 páginasLecture Notes On Revaluation and Impairment PDFjudel ArielAinda não há avaliações

- IAS 16 Property Plant EquipmentDocumento1 páginaIAS 16 Property Plant Equipmentm2mlckAinda não há avaliações

- Ias 16 Ifrs3 Ifrs 5Documento26 páginasIas 16 Ifrs3 Ifrs 5Nearchos A. IoannouAinda não há avaliações

- International Accounting Standard 16Documento100 páginasInternational Accounting Standard 16ClarkMaasAinda não há avaliações

- Accounting Standard 6Documento208 páginasAccounting Standard 6aanu1234Ainda não há avaliações

- Financial Accounting: Indian Institute of Management, RaipurDocumento21 páginasFinancial Accounting: Indian Institute of Management, RaipurJHANVI LAKRAAinda não há avaliações

- PPE Theory-DepDocumento5 páginasPPE Theory-DepDibyansu KumarAinda não há avaliações

- IAS#36Documento31 páginasIAS#36Shah KamalAinda não há avaliações

- Lesson 4Documento23 páginasLesson 4shadowlord468Ainda não há avaliações

- Section 17Documento33 páginasSection 17Abata BageyuAinda não há avaliações

- 10 Week 10 CHPT 14n15 NCADocumento47 páginas10 Week 10 CHPT 14n15 NCA1621995944Ainda não há avaliações

- Session 8 - Valuation of Intangible AssetsDocumento18 páginasSession 8 - Valuation of Intangible AssetsManan AgarwalAinda não há avaliações

- International Accounting Standard 16 Property, Plant and EquipmentDocumento29 páginasInternational Accounting Standard 16 Property, Plant and EquipmentAbdullah Shaker TahaAinda não há avaliações

- Topic 1Documento49 páginasTopic 1TafadzwaAinda não há avaliações

- Accountingstandard 161023112619Documento24 páginasAccountingstandard 161023112619prasadAinda não há avaliações

- Facilitators Guide For Accenture-IGNOU Diploma Program: Unit 4Documento20 páginasFacilitators Guide For Accenture-IGNOU Diploma Program: Unit 4Vinay SinghAinda não há avaliações

- LESSON3Documento19 páginasLESSON3Ira Charisse BurlaosAinda não há avaliações

- Application of Ifrs (Ind As) For Transactions: Unit - 2Documento40 páginasApplication of Ifrs (Ind As) For Transactions: Unit - 2Talla Mokshitha100% (1)

- Fixed Assets AccountingDocumento24 páginasFixed Assets Accountingjayti desaiAinda não há avaliações

- Examender Engl 1Documento23 páginasExamender Engl 1VISHAL PANDYAAinda não há avaliações

- IAS 36 Impairment of AssetsDocumento25 páginasIAS 36 Impairment of AssetsSherif MohamedAinda não há avaliações

- Property, Plant and Equipment IAS 16: Lacpa IFRS PresentationDocumento31 páginasProperty, Plant and Equipment IAS 16: Lacpa IFRS PresentationKenncyAinda não há avaliações

- WebcastAccountingStandardsAS 6,10&28Documento40 páginasWebcastAccountingStandardsAS 6,10&28ArunkumarAinda não há avaliações

- SBR - Chapter 4Documento6 páginasSBR - Chapter 4Jason KumarAinda não há avaliações

- Pertemuan Ke: 16 SC&C Ch-9 LT Assets I: Kode Mata Kuliah: Ea 33401Documento35 páginasPertemuan Ke: 16 SC&C Ch-9 LT Assets I: Kode Mata Kuliah: Ea 33401Alvin HartantioAinda não há avaliações

- IAS 36 Impairment of AssetsDocumento29 páginasIAS 36 Impairment of AssetsEmms Adelaine TulaganAinda não há avaliações

- Ias 36Documento2 páginasIas 36Azeez BidemiAinda não há avaliações

- Accounting Standard 2 and 19Documento8 páginasAccounting Standard 2 and 19Sadhvi BansalAinda não há avaliações

- 9.2 IAS36 - Impairment of Assets 1Documento41 páginas9.2 IAS36 - Impairment of Assets 1Given RefilweAinda não há avaliações

- IAS 16 - Property Plant and EquipmentDocumento35 páginasIAS 16 - Property Plant and EquipmentlaaybaAinda não há avaliações

- Chapter Three: Accounting For General Capital Assets & Capital Project FundsDocumento46 páginasChapter Three: Accounting For General Capital Assets & Capital Project FundsTilahun MikiasAinda não há avaliações

- Financial Reporting Framework For CooperativesDocumento46 páginasFinancial Reporting Framework For CooperativesIsaac joule100% (1)

- Ias 16 - PpeDocumento4 páginasIas 16 - Ppecar itselfAinda não há avaliações

- Fixed Assets, DepreciationDocumento30 páginasFixed Assets, Depreciationnahar570Ainda não há avaliações

- IAS16 Defines Property, Plant and Equipment As "Tangible Items ThatDocumento35 páginasIAS16 Defines Property, Plant and Equipment As "Tangible Items ThatMo HachimAinda não há avaliações

- Accounting Standards: Accounting Standard 1: Disclosure of Accounting PoliciesDocumento5 páginasAccounting Standards: Accounting Standard 1: Disclosure of Accounting PoliciesAnkita GoelAinda não há avaliações

- Accounting For Non-Current AssetsDocumento8 páginasAccounting For Non-Current AssetsvladsteinarminAinda não há avaliações

- Chapter 8 - Operating Assets: Property, Plant, and Equipment, and IntangiblesDocumento9 páginasChapter 8 - Operating Assets: Property, Plant, and Equipment, and IntangiblesHareem Zoya WarsiAinda não há avaliações

- Property, Plant and EquipmentDocumento16 páginasProperty, Plant and EquipmentnurthiwnyAinda não há avaliações

- Ias 38Documento33 páginasIas 38Reever River100% (1)

- PAS IntangibleDocumento21 páginasPAS IntangibleAngela WaganAinda não há avaliações

- PP (A) - Lect 2 - Ias 16 PpeDocumento19 páginasPP (A) - Lect 2 - Ias 16 Ppekevin digumberAinda não há avaliações

- Name:-Akash Jaiswal ROLL NO.:-0645 ROOM NO.:-045 SESSION:-2014-2017 Topic:-Accounting For FixedDocumento6 páginasName:-Akash Jaiswal ROLL NO.:-0645 ROOM NO.:-045 SESSION:-2014-2017 Topic:-Accounting For FixedAKASH JAISWALAinda não há avaliações

- Ias 36 Impairment of Assets-1Documento16 páginasIas 36 Impairment of Assets-1vincentAinda não há avaliações

- Farap 4505Documento7 páginasFarap 4505Marya NvlzAinda não há avaliações

- Ias 16Documento9 páginasIas 16ADEYANJU AKEEMAinda não há avaliações

- Audit of Fixed Assets 1Documento3 páginasAudit of Fixed Assets 1Leon MushiAinda não há avaliações

- PAS 38 Intangible Assets PowerpointDocumento18 páginasPAS 38 Intangible Assets PowerpointYassi CurtisAinda não há avaliações

- Accounting Standards - 10 A F F A: Ccounting OR Ixed SsetsDocumento4 páginasAccounting Standards - 10 A F F A: Ccounting OR Ixed SsetscutejaskiAinda não há avaliações

- Non Current Assets EssayDocumento9 páginasNon Current Assets Essaystorky05600% (1)

- Depreciation: Aromal S A Roll No. 5 Govt. College NedumangadDocumento24 páginasDepreciation: Aromal S A Roll No. 5 Govt. College NedumangadAromalAinda não há avaliações

- Fixed AssetsDocumento46 páginasFixed AssetsSprancenatu Lavinia0% (1)

- DepreciationDocumento16 páginasDepreciationYashi GuptaAinda não há avaliações

- Financial Accounting and Reporting Study Guide NotesNo EverandFinancial Accounting and Reporting Study Guide NotesNota: 1 de 5 estrelas1/5 (1)

- The Entrepreneur’S Dictionary of Business and Financial TermsNo EverandThe Entrepreneur’S Dictionary of Business and Financial TermsAinda não há avaliações

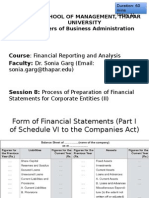

- LMT School of Management, Thapar University Masters of Business AdministrationDocumento23 páginasLMT School of Management, Thapar University Masters of Business Administrationgursimran jit singhAinda não há avaliações

- LMT School of Management, Thapar University Masters of Business AdministrationDocumento14 páginasLMT School of Management, Thapar University Masters of Business Administrationgursimran jit singhAinda não há avaliações

- LMT School of Management, Thapar University Masters of Business AdministrationDocumento9 páginasLMT School of Management, Thapar University Masters of Business Administrationgursimran jit singhAinda não há avaliações

- LMT School of Management, Thapar University Masters of Business AdministrationDocumento11 páginasLMT School of Management, Thapar University Masters of Business Administrationgursimran jit singhAinda não há avaliações

- LMT School of Management, Thapar University Masters of Business AdministrationDocumento17 páginasLMT School of Management, Thapar University Masters of Business Administrationgursimran jit singhAinda não há avaliações

- LMT School of Management, Thapar University Masters of Business AdministrationDocumento9 páginasLMT School of Management, Thapar University Masters of Business Administrationgursimran jit singhAinda não há avaliações

- LMT School of Management, Thapar University Masters of Business AdministrationDocumento18 páginasLMT School of Management, Thapar University Masters of Business Administrationgursimran jit singhAinda não há avaliações

- LMT School of Management, Thapar University Masters of Business AdministrationDocumento21 páginasLMT School of Management, Thapar University Masters of Business Administrationgursimran jit singhAinda não há avaliações

- Session 3Documento13 páginasSession 3gursimran jit singhAinda não há avaliações

- Soybeans (OZS - ZS) OZSU2 Vs 1463.25 - Open Interest ChangeDocumento1 páginaSoybeans (OZS - ZS) OZSU2 Vs 1463.25 - Open Interest ChangeIndranil BanerjeeAinda não há avaliações

- HKUST Canvas - Quiz 2 - FINA1303 (L1) - Introduction To Financial Markets and InstitutionsDocumento10 páginasHKUST Canvas - Quiz 2 - FINA1303 (L1) - Introduction To Financial Markets and InstitutionslauyingsumAinda não há avaliações

- Cgr660 10 LiquidationDocumento39 páginasCgr660 10 Liquidationr4vemasterAinda não há avaliações

- Distributor Manual: A Handbook For Distributors Using Karvy MFS Online ServicesDocumento14 páginasDistributor Manual: A Handbook For Distributors Using Karvy MFS Online Serviceschandrashekhar.verma4025Ainda não há avaliações

- Demerger of BajajDocumento30 páginasDemerger of BajajNikhil100% (1)

- Financial Reporting ICAI Study MaterialDocumento1.821 páginasFinancial Reporting ICAI Study MaterialKrishna Kowshik100% (1)

- Guidebook For European Investors in IndiaDocumento177 páginasGuidebook For European Investors in IndiaWim KrämerAinda não há avaliações

- Chapter 1 - Solution Manual PDFDocumento32 páginasChapter 1 - Solution Manual PDFNatalie ChoiAinda não há avaliações

- Using The Heikin Ashi Technique D ValcuDocumento8 páginasUsing The Heikin Ashi Technique D ValcumodyvicAinda não há avaliações

- Investment Decision Making Between Games Workshop and Hornby Finance EssayDocumento23 páginasInvestment Decision Making Between Games Workshop and Hornby Finance EssayHND Assignment HelpAinda não há avaliações

- (Reviewer - Midterm GoSalTo) Tax 2 PDFDocumento38 páginas(Reviewer - Midterm GoSalTo) Tax 2 PDFHoreb Felix VillaAinda não há avaliações

- MILAOR+ +Province+of+Tarlac+vs.+AlcantaraDocumento3 páginasMILAOR+ +Province+of+Tarlac+vs.+AlcantaraAndrea MilaorAinda não há avaliações

- California Apostile Info and HelpDocumento3 páginasCalifornia Apostile Info and HelpDiana0% (1)

- Strategies LOW VOLATILITYDocumento8 páginasStrategies LOW VOLATILITYbla blaAinda não há avaliações

- Final-Term Quiz Mankeu Roki Fajri 119108077Documento4 páginasFinal-Term Quiz Mankeu Roki Fajri 119108077kota lainAinda não há avaliações

- Uniform Loan and Mortgage Agreement (Real Estate) : Pangasinan Bank, IncDocumento7 páginasUniform Loan and Mortgage Agreement (Real Estate) : Pangasinan Bank, IncCampbell HezekiahAinda não há avaliações

- RSM FinalDocumento29 páginasRSM FinalNihal LamgeAinda não há avaliações

- PNB vs. Delos ReyesDocumento2 páginasPNB vs. Delos ReyesGretchen Dominguez-Zaldivar100% (1)

- Technical Analysis of Indian Stock MarketDocumento62 páginasTechnical Analysis of Indian Stock MarketPritesh PuntambekarAinda não há avaliações

- Tugas ManajemenDocumento226 páginasTugas ManajemenFatwaAinda não há avaliações

- NBFCDocumento7 páginasNBFCRaktima MajumdarAinda não há avaliações

- Trade StoryDocumento12 páginasTrade Storyamos amosAinda não há avaliações

- Equity Bank - Information Memorandum FinalDocumento100 páginasEquity Bank - Information Memorandum FinalsurambayaAinda não há avaliações

- 21 09 21 Tastytrade ResearchDocumento5 páginas21 09 21 Tastytrade ResearchtrungAinda não há avaliações

- Chapter 10 DerivativesDocumento8 páginasChapter 10 DerivativesClaire VensueloAinda não há avaliações

- Amado G. Soriano and Rafael B. Garcia Vs Hon. Ruben B. Ancheta, (G.R. No. 57589. March 18, 1985.) Landmark Case SynopsisDocumento7 páginasAmado G. Soriano and Rafael B. Garcia Vs Hon. Ruben B. Ancheta, (G.R. No. 57589. March 18, 1985.) Landmark Case SynopsisJay Mark Albis SantosAinda não há avaliações

- Form No.92-Affidavit of LossDocumento2 páginasForm No.92-Affidavit of LossMaica PinedaAinda não há avaliações

- Siemens AR 2006 1427558 2Documento147 páginasSiemens AR 2006 1427558 2shashi_k07Ainda não há avaliações

- Syllabus Mba4Documento7 páginasSyllabus Mba4Vishal SoodAinda não há avaliações

- Mayo 10e CH 14Documento20 páginasMayo 10e CH 14Karl Mitzi Faith DalmanAinda não há avaliações