Você também pode gostar

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- Food Safety and Hygiene LayoutDocumento9 páginasFood Safety and Hygiene LayoutJann Kerky100% (1)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- Precision Delivery Inc. Case StudyDocumento2 páginasPrecision Delivery Inc. Case StudyJann Kerky0% (1)

- SFPC Operational Definition InstructionsDocumento2 páginasSFPC Operational Definition InstructionsJann KerkyAinda não há avaliações

- KFC CaseDocumento2 páginasKFC CaseJann KerkyAinda não há avaliações

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Cash BudgetDocumento3 páginasCash BudgetJann Kerky0% (1)

- EbitDocumento3 páginasEbitJann KerkyAinda não há avaliações

- 10 AxiomsDocumento6 páginas10 AxiomsJann KerkyAinda não há avaliações

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

- Horizontal and Vertical Analysis DetailsDocumento9 páginasHorizontal and Vertical Analysis DetailsJann KerkyAinda não há avaliações

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Unsecured ST FinancingDocumento5 páginasUnsecured ST FinancingJann KerkyAinda não há avaliações

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

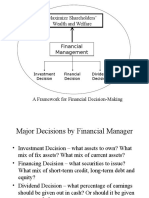

- Maximize Shareholders' Wealth and Welfare: Investment Decision Financial Decision Dividend DecisionDocumento6 páginasMaximize Shareholders' Wealth and Welfare: Investment Decision Financial Decision Dividend DecisionJann KerkyAinda não há avaliações

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Energy TransformationDocumento6 páginasEnergy TransformationJann KerkyAinda não há avaliações

- Accord 2013 BrochureDocumento25 páginasAccord 2013 BrochureJann KerkyAinda não há avaliações

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- Sample FinalDocumento9 páginasSample FinalJann KerkyAinda não há avaliações

- Telfer - Food As ArtDocumento10 páginasTelfer - Food As ArtJann Kerky100% (1)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- Roofing Shingles in KeralaDocumento13 páginasRoofing Shingles in KeralaCertainteed Roofing tilesAinda não há avaliações

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (345)

- Cruz-Arevalo v. Layosa DigestDocumento2 páginasCruz-Arevalo v. Layosa DigestPatricia Ann RueloAinda não há avaliações

- ChitsongChen, Signalsandsystems Afreshlook PDFDocumento345 páginasChitsongChen, Signalsandsystems Afreshlook PDFCarlos_Eduardo_2893Ainda não há avaliações

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- Layos vs. VillanuevaDocumento2 páginasLayos vs. VillanuevaLaura MangantulaoAinda não há avaliações

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- CLASS 12 PracticalDocumento10 páginasCLASS 12 PracticalWORLD HISTORYAinda não há avaliações

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- Data Science Online Workshop Data Science vs. Data AnalyticsDocumento1 páginaData Science Online Workshop Data Science vs. Data AnalyticsGaurav VarshneyAinda não há avaliações

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- Oda A La InmortalidadDocumento7 páginasOda A La InmortalidadEmy OoTeam ClésAinda não há avaliações

- Domestic and Foreign Policy Essay: Immigration: Salt Lake Community CollegeDocumento6 páginasDomestic and Foreign Policy Essay: Immigration: Salt Lake Community Collegeapi-533010636Ainda não há avaliações

- Chapter 9 - PPT (New)Documento43 páginasChapter 9 - PPT (New)Syarifah NourazlinAinda não há avaliações

- Introduction To Political ScienceDocumento18 páginasIntroduction To Political Sciencecyrene cayananAinda não há avaliações

- SpellsDocumento86 páginasSpellsGypsy580% (5)

- Pagan and Wiccan Quotes and GuidanceDocumento8 páginasPagan and Wiccan Quotes and GuidanceStinkyBooAinda não há avaliações

- A/L 2021 Practice Exam - 13 (Combined Mathematics I) : S.No Name Batch School Ad No. Marks RankDocumento12 páginasA/L 2021 Practice Exam - 13 (Combined Mathematics I) : S.No Name Batch School Ad No. Marks RankElectronAinda não há avaliações

- 2019 Ulverstone Show ResultsDocumento10 páginas2019 Ulverstone Show ResultsMegan PowellAinda não há avaliações

- Mirza HRM ProjectDocumento44 páginasMirza HRM Projectsameer82786100% (1)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- Statistical MethodsDocumento4 páginasStatistical MethodsYra Louisse Taroma100% (1)

- 5HP500-590 4139 - 751 - 627dDocumento273 páginas5HP500-590 4139 - 751 - 627ddejanflojd100% (24)

- Framework For Marketing Management Global 6Th Edition Kotler Solutions Manual Full Chapter PDFDocumento33 páginasFramework For Marketing Management Global 6Th Edition Kotler Solutions Manual Full Chapter PDFWilliamThomasbpsg100% (9)

- An Analysis of The PoemDocumento2 páginasAn Analysis of The PoemDayanand Gowda Kr100% (2)

- Conversational Maxims and Some Philosophical ProblemsDocumento15 páginasConversational Maxims and Some Philosophical ProblemsPedro Alberto SanchezAinda não há avaliações

- Introduction To PTC Windchill PDM Essentials 11.1 For Light UsersDocumento6 páginasIntroduction To PTC Windchill PDM Essentials 11.1 For Light UsersJYAinda não há avaliações

- DissertationDocumento59 páginasDissertationFatma AlkindiAinda não há avaliações

- 4 Major Advantages of Japanese Education SystemDocumento3 páginas4 Major Advantages of Japanese Education SystemIsa HafizaAinda não há avaliações

- Stockholm KammarbrassDocumento20 páginasStockholm KammarbrassManuel CoitoAinda não há avaliações

- Leisure TimeDocumento242 páginasLeisure TimeArdelean AndradaAinda não há avaliações

- Psc720-Comparative Politics 005 Political CultureDocumento19 páginasPsc720-Comparative Politics 005 Political CultureGeorge ForcoșAinda não há avaliações

- Designing A Peace Building InfrastructureDocumento253 páginasDesigning A Peace Building InfrastructureAditya SinghAinda não há avaliações

- Grade 3Documento4 páginasGrade 3Shai HusseinAinda não há avaliações

- The Gower Handbook of Project Management: Part 1: ProjectsDocumento2 páginasThe Gower Handbook of Project Management: Part 1: ProjectschineduAinda não há avaliações

- Claribel Ria MaeDocumento19 páginasClaribel Ria MaeGLENN MENDOZAAinda não há avaliações