Você também pode gostar

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- Sample Barista Offer LetterDocumento2 páginasSample Barista Offer LetterMohammed Albalushi100% (2)

- ProjectLookingGlassDeclassified PDFDocumento13 páginasProjectLookingGlassDeclassified PDFAmi Ferguson83% (6)

- Maruti FinalDocumento23 páginasMaruti FinalYash MangeAinda não há avaliações

- Chapter 3 MethodologyDocumento22 páginasChapter 3 MethodologySiva KrishnaAinda não há avaliações

- Deviation Control MethodsDocumento4 páginasDeviation Control MethodsLazuardhy Vozicha FuturAinda não há avaliações

- AM2020-AFP1010 Installation Programming OperatingDocumento268 páginasAM2020-AFP1010 Installation Programming OperatingBaron RicthenAinda não há avaliações

- Project TerminationDocumento13 páginasProject TerminationsakshiAinda não há avaliações

- Export Promotion Zone/Special Economic Zone (Epz/Sez) & Export Oriented Units (EOU)Documento17 páginasExport Promotion Zone/Special Economic Zone (Epz/Sez) & Export Oriented Units (EOU)sakshiAinda não há avaliações

- Provisions Relating To Default in Furnishing Returns Under GSTDocumento2 páginasProvisions Relating To Default in Furnishing Returns Under GSTsakshiAinda não há avaliações

- Consumer Protection Act: Tushar Swami (609) Reshma Patil (610) Sarvesh Raj Singh (611) Sunket Anand PantDocumento41 páginasConsumer Protection Act: Tushar Swami (609) Reshma Patil (610) Sarvesh Raj Singh (611) Sunket Anand PantsakshiAinda não há avaliações

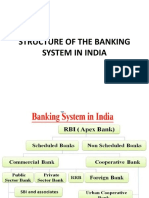

- Banking System in IndiaDocumento18 páginasBanking System in IndiasakshiAinda não há avaliações

- Unit - 1 - Acma CMC 653Documento128 páginasUnit - 1 - Acma CMC 653sakshiAinda não há avaliações

- Unit - 3 - Acma CMC 653Documento192 páginasUnit - 3 - Acma CMC 653sakshiAinda não há avaliações

- Meaning & Characteristics of A CompanyDocumento19 páginasMeaning & Characteristics of A Companysakshi100% (2)

- Derivatives & Risk ManagementDocumento62 páginasDerivatives & Risk ManagementsakshiAinda não há avaliações

- Option Valuation ModelsDocumento37 páginasOption Valuation ModelssakshiAinda não há avaliações

- Articles of AssociationDocumento21 páginasArticles of AssociationsakshiAinda não há avaliações

- 3a. Financial - Sector - ReformsDocumento23 páginas3a. Financial - Sector - ReformssakshiAinda não há avaliações

- Leasing1 AspectsDocumento19 páginasLeasing1 AspectssakshiAinda não há avaliações

- Financial InstitutionsDocumento15 páginasFinancial InstitutionssakshiAinda não há avaliações

- 329 Cryogenic Valves September 2016Documento8 páginas329 Cryogenic Valves September 2016TututSlengeanTapiSopanAinda não há avaliações

- FFL/ A: Tutorial On Reed-Solomon Error Correction CodingDocumento144 páginasFFL/ A: Tutorial On Reed-Solomon Error Correction Codingbatman chamkadarAinda não há avaliações

- Police Log September 24, 2016Documento14 páginasPolice Log September 24, 2016MansfieldMAPoliceAinda não há avaliações

- Bhakra Nangal Project1Documento3 páginasBhakra Nangal Project1Sonam Pahuja100% (1)

- Proposal Mini Project SBL LatestDocumento19 páginasProposal Mini Project SBL Latestapi-310034018Ainda não há avaliações

- Basic Definition of Manufacturing SystemDocumento18 páginasBasic Definition of Manufacturing SystemRavenjoy ArcegaAinda não há avaliações

- MOOT 1 (Principal Sir)Documento3 páginasMOOT 1 (Principal Sir)vaibhav jainAinda não há avaliações

- Accessing Biodiversity and Sharing The BenefitsDocumento332 páginasAccessing Biodiversity and Sharing The BenefitsNelson MartínezAinda não há avaliações

- RK3066 Mid PDFDocumento17 páginasRK3066 Mid PDFSharon MurphyAinda não há avaliações

- Jibachha's Textbook of Animal Health Volume-IIDocumento16 páginasJibachha's Textbook of Animal Health Volume-IIjibachha sahAinda não há avaliações

- 2.fundamentals of MappingDocumento5 páginas2.fundamentals of MappingB S Praveen BspAinda não há avaliações

- Dpco 151223080520 PDFDocumento23 páginasDpco 151223080520 PDFSiva PrasadAinda não há avaliações

- MAF 451 Suggested Solutions - A) I) Process 1Documento9 páginasMAF 451 Suggested Solutions - A) I) Process 1anis izzatiAinda não há avaliações

- Factors Influencing The Selection Of: MaterialsDocumento22 páginasFactors Influencing The Selection Of: MaterialsMaulik KotadiyaAinda não há avaliações

- Ventilation WorksheetDocumento1 páginaVentilation WorksheetIskandar 'muda' AdeAinda não há avaliações

- Shock Cat 2009Documento191 páginasShock Cat 2009gersonplovasAinda não há avaliações

- The Art of Starting OverDocumento2 páginasThe Art of Starting Overlarry brezoAinda não há avaliações

- Chain Rule 3LNDocumento2 páginasChain Rule 3LNsaad khAinda não há avaliações

- Irshad KamilDocumento11 páginasIrshad Kamilprakshid3022100% (1)

- Opening StrategyDocumento6 páginasOpening StrategyashrafsekalyAinda não há avaliações

- InflibnetDocumento3 páginasInflibnetSuhotra GuptaAinda não há avaliações

- Ecological Pyramids WorksheetDocumento3 páginasEcological Pyramids Worksheetapi-26236818833% (3)

- World War 1 NotesDocumento2 páginasWorld War 1 NotesSoarSZNAinda não há avaliações

- Awareness On Stock MarketDocumento11 páginasAwareness On Stock MarketBharath ReddyAinda não há avaliações