Você também pode gostar

- Chapter 19, Modern Advanced Accounting-Review Q & ExrDocumento17 páginasChapter 19, Modern Advanced Accounting-Review Q & Exrrlg4814100% (2)

- Nielsen Esports Playbook For Brands 2019Documento28 páginasNielsen Esports Playbook For Brands 2019Jean-Louis ManzonAinda não há avaliações

- M4 Budgeting For Profit and ControlDocumento8 páginasM4 Budgeting For Profit and Controlwingsenigma 00Ainda não há avaliações

- Far Qualifying ExaminationDocumento30 páginasFar Qualifying ExaminationAlvin BaternaAinda não há avaliações

- Grill Restaurant Business Plan TemplateDocumento11 páginasGrill Restaurant Business Plan TemplateSemira SimonAinda não há avaliações

- Ap 06 REO Receivables - PDF 074431Documento19 páginasAp 06 REO Receivables - PDF 074431ChristianAinda não há avaliações

- 20 Chapter - 20 - Effective - Interest - Method PDFDocumento25 páginas20 Chapter - 20 - Effective - Interest - Method PDFSheila Grace BajaAinda não há avaliações

- Chapter 10 Investments in Debt SecuritiesDocumento24 páginasChapter 10 Investments in Debt SecuritiesChristian Jade Lumasag NavaAinda não há avaliações

- How To Format Your Business ProposalDocumento2 páginasHow To Format Your Business Proposalwilly sergeAinda não há avaliações

- CH 5 LS Practice HW QUIZDocumento25 páginasCH 5 LS Practice HW QUIZDenise Jane RoqueAinda não há avaliações

- Principles of Marketing: Quarter 1 - Module 6: Marketing ResearchDocumento17 páginasPrinciples of Marketing: Quarter 1 - Module 6: Marketing ResearchAmber Dela Cruz100% (1)

- Unit II CFS Intercompany TransactionsDocumento17 páginasUnit II CFS Intercompany TransactionsDaisy TañoteAinda não há avaliações

- On April 1 2015 Benton Corporation Purchased 80 of TheDocumento1 páginaOn April 1 2015 Benton Corporation Purchased 80 of TheMuhammad Shahid0% (1)

- Floating PonttonDocumento9 páginasFloating PonttonToniAinda não há avaliações

- Consolidations - Subsequent To The Date of Acquisition: Multiple Choice QuestionsDocumento290 páginasConsolidations - Subsequent To The Date of Acquisition: Multiple Choice QuestionsKim FloresAinda não há avaliações

- Topic 9 - Inventories - Rev (Students)Documento42 páginasTopic 9 - Inventories - Rev (Students)RomziAinda não há avaliações

- HARRISON 1993 - The Soviet Economy and Relations With The United States and Britain, 1941-45Documento49 páginasHARRISON 1993 - The Soviet Economy and Relations With The United States and Britain, 1941-45Floripondio19Ainda não há avaliações

- ch4 PDFDocumento94 páginasch4 PDFMekanchha Dhakal100% (1)

- Dayag - Chapter 5 PDFDocumento25 páginasDayag - Chapter 5 PDFKen ZafraAinda não há avaliações

- Accounting Information System: The Expenditure CycleDocumento11 páginasAccounting Information System: The Expenditure CycleRatu ShaviraAinda não há avaliações

- Acc14 Exercise Capital-BudgetingDocumento3 páginasAcc14 Exercise Capital-BudgetingyeezzzzAinda não há avaliações

- Chapter 11 Capital Budgeting: Answers To QuestionsDocumento35 páginasChapter 11 Capital Budgeting: Answers To Questionsafsdasdf3qf4341f4asDAinda não há avaliações

- Advance Acct CH 3NDocumento18 páginasAdvance Acct CH 3NtemedebereAinda não há avaliações

- Wacc Practice 1Documento3 páginasWacc Practice 1Ash LayAinda não há avaliações

- TM 7 AklDocumento6 páginasTM 7 AklSyam NrAinda não há avaliações

- CH 1 & 14Documento13 páginasCH 1 & 14Rabie HarounAinda não há avaliações

- CA5 Accounting For Factory OverheadDocumento15 páginasCA5 Accounting For Factory OverheadhellokittysaranghaeAinda não há avaliações

- Auditing Chapter 1Documento7 páginasAuditing Chapter 1Sigei LeonardAinda não há avaliações

- Investments: Learning ObjectivesDocumento52 páginasInvestments: Learning ObjectivesElaine LingxAinda não há avaliações

- Advanced Financial Accounting and Reporting ExamDocumento10 páginasAdvanced Financial Accounting and Reporting ExamMuhammad HassaanAinda não há avaliações

- Chapter 09 Indirect and Mutual HoldingsDocumento22 páginasChapter 09 Indirect and Mutual HoldingsKukuh HariyadiAinda não há avaliações

- Mas 09 - Working CapitalDocumento7 páginasMas 09 - Working CapitalCarl Angelo LopezAinda não há avaliações

- Chap 17 Intercompany Sales of InventoryDocumento71 páginasChap 17 Intercompany Sales of InventoryPhrexilyn PajarilloAinda não há avaliações

- 02 CVP Analysis PDFDocumento5 páginas02 CVP Analysis PDFJunZon VelascoAinda não há avaliações

- This Study Resource WasDocumento7 páginasThis Study Resource WasAryan LeeAinda não há avaliações

- 02 Exercises - Accounting For NPOs v2Documento3 páginas02 Exercises - Accounting For NPOs v2Peter Andre GuintoAinda não há avaliações

- Financial Statement AnalysisDocumento5 páginasFinancial Statement AnalysisErwin Dave M. DahaoAinda não há avaliações

- Hca14 PPT CH07Documento39 páginasHca14 PPT CH07Kamlesh ShuklaAinda não há avaliações

- Ch15 Raiborn SMDocumento26 páginasCh15 Raiborn SMMendelle Murry100% (1)

- Ifrs 9 Debt Investment IllustrationDocumento9 páginasIfrs 9 Debt Investment IllustrationVatchdemonAinda não há avaliações

- Basic Accounting Equation Exercises 2Documento2 páginasBasic Accounting Equation Exercises 2Ace Joseph TabaderoAinda não há avaliações

- Financial AnalysisDocumento18 páginasFinancial AnalysisHannah JoyAinda não há avaliações

- Chapter 5: The Expenditure Cycle Part 1: Purchases and Cash Disbursements ProceduresDocumento7 páginasChapter 5: The Expenditure Cycle Part 1: Purchases and Cash Disbursements ProceduresAstxilAinda não há avaliações

- CH 14Documento4 páginasCH 14Hoàng HuyAinda não há avaliações

- BUSCOMDocumento5 páginasBUSCOMGeoreyGAinda não há avaliações

- Business Combination Drill PDFDocumento2 páginasBusiness Combination Drill PDFMelvin MendozaAinda não há avaliações

- ROMERO BSMA1E Standard Costing ExerciseDocumento4 páginasROMERO BSMA1E Standard Costing ExerciseAliah Romero100% (1)

- IFRS 11 SummaryDocumento4 páginasIFRS 11 SummaryJoshua Capa Fronda100% (1)

- Backflush Costing System and Activity Based Costing System With SolutionDocumento15 páginasBackflush Costing System and Activity Based Costing System With SolutionJhazreene ArnozaAinda não há avaliações

- Case 2Documento4 páginasCase 2Chris WongAinda não há avaliações

- Accou NT No. Account Name Trial Balance Adjustment Income Statement Debit Credit Debit Credit DebitDocumento44 páginasAccou NT No. Account Name Trial Balance Adjustment Income Statement Debit Credit Debit Credit DebitJam SurdivillaAinda não há avaliações

- 01 Equity MethodDocumento41 páginas01 Equity MethodAngel Obligacion100% (1)

- Refer To The Accounting Change by Wertz Construction Company in PDFDocumento1 páginaRefer To The Accounting Change by Wertz Construction Company in PDFAnbu jaromiaAinda não há avaliações

- Financial Asset at Fair Value: Intermediate Accounting 1 Ray Patrick S. Guangco, CPADocumento17 páginasFinancial Asset at Fair Value: Intermediate Accounting 1 Ray Patrick S. Guangco, CPAClaire Magbunag AntidoAinda não há avaliações

- Foreign Currency Transactions2019Documento6 páginasForeign Currency Transactions2019Jeann MuycoAinda não há avaliações

- Capital BudgetingDocumento4 páginasCapital Budgetingrachmmm0% (3)

- Chapter 15Documento34 páginasChapter 15IstikharohAinda não há avaliações

- Week 8Documento3 páginasWeek 8Anonymous J0pEMcy5vY100% (1)

- This Study Resource Was: Multiple ChoiceDocumento6 páginasThis Study Resource Was: Multiple ChoiceNicah AcojonAinda não há avaliações

- Scanner CAP II Financial ManagementDocumento195 páginasScanner CAP II Financial ManagementEdtech NepalAinda não há avaliações

- Strat Cost Drop or ContinueDocumento1 páginaStrat Cost Drop or ContinueStephannieArreolaAinda não há avaliações

- Quiz 5 Problems Second Semester AY2223 With AnswersDocumento4 páginasQuiz 5 Problems Second Semester AY2223 With AnswersManzano, Carl Clinton Neil D.Ainda não há avaliações

- Capital BudgetingDocumento44 páginasCapital Budgetingrisbd appliancesAinda não há avaliações

- CompExam D AcceptedDocumento10 páginasCompExam D Acceptedrahul shahAinda não há avaliações

- Chap7.PAYOUT POLICYDocumento85 páginasChap7.PAYOUT POLICYHoang NguyenAinda não há avaliações

- Chap 6 BBDocumento66 páginasChap 6 BBTaVuKieuNhiAinda não há avaliações

- Chapter 14 BBDocumento69 páginasChapter 14 BBTaVuKieuNhiAinda não há avaliações

- Chap 11 (PT 1) BBDocumento43 páginasChap 11 (PT 1) BBTaVuKieuNhiAinda não há avaliações

- Chapter 27 BBDocumento23 páginasChapter 27 BBTaVuKieuNhiAinda não há avaliações

- Market Efficiency BBDocumento11 páginasMarket Efficiency BBTaVuKieuNhiAinda não há avaliações

- Estimating The Cost of CapitalDocumento50 páginasEstimating The Cost of CapitalTaVuKieuNhiAinda não há avaliações

- Chapter 24 BBDocumento25 páginasChapter 24 BBTaVuKieuNhiAinda não há avaliações

- Chap 11 BB (PT 2 New)Documento59 páginasChap 11 BB (PT 2 New)TaVuKieuNhiAinda não há avaliações

- Chapter 23BBDocumento27 páginasChapter 23BBTaVuKieuNhi100% (1)

- Chap 9 BBDocumento69 páginasChap 9 BBTaVuKieuNhiAinda não há avaliações

- Capital Markets and The Pricing of Risk: Chapter 10 (Part I)Documento43 páginasCapital Markets and The Pricing of Risk: Chapter 10 (Part I)TaVuKieuNhiAinda não há avaliações

- Capital Markets and The Pricing of Risk: Chapter 10 (Part 2)Documento66 páginasCapital Markets and The Pricing of Risk: Chapter 10 (Part 2)TaVuKieuNhiAinda não há avaliações

- Financial Management: Chapter 1 The CorporationDocumento38 páginasFinancial Management: Chapter 1 The CorporationTaVuKieuNhiAinda não há avaliações

- Tutorial 1Documento2 páginasTutorial 1TaVuKieuNhi100% (1)

- Formula SheetDocumento3 páginasFormula SheetTaVuKieuNhiAinda não há avaliações

- Leaders Eat LastDocumento6 páginasLeaders Eat LastTaVuKieuNhi25% (4)

- Introduction To APA Style 6th Ed 2010Documento32 páginasIntroduction To APA Style 6th Ed 2010Wided SassiAinda não há avaliações

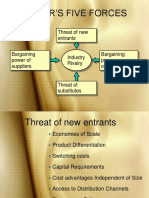

- Porter's Five ForcesDocumento9 páginasPorter's Five ForcesTaVuKieuNhiAinda não há avaliações

- Introduction To APA Style 6th Ed 2010Documento32 páginasIntroduction To APA Style 6th Ed 2010Wided SassiAinda não há avaliações

- Malaysian Judicial Structure: Superior CourtsDocumento21 páginasMalaysian Judicial Structure: Superior CourtsIz'aan AzalanAinda não há avaliações

- Chapter 9: Stocks ValuationDocumento35 páginasChapter 9: Stocks ValuationTaVuKieuNhiAinda não há avaliações

- All-India rWnMYexDocumento89 páginasAll-India rWnMYexketan kanameAinda não há avaliações

- SAi Sankata Nivarana StotraDocumento3 páginasSAi Sankata Nivarana Stotrageetai897Ainda não há avaliações

- The Relationship Between Law and MoralityDocumento12 páginasThe Relationship Between Law and MoralityAnthony JosephAinda não há avaliações

- Lipid Metabolism Quize PDFDocumento5 páginasLipid Metabolism Quize PDFMadani TawfeeqAinda não há avaliações

- Developmental PsychologyDocumento2 páginasDevelopmental PsychologyPatricia Xandra AurelioAinda não há avaliações

- Klarna: Klarna A Company Valued To Be 5.5 Billion and 8 Most Valued Fintech Company in The WorldDocumento1 páginaKlarna: Klarna A Company Valued To Be 5.5 Billion and 8 Most Valued Fintech Company in The WorldChetan NarasannavarAinda não há avaliações

- Draft DAO SAPA Provisional AgreementDocumento6 páginasDraft DAO SAPA Provisional AgreementStaff of Gov Victor J YuAinda não há avaliações

- FAR REview. DinkieDocumento10 páginasFAR REview. DinkieJollibee JollibeeeAinda não há avaliações

- Chapter 12 Financial Management and Financial Objectives: Answer 1Documento9 páginasChapter 12 Financial Management and Financial Objectives: Answer 1PmAinda não há avaliações

- The Role of Religion in The Causation of Global Conflict & Peace and Other Related Issues Regarding Conflict ResolutionDocumento11 páginasThe Role of Religion in The Causation of Global Conflict & Peace and Other Related Issues Regarding Conflict ResolutionlorenAinda não há avaliações

- Chronology of Events:: Account: North Davao Mining Corp (NDMC)Documento2 páginasChronology of Events:: Account: North Davao Mining Corp (NDMC)John Robert BautistaAinda não há avaliações

- Math Country Ranking Alevel 2023Documento225 páginasMath Country Ranking Alevel 2023Lutaaya Paul BamutaliraAinda não há avaliações

- Ogl 350 Paper 2Documento5 páginasOgl 350 Paper 2api-672448292Ainda não há avaliações

- Anthem Harrison Bargeron EssayDocumento3 páginasAnthem Harrison Bargeron Essayapi-242741408Ainda não há avaliações

- Chapter 3 - StudentDocumento38 páginasChapter 3 - StudentANIS NATASHA BT ABDULAinda não há avaliações

- Assignment 1: Microeconomics - Group 10Documento13 páginasAssignment 1: Microeconomics - Group 10Hải LêAinda não há avaliações

- John Wick 4 HD Free r6hjDocumento16 páginasJohn Wick 4 HD Free r6hjafdal mahendraAinda não há avaliações

- Research Article: Old Sagay, Sagay City, Negros Old Sagay, Sagay City, Negros Occidental, PhilippinesDocumento31 páginasResearch Article: Old Sagay, Sagay City, Negros Old Sagay, Sagay City, Negros Occidental, PhilippinesLuhenAinda não há avaliações

- Tiananmen1989(六四事件)Documento55 páginasTiananmen1989(六四事件)qianzhonghua100% (3)

- Fort St. John 108 Street & Alaska Highway IntersectionDocumento86 páginasFort St. John 108 Street & Alaska Highway IntersectionAlaskaHighwayNewsAinda não há avaliações

- Math 3140-004: Vector Calculus and PdesDocumento6 páginasMath 3140-004: Vector Calculus and PdesNathan MonsonAinda não há avaliações

- In Practice Blood Transfusion in Dogs and Cats1Documento7 páginasIn Practice Blood Transfusion in Dogs and Cats1何元Ainda não há avaliações

- Gender CriticismDocumento17 páginasGender CriticismJerickRepilRabeAinda não há avaliações

- 3RD Last RPHDocumento5 páginas3RD Last RPHAdil Mohamad KadriAinda não há avaliações