Você também pode gostar

- FM Assignment 7 - Group 4Documento7 páginasFM Assignment 7 - Group 4Puspita RamadhaniaAinda não há avaliações

- Receivables ProblemsDocumento13 páginasReceivables ProblemsIris Mnemosyne0% (1)

- Capital StructureDocumento21 páginasCapital StructureRameen Jawad MalikAinda não há avaliações

- CH 15Documento28 páginasCH 15RSAinda não há avaliações

- C09 +chap+16 +Capital+Structure+-+Basic+ConceptsDocumento24 páginasC09 +chap+16 +Capital+Structure+-+Basic+Conceptsstanley tsangAinda não há avaliações

- Manajemen Keuangan - 20 Nov 2021 - BDocumento24 páginasManajemen Keuangan - 20 Nov 2021 - Bmuhammad nurAinda não há avaliações

- CF - Chapter 16 - Capital StructureDocumento25 páginasCF - Chapter 16 - Capital StructureS A M AAinda não há avaliações

- Capital Structure: Rakesh ArrawatiaDocumento38 páginasCapital Structure: Rakesh ArrawatiashravaniAinda não há avaliações

- Capital Structure - Basic ConceptsDocumento10 páginasCapital Structure - Basic ConceptsDUY LE NHAT TRUONGAinda não há avaliações

- 041924353041-Review Chapter 16Documento3 páginas041924353041-Review Chapter 16Aimé RandrianantenainaAinda não há avaliações

- Capital Structure: Basic ConceptsDocumento34 páginasCapital Structure: Basic ConceptsNitish BudhirajaAinda não há avaliações

- Capital Structure Extra NotesDocumento29 páginasCapital Structure Extra NotesleighannAinda não há avaliações

- CF - Chapter 16Documento25 páginasCF - Chapter 16Quân LêAinda não há avaliações

- LN Capstru1Documento63 páginasLN Capstru1pgdm23samamalAinda não há avaliações

- Chap 016Documento25 páginasChap 016Utkarsh GoelAinda não há avaliações

- Capital Structure Basic ConceptsDocumento25 páginasCapital Structure Basic ConceptsisratzamananuAinda não há avaliações

- Capital Structure: Basic ConceptsDocumento25 páginasCapital Structure: Basic ConceptsThuyDuongAinda não há avaliações

- Capital Structure: Basic Concepts: Mcgraw-Hill/IrwinDocumento25 páginasCapital Structure: Basic Concepts: Mcgraw-Hill/IrwinBennyKurniawanAinda não há avaliações

- Fundamentals of Capital StructureDocumento42 páginasFundamentals of Capital StructureSona Singh pgpmx 2017 batch-2Ainda não há avaliações

- Ebit Eps AnalysisDocumento15 páginasEbit Eps AnalysisGunjan GargAinda não há avaliações

- Capital Structure - Sep 2021Documento52 páginasCapital Structure - Sep 2021BHAVYA KANDPAL 13BCE0206Ainda não há avaliações

- Capital Structure: Basic ConceptsDocumento27 páginasCapital Structure: Basic ConceptsRemonAinda não há avaliações

- Chap 15Documento66 páginasChap 15jamn1979Ainda não há avaliações

- Capital Structure DecisionDocumento26 páginasCapital Structure DecisionNet BeeAinda não há avaliações

- FFM 1013Documento55 páginasFFM 1013Suzana MerchantAinda não há avaliações

- Optimal Capital Structure Is The Mix of Debt and Equity ThatDocumento29 páginasOptimal Capital Structure Is The Mix of Debt and Equity ThatdevashneeAinda não há avaliações

- Capital Structure IDocumento23 páginasCapital Structure IhatemAinda não há avaliações

- Chapter 16 Tcdn GốcDocumento37 páginasChapter 16 Tcdn GốcN KhAinda não há avaliações

- Capital Structure: Basic ConceptsDocumento27 páginasCapital Structure: Basic ConceptsArjun SharmaAinda não há avaliações

- Questions F9 Ipass PDFDocumento60 páginasQuestions F9 Ipass PDFAmir ArifAinda não há avaliações

- M M HypothesisDocumento37 páginasM M HypothesisJim MathilakathuAinda não há avaliações

- Capital Structure and LeverageDocumento51 páginasCapital Structure and LeverageGian Alexis FernandezAinda não há avaliações

- Capital StructureDocumento73 páginasCapital Structuresourav kumar dasAinda não há avaliações

- Free Cash Flow From EBITDA Excel TemplateDocumento5 páginasFree Cash Flow From EBITDA Excel TemplatePhuongwater Le Thanh PhuongAinda não há avaliações

- ExportDocumento21 páginasExportBükre PAinda não há avaliações

- FM Assignment1Documento6 páginasFM Assignment1Rishi Kumar SainiAinda não há avaliações

- 2nd Assignment of Financial ManagementDocumento6 páginas2nd Assignment of Financial Managementpratiksha24Ainda não há avaliações

- AC6101 Lecture 3 - Capital Structure (M&M) - Xid-2956908 - 1Documento28 páginasAC6101 Lecture 3 - Capital Structure (M&M) - Xid-2956908 - 1Kelsey GaoAinda não há avaliações

- CTM Tutorial 3Documento4 páginasCTM Tutorial 3crsAinda não há avaliações

- Leverages: Raksha Khetan-23 Saumitra Kumar-26 Saqib Azam Qadri-42Documento21 páginasLeverages: Raksha Khetan-23 Saumitra Kumar-26 Saqib Azam Qadri-42sampdalvi07Ainda não há avaliações

- Fitriyanto - Financial Management Asignment - CH 14 15Documento6 páginasFitriyanto - Financial Management Asignment - CH 14 15iyanAinda não há avaliações

- LeveragesDocumento50 páginasLeveragesPrem KishanAinda não há avaliações

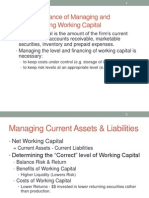

- The Importance of Managing and Accumulating Working CapitalDocumento18 páginasThe Importance of Managing and Accumulating Working CapitalSreekanth DhananjayanAinda não há avaliações

- Topic 8Documento7 páginasTopic 8黄芷琦Ainda não há avaliações

- Concepts Review and Critical Thinking Questions 4Documento6 páginasConcepts Review and Critical Thinking Questions 4fnrbhcAinda não há avaliações

- Capital StructureDocumento27 páginasCapital Structuresiddharth agrawalAinda não há avaliações

- 317 Midterm 1 Practice Exam SolutionsDocumento9 páginas317 Midterm 1 Practice Exam Solutionskinyuadavid000Ainda não há avaliações

- New LeveragesDocumento16 páginasNew Leveragesmackm87Ainda não há avaliações

- Ch13 Capital Structure and LeverageDocumento49 páginasCh13 Capital Structure and LeverageSukmawatiiAinda não há avaliações

- LÀM LẠI ĐỀ MIDTERMDocumento15 páginasLÀM LẠI ĐỀ MIDTERMGiang HoàngAinda não há avaliações

- Chapter 3 BA 390Documento25 páginasChapter 3 BA 390SweezAinda não há avaliações

- 3rd Presentation 2020Documento51 páginas3rd Presentation 2020Camila Arango PérezAinda não há avaliações

- S7 Capital Structure Online VersionDocumento34 páginasS7 Capital Structure Online Versionconstruction omanAinda não há avaliações

- 02 CapStr Basic NiuDocumento28 páginas02 CapStr Basic NiuLombeAinda não há avaliações

- RADHA Financial ASSIGNMENTDocumento4 páginasRADHA Financial ASSIGNMENTradha sharmaAinda não há avaliações

- MBS Corporate Finance 2023 Slide Set 4Documento112 páginasMBS Corporate Finance 2023 Slide Set 4PGAinda não há avaliações

- Leverage: Prepared By:-Priyanka GohilDocumento23 páginasLeverage: Prepared By:-Priyanka GohilSunil PillaiAinda não há avaliações

- Report p2Documento58 páginasReport p2Roland Jay DelfinAinda não há avaliações

- Session 13Documento38 páginasSession 13Priyanshi PaliwalAinda não há avaliações

- AFM IBSB Leverages WordDocumento16 páginasAFM IBSB Leverages WordSangeetha K SAinda não há avaliações

- Wiley CMAexcel Learning System Exam Review 2017: Part 2, Financial Decision Making (1-year access)No EverandWiley CMAexcel Learning System Exam Review 2017: Part 2, Financial Decision Making (1-year access)Ainda não há avaliações

- Hampton Suggested AnswersDocumento5 páginasHampton Suggested Answersamsa100% (1)

- Citicorp 1985Documento13 páginasCiticorp 1985amsaAinda não há avaliações

- The Power of TalkDocumento24 páginasThe Power of TalkamsaAinda não há avaliações

- The Power of TalkDocumento24 páginasThe Power of TalkamsaAinda não há avaliações

- Xls066 Xls EngDocumento11 páginasXls066 Xls EngamsaAinda não há avaliações

- G.R. No. 47593 September 13, 1941 - The Insular Life Assurance Co. v. Serafin D. Feliciano, Et Al. - 073 Phil 201Documento14 páginasG.R. No. 47593 September 13, 1941 - The Insular Life Assurance Co. v. Serafin D. Feliciano, Et Al. - 073 Phil 201Vanny Joyce BaluyutAinda não há avaliações

- HIH Insurance GroupDocumento41 páginasHIH Insurance Groupgigito100% (1)

- Investments, 8 Edition: Risk Aversion and Capital Allocation To Risky AssetsDocumento34 páginasInvestments, 8 Edition: Risk Aversion and Capital Allocation To Risky AssetsAkshat JainAinda não há avaliações

- McDonalds Marketing AuditingDocumento3 páginasMcDonalds Marketing AuditingRawan AdelAinda não há avaliações

- Quiz 1 With Sol KeyDocumento5 páginasQuiz 1 With Sol KeySachin Gupta100% (1)

- Starting A New Venture: Module For Principles of Entrepreneurship (ENT 530)Documento31 páginasStarting A New Venture: Module For Principles of Entrepreneurship (ENT 530)Mohd Azrul Hisham AmranAinda não há avaliações

- Misa Service Manual 8th Edition en v18Documento155 páginasMisa Service Manual 8th Edition en v18HussonAinda não há avaliações

- R Money Sip Presentation by Ravish Roshandelhi 1223401016149009 9Documento19 páginasR Money Sip Presentation by Ravish Roshandelhi 1223401016149009 9Yukti KhoslaAinda não há avaliações

- Family Budget (Monthly) 1Documento5 páginasFamily Budget (Monthly) 1Jesiél Da RochaAinda não há avaliações

- Adani PowerDocumento10 páginasAdani PowerMontu AdaniAinda não há avaliações

- Project Charter - Waftly Towers Hotel RehabilitationDocumento5 páginasProject Charter - Waftly Towers Hotel RehabilitationabdullahAinda não há avaliações

- GFMS Gold Survey 2015Documento116 páginasGFMS Gold Survey 2015Vaggelis PanagiotopoulosAinda não há avaliações

- General Mathematics 1Documento23 páginasGeneral Mathematics 1Pat G.Ainda não há avaliações

- Accounting Assignment: Company Name:-Bajaj AutoDocumento5 páginasAccounting Assignment: Company Name:-Bajaj Autonand bhushanAinda não há avaliações

- Chapter 1 - Buyback Additional QuestionsDocumento9 páginasChapter 1 - Buyback Additional QuestionsMohammad ArifAinda não há avaliações

- BCC BR 112 14Documento4 páginasBCC BR 112 14Nitesh varmaAinda não há avaliações

- Civil Services Mentor May 2012 PDFDocumento121 páginasCivil Services Mentor May 2012 PDFBhavtosh ChaturvediAinda não há avaliações

- Banking Midterms ReviewerDocumento6 páginasBanking Midterms ReviewerFlorence RoseteAinda não há avaliações

- Mba 4 YerDocumento3 páginasMba 4 YerRashidAinda não há avaliações

- Billercode FavouritesDocumento7 páginasBillercode FavouritesJaya SugantiniAinda não há avaliações

- Company's Profile Presentation (Mauritius Commercial Bank)Documento23 páginasCompany's Profile Presentation (Mauritius Commercial Bank)ashairways100% (2)

- Ishares Core Growth Etf Portfolio: Key FactsDocumento2 páginasIshares Core Growth Etf Portfolio: Key FactsTushar PatelAinda não há avaliações

- 02.damodaran - Corporate FinanceDocumento239 páginas02.damodaran - Corporate Financessj9Ainda não há avaliações

- Chapter 23 Associates and Joint Ventures (Samplepractice-Exam-18-September-2018-Questions-And-Answers)Documento18 páginasChapter 23 Associates and Joint Ventures (Samplepractice-Exam-18-September-2018-Questions-And-Answers)XAinda não há avaliações

- Lec 4 Optimal Portfolio Selection A Few Analytical Results 20170923102633 PDFDocumento12 páginasLec 4 Optimal Portfolio Selection A Few Analytical Results 20170923102633 PDFMassimiliano RizzoAinda não há avaliações

- Manufacture of NaphthalenMANUFACTURE OF NAPHTHALENEDocumento14 páginasManufacture of NaphthalenMANUFACTURE OF NAPHTHALENEManoj Ranjan100% (1)

- Merger of HDFC Bank and Centurion Bank of PunjabDocumento9 páginasMerger of HDFC Bank and Centurion Bank of PunjabJacob BrewerAinda não há avaliações

- Market RatioDocumento11 páginasMarket RatioThảo LêAinda não há avaliações