Você também pode gostar

- Review Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020Documento34 páginasReview Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020AB Cloyd100% (1)

- Cash Flow StatementDocumento19 páginasCash Flow Statementasherjoe67% (3)

- Cash Flow AnalysisDocumento38 páginasCash Flow AnalysisDragan100% (4)

- Cash Flow Analysis and StatementDocumento127 páginasCash Flow Analysis and Statementsnhk679546100% (6)

- Cash Flow Analysis and Statement of Cash FlowsDocumento29 páginasCash Flow Analysis and Statement of Cash FlowsUmer Zaheer100% (1)

- Working Capital ManagementDocumento34 páginasWorking Capital ManagementShikha Agarwal100% (1)

- Analysis of Financial Statements Of: Presented by AyeshaDocumento30 páginasAnalysis of Financial Statements Of: Presented by AyeshaaaaaAinda não há avaliações

- Cash Flow AnalysisDocumento28 páginasCash Flow AnalysisHONG RY100% (1)

- Lecture7 WorkingCapitalManagementDocumento91 páginasLecture7 WorkingCapitalManagementduncan100% (4)

- SEM II Cost-Accounting Unit 1Documento23 páginasSEM II Cost-Accounting Unit 1mahendrabpatelAinda não há avaliações

- Cost and Management AccountingDocumento82 páginasCost and Management Accountinghimanshugupta6100% (1)

- Financial AnalysisDocumento3 páginasFinancial Analysissai271992100% (1)

- 1.financial Management IntroductionDocumento78 páginas1.financial Management Introductionvijay kumar50% (2)

- Financial Modeling & ValuationDocumento71 páginasFinancial Modeling & ValuationKoray Çelik67% (3)

- Cash Flow StatementDocumento40 páginasCash Flow Statementtairakazida100% (3)

- Capital BudgetingDocumento12 páginasCapital BudgetingAbs Pangader100% (11)

- Financial ManagementDocumento85 páginasFinancial ManagementRajesh MgAinda não há avaliações

- Financial PlanningDocumento22 páginasFinancial Planningangshu002085% (13)

- Balance Sheet Income StatementDocumento50 páginasBalance Sheet Income Statementgurbaxeesh0% (1)

- Introduction To Financial ManagementDocumento34 páginasIntroduction To Financial ManagementKevin OnaroAinda não há avaliações

- Working Capital ManagementDocumento43 páginasWorking Capital ManagementDebasmita Saha77% (31)

- Calculate real cost of capitalDocumento8 páginasCalculate real cost of capitalJiya RajputAinda não há avaliações

- Chapter 1 - Introduction To Managerial AccountingDocumento22 páginasChapter 1 - Introduction To Managerial AccountingviraAinda não há avaliações

- Capital BudgetingDocumento30 páginasCapital BudgetingPrabath Suranaga MorawakageAinda não há avaliações

- Understanding The Income StatementDocumento4 páginasUnderstanding The Income Statementluvujaya100% (1)

- Financial Planning & ForecastingDocumento44 páginasFinancial Planning & Forecastingnageshalways503275% (4)

- Financial Ratio AnalysisDocumento11 páginasFinancial Ratio Analysispradeep100% (5)

- Financial Statement AnalysisDocumento53 páginasFinancial Statement Analysisremon4hrAinda não há avaliações

- Financial ManagementDocumento20 páginasFinancial ManagementGAURAV SHARMA100% (1)

- Cash Flow Statement AnalysisDocumento19 páginasCash Flow Statement AnalysisKNOWLEDGE CREATORS90% (10)

- Financial ManagementDocumento65 páginasFinancial Managementshekharnishu96% (27)

- Chapter 15 Company AnalysisDocumento51 páginasChapter 15 Company Analysissharktale282850% (2)

- Learn Financial Modelling & Get NSE CertifiedDocumento25 páginasLearn Financial Modelling & Get NSE CertifiedSukumarAinda não há avaliações

- Ratio Analysis GuideDocumento20 páginasRatio Analysis Guideanurag6866Ainda não há avaliações

- Cost Accounting Book of 3rd Sem Mba at Bec DomsDocumento148 páginasCost Accounting Book of 3rd Sem Mba at Bec DomsBabasab Patil (Karrisatte)100% (3)

- Cost of CapitalDocumento18 páginasCost of CapitalyukiAinda não há avaliações

- Cost and Management AccountingDocumento29 páginasCost and Management AccountingAks SinhaAinda não há avaliações

- Cash FlowDocumento28 páginasCash Flowleen mercado100% (1)

- Financial StatementDocumento10 páginasFinancial StatementJessica100% (1)

- Introduction To Financial Markets and Investment PDFDocumento64 páginasIntroduction To Financial Markets and Investment PDFDr. Chhiv Sok Thet100% (12)

- Financial AnalysisDocumento44 páginasFinancial AnalysisHeap Ke Xin100% (3)

- Statement of Cash FlowDocumento4 páginasStatement of Cash FlowElyse Burns-HillAinda não há avaliações

- Financial Reporting PDFDocumento67 páginasFinancial Reporting PDFlukamasia93% (15)

- FINANCIAL STATEMENT ANALYSIS TOOLSDocumento28 páginasFINANCIAL STATEMENT ANALYSIS TOOLSSachin Methree75% (4)

- Toyota & Honda Financial Ratios ComparisonDocumento11 páginasToyota & Honda Financial Ratios Comparisonuaintdown2100% (1)

- Cash Flow Statement AnalysisDocumento11 páginasCash Flow Statement Analysisrscjat100% (1)

- Corporate Financial StrategyDocumento14 páginasCorporate Financial StrategyHammad AhmadAinda não há avaliações

- Dividend PolicyDocumento10 páginasDividend Policyanuramaharjan78% (9)

- CHP 1 - Capital Investment Decisions Appraisal MethodsDocumento52 páginasCHP 1 - Capital Investment Decisions Appraisal MethodsConnieLowAinda não há avaliações

- Balance Sheet BasicsDocumento12 páginasBalance Sheet Basicsapi-3741610100% (2)

- Cash Flow Statements PDFDocumento101 páginasCash Flow Statements PDFSubbu ..100% (1)

- Financial Ratio AnalysisDocumento85 páginasFinancial Ratio AnalysisSarah PontinesAinda não há avaliações

- Statement of Cash FlowsDocumento16 páginasStatement of Cash FlowsBrian Reyes GangcaAinda não há avaliações

- Financial Statement Analysis: An OverviewDocumento57 páginasFinancial Statement Analysis: An OverviewYogesh PawarAinda não há avaliações

- Cash Flow Analysis, Gross Profit Analysis, Basic Earnings Per Share and Diluted Earnings Per ShareDocumento135 páginasCash Flow Analysis, Gross Profit Analysis, Basic Earnings Per Share and Diluted Earnings Per ShareMariel de Lara100% (2)

- Atp 106 LPM Accounting - Topic 5 - Statement of Cash FlowsDocumento17 páginasAtp 106 LPM Accounting - Topic 5 - Statement of Cash FlowsTwain JonesAinda não há avaliações

- Ias 3Documento21 páginasIas 3JyotiAinda não há avaliações

- Guide to Cash Flow Statements - Operating, Investing, Financing ActivitiesDocumento29 páginasGuide to Cash Flow Statements - Operating, Investing, Financing ActivitiesPalak GoelAinda não há avaliações

- Pas 7 - Statement of Cash FlowsDocumento8 páginasPas 7 - Statement of Cash FlowsJohn Rafael Reyes PeloAinda não há avaliações

- Sex and Love 2Documento11 páginasSex and Love 2kojo2kgAinda não há avaliações

- Information Technology Audit: General PrinciplesDocumento26 páginasInformation Technology Audit: General Principlesreema_rao_2Ainda não há avaliações

- Africa and Global Economic Trends Quarterly Review - First Quarter 2013Documento23 páginasAfrica and Global Economic Trends Quarterly Review - First Quarter 2013kojo2kgAinda não há avaliações

- 3rd Mobile Post Conference ReportDocumento14 páginas3rd Mobile Post Conference Reportkojo2kgAinda não há avaliações

- Measuring Impact of Dos Attacks: NtroductionDocumento4 páginasMeasuring Impact of Dos Attacks: Ntroductionkojo2kgAinda não há avaliações

- Emergency Management Plan (Summary) Concordia UniversityDocumento16 páginasEmergency Management Plan (Summary) Concordia Universitykojo2kgAinda não há avaliações

- ECSS v3 BrochureDocumento39 páginasECSS v3 Brochurekojo2kgAinda não há avaliações

- A Scaleable M-Commerce Solution WPDocumento36 páginasA Scaleable M-Commerce Solution WPkojo2kgAinda não há avaliações

- 1st Quarter NewsletterDocumento16 páginas1st Quarter NewsletterkayaozgurAinda não há avaliações

- Strategic Priorities For The Indian Telecom Industry in The Next DecadeDocumento1 páginaStrategic Priorities For The Indian Telecom Industry in The Next Decadekojo2kgAinda não há avaliações

- Joint Venture ProceduresDocumento12 páginasJoint Venture Procedureskojo2kgAinda não há avaliações

- Strategic Priorities For The Indian Telecom Industry in The Next DecadeDocumento1 páginaStrategic Priorities For The Indian Telecom Industry in The Next Decadekojo2kgAinda não há avaliações

- Research PaperDocumento205 páginasResearch Paperec01Ainda não há avaliações

- Ghana Energy and PovertyDocumento8 páginasGhana Energy and Povertykojo2kgAinda não há avaliações

- DistanceDistance Vector Versus Link Vector Versus LinkDocumento3 páginasDistanceDistance Vector Versus Link Vector Versus Linkkojo2kgAinda não há avaliações

- Petrolum revpaper-NP PDFDocumento26 páginasPetrolum revpaper-NP PDFfranck008Ainda não há avaliações

- ProjectDocumento1 páginaProjectkojo2kgAinda não há avaliações

- What To Ask .. Team Building: Some Questions For A Potential Service ProviderDocumento2 páginasWhat To Ask .. Team Building: Some Questions For A Potential Service ProviderHo Thuy DungAinda não há avaliações

- 19-Article Text-27-1-10-20210124Documento14 páginas19-Article Text-27-1-10-20210124CindaAinda não há avaliações

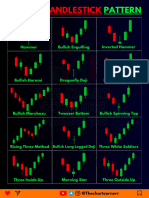

- Chart Pattern Cheat Sheet-1Documento18 páginasChart Pattern Cheat Sheet-1YASHANK VISHWAKARMAAinda não há avaliações

- Subsequent Acquisition PDFDocumento21 páginasSubsequent Acquisition PDFEvangeline WongAinda não há avaliações

- What is Market Profile in 40 CharactersDocumento3 páginasWhat is Market Profile in 40 Charactersnakulyadav7Ainda não há avaliações

- Audit procedures and evidenceDocumento7 páginasAudit procedures and evidenceJun Ladrillo100% (1)

- ECGCDocumento24 páginasECGCShilpa KhannaAinda não há avaliações

- Gbus 7603 - Valuation in Financial Markets Fall 2017, SY Quarter 1Documento19 páginasGbus 7603 - Valuation in Financial Markets Fall 2017, SY Quarter 1zZl3Ul2NNINGZzAinda não há avaliações

- Due Diligence InvestmentsDocumento6 páginasDue Diligence InvestmentselinzolaAinda não há avaliações

- Central Bank of The Philippines v. CA (G.r. No. 88353) DigestDocumento2 páginasCentral Bank of The Philippines v. CA (G.r. No. 88353) DigestApril100% (1)

- Lesson 11 Introduction To EasyLanguageDocumento18 páginasLesson 11 Introduction To EasyLanguageJose Alfredo CabreraAinda não há avaliações

- The Cost of Capital ExplainedDocumento56 páginasThe Cost of Capital ExplainedAndayani SalisAinda não há avaliações

- Chapter 02 AnsDocumento9 páginasChapter 02 AnsDave Manalo100% (1)

- CalPERS Annual Investment Report SummaryDocumento296 páginasCalPERS Annual Investment Report SummaryChris WatkinsAinda não há avaliações

- Goldman Sachs Presentationppt409Documento25 páginasGoldman Sachs Presentationppt409Swati AryaAinda não há avaliações

- Forgery Defenses; Bank LiabilitiesDocumento24 páginasForgery Defenses; Bank LiabilitiesbrendamanganaanAinda não há avaliações

- Topic 1 - Chapter 1 - 2018 SGDocumento6 páginasTopic 1 - Chapter 1 - 2018 SGMichael LightAinda não há avaliações

- (Principle of Commerce) T, C & B MCQS: Rade Ommerce UsinessDocumento18 páginas(Principle of Commerce) T, C & B MCQS: Rade Ommerce UsinessGhalib HussainAinda não há avaliações

- Financial Analysis of DG Khan Cement Company LtdDocumento19 páginasFinancial Analysis of DG Khan Cement Company LtdHissan AhmedAinda não há avaliações

- s4 Hana Finance OverviewDocumento21 páginass4 Hana Finance OverviewsundarsapAinda não há avaliações

- Accounting StandardDocumento14 páginasAccounting StandardridhiAinda não há avaliações

- City of London LSE David KynastonDocumento2 páginasCity of London LSE David Kynastonmary engAinda não há avaliações

- Private Commercial BanksDocumento7 páginasPrivate Commercial Banksjakia sultanaAinda não há avaliações

- Technical Anomalies: A Theoretical Review: Keywords: Technical Anomalies, Short-Term Momentum, Long-Run Return ReversalsDocumento8 páginasTechnical Anomalies: A Theoretical Review: Keywords: Technical Anomalies, Short-Term Momentum, Long-Run Return ReversalsAlan TurkAinda não há avaliações

- GLIFDocumento38 páginasGLIFTigmarashmi MahantaAinda não há avaliações

- Types of Business Organizations (Principles of Management)Documento5 páginasTypes of Business Organizations (Principles of Management)Mushima Tours & TransfersAinda não há avaliações

- Ireland - Shareholders Agreement Existing Company Shareholder DirectorsDocumento3 páginasIreland - Shareholders Agreement Existing Company Shareholder Directorsclark_taylorukAinda não há avaliações

- Demat and DepositoryDocumento19 páginasDemat and Depositorydjay sharmaAinda não há avaliações

- Regulatory Framework and Types of Depository ReceiptsDocumento22 páginasRegulatory Framework and Types of Depository ReceiptsJay PandyaAinda não há avaliações

- Financial Accounting 7th EditionDocumento4 páginasFinancial Accounting 7th Editiongilli1trAinda não há avaliações