Você também pode gostar

- Irregularities, Frauds and the Necessity of Technical Auditing in Construction IndustryNo EverandIrregularities, Frauds and the Necessity of Technical Auditing in Construction IndustryAinda não há avaliações

- Guidebook for Utilities-Led Business Models: Way Forward for Rooftop Solar in IndiaNo EverandGuidebook for Utilities-Led Business Models: Way Forward for Rooftop Solar in IndiaAinda não há avaliações

- Industrial Building Allowance (IBA)Documento32 páginasIndustrial Building Allowance (IBA)Ee LynnAinda não há avaliações

- Industrial Building Allowance-Notes (TAX370)Documento5 páginasIndustrial Building Allowance-Notes (TAX370)ewinze100% (1)

- Chapter 3B IBADocumento28 páginasChapter 3B IBAngutk91Ainda não há avaliações

- Chapter 2 - Industrial Building AllowanceDocumento49 páginasChapter 2 - Industrial Building AllowanceSri Renugha KaliaasanAinda não há avaliações

- Capital AllowanceDocumento6 páginasCapital AllowancedidieAinda não há avaliações

- Chapter 3 Agriculture Allowance StudntDocumento22 páginasChapter 3 Agriculture Allowance StudntCharmaine Deirdre DaveAinda não há avaliações

- Definition of Capital AllowancesDocumento9 páginasDefinition of Capital AllowancesAdesolaAinda não há avaliações

- F7.1 Chap 3 Tangible AssetDocumento47 páginasF7.1 Chap 3 Tangible AssetTrang TranAinda não há avaliações

- Ias 16Documento5 páginasIas 16Edga WariobaAinda não há avaliações

- 007 - Chapter 04 - IAS 16 Property, Plant and EquipmentDocumento7 páginas007 - Chapter 04 - IAS 16 Property, Plant and EquipmentHaris ButtAinda não há avaliações

- 6. Allowances (1)Documento52 páginas6. Allowances (1)biggoboziAinda não há avaliações

- IAS 16 Property, Plant and EquipmentDocumento9 páginasIAS 16 Property, Plant and Equipmentsalman jabbarAinda não há avaliações

- Capital Allowance 2220Documento58 páginasCapital Allowance 2220YanPing AngAinda não há avaliações

- IAS 40 - INVESTMENT PROPERTY - 2Documento53 páginasIAS 40 - INVESTMENT PROPERTY - 2penehafoshilengifaAinda não há avaliações

- Kuliah 1 Elaun Bangunan Industri (Industrial Building Allowances)Documento28 páginasKuliah 1 Elaun Bangunan Industri (Industrial Building Allowances)MUHAMMAD ZAWAWI BIN AYUP100% (1)

- Capital Allowances - PPTX 1Documento55 páginasCapital Allowances - PPTX 1sungurojephtertakudzwaAinda não há avaliações

- Chapter 6 Capital AllowanceDocumento59 páginasChapter 6 Capital AllowanceKailing KhowAinda não há avaliações

- Capital and Revenue ReceiptDocumento14 páginasCapital and Revenue ReceiptMuskan BohraAinda não há avaliações

- Chapter 6 Capital Allowance - Part 3 - IBADocumento18 páginasChapter 6 Capital Allowance - Part 3 - IBAPatricia TangAinda não há avaliações

- Property, Plant & EquipmentDocumento43 páginasProperty, Plant & Equipmenttobias jAinda não há avaliações

- FAR - Property, Plant and EquipmentDocumento7 páginasFAR - Property, Plant and EquipmentJohn Mahatma Agripa100% (2)

- Capital Allowances GuideDocumento32 páginasCapital Allowances GuideMakoni CharityAinda não há avaliações

- Capital AllowancesDocumento11 páginasCapital Allowancesfaith olaAinda não há avaliações

- Chapter 3b - Agriculture AllowanceDocumento19 páginasChapter 3b - Agriculture AllowanceNgAinda não há avaliações

- Capital AllowanceDocumento9 páginasCapital AllowanceAlfred MphandeAinda não há avaliações

- Capitalallowances 1Documento29 páginasCapitalallowances 1Teh Chu LeongAinda não há avaliações

- Chapter 3b - Agriculture AllowanceDocumento19 páginasChapter 3b - Agriculture AllowanceNgAinda não há avaliações

- Land, Building and MachineryDocumento26 páginasLand, Building and MachineryJirah DigalAinda não há avaliações

- Presentationprint TempDocumento67 páginasPresentationprint TempMd EndrisAinda não há avaliações

- Property, Plant, and Equipment - Initial RecognitionDocumento38 páginasProperty, Plant, and Equipment - Initial RecognitionCaila Nicole M. ReyesAinda não há avaliações

- AS Part 2Documento209 páginasAS Part 2hariinshrAinda não há avaliações

- Ias 16Documento31 páginasIas 16Reever RiverAinda não há avaliações

- Part D-8 Tangible non current assests (ch06)Documento68 páginasPart D-8 Tangible non current assests (ch06)hyangAinda não há avaliações

- As 10Documento14 páginasAs 10Tarique KhanAinda não há avaliações

- #20 Land, BLDG., & Machinery (Notes For 6204)Documento3 páginas#20 Land, BLDG., & Machinery (Notes For 6204)Zaaavnn VannnnnAinda não há avaliações

- Ias 16 PpeDocumento40 páginasIas 16 PpeziyuAinda não há avaliações

- Lecture Notes On PPE - Acq & RecDocumento6 páginasLecture Notes On PPE - Acq & Recjudel ArielAinda não há avaliações

- PPE - FinalDocumento71 páginasPPE - FinalKristen KooAinda não há avaliações

- As 10 - Fixed Assets - As Made EasyDocumento23 páginasAs 10 - Fixed Assets - As Made EasyraviAinda não há avaliações

- Lkas 16 - PpeDocumento45 páginasLkas 16 - PpeKogularamanan Nithiananthan100% (1)

- Chapter 3 - Agriculture AllowancesDocumento3 páginasChapter 3 - Agriculture AllowancesNURKHAIRUNNISA100% (2)

- ACC 1100 Days 14&15 Long-Lived Assets PDFDocumento25 páginasACC 1100 Days 14&15 Long-Lived Assets PDFYevhenii VdovenkoAinda não há avaliações

- IAS 16 GuideDocumento100 páginasIAS 16 GuideClarkMaasAinda não há avaliações

- Lecture 7fDocumento32 páginasLecture 7fHemant KumarAinda não há avaliações

- FR Revision Notes B1Documento6 páginasFR Revision Notes B1vandenberghchanellAinda não há avaliações

- Financial Accounting: Topic 2: Accounting For Plant AssetsDocumento58 páginasFinancial Accounting: Topic 2: Accounting For Plant AssetsDanielle ObenAinda não há avaliações

- Fixed Assets IAS 16Documento40 páginasFixed Assets IAS 16feliz100% (1)

- AO1M1Documento13 páginasAO1M1jashkishore0% (1)

- Lecture Notes On Capital Allowances and RecoupmentsDocumento53 páginasLecture Notes On Capital Allowances and RecoupmentsNchafie AsemahleAinda não há avaliações

- Investment Allowance Notes SummaryDocumento12 páginasInvestment Allowance Notes SummaryTriila manillaAinda não há avaliações

- Problems - PPE & DepnDocumento5 páginasProblems - PPE & DepnSaurabh SinghAinda não há avaliações

- Changing DepreciationDocumento12 páginasChanging DepreciationIsiyaku AdoAinda não há avaliações

- ABEN125 - Lecture 2Documento18 páginasABEN125 - Lecture 2PEARL ANGELIE UMBAAinda não há avaliações

- Capital Budgeting Cash FlowsDocumento13 páginasCapital Budgeting Cash FlowsNagaeshwary Murugan100% (1)

- Report On Sinclair CompanyDocumento5 páginasReport On Sinclair CompanyVictor LimAinda não há avaliações

- Case Study 1Documento6 páginasCase Study 1Narendra VaidyaAinda não há avaliações

- Chapter 9 Feb.19Documento69 páginasChapter 9 Feb.19AaaAinda não há avaliações

- Capital Allowance Guide for EducationDocumento41 páginasCapital Allowance Guide for EducationAgnesAinda não há avaliações

- Developing Your Own Case StudyDocumento33 páginasDeveloping Your Own Case StudyNero ShaAinda não há avaliações

- ICS Case Study (Ethical Dilemma)Documento1 páginaICS Case Study (Ethical Dilemma)Nero ShaAinda não há avaliações

- Integrating Sustainability Acctg Into MGT Practice-MainDocumento15 páginasIntegrating Sustainability Acctg Into MGT Practice-MainNero ShaAinda não há avaliações

- Chapter 5 - Personality ValuesDocumento32 páginasChapter 5 - Personality ValuesNero ShaAinda não há avaliações

- Topic 6 (PMS 1)Documento41 páginasTopic 6 (PMS 1)Nero ShaAinda não há avaliações

- Chapter 5 - Vision and Mission AnalysisDocumento40 páginasChapter 5 - Vision and Mission AnalysisNero Sha100% (5)

- Contemporary Performance Measurement SystemsDocumento36 páginasContemporary Performance Measurement SystemsNero ShaAinda não há avaliações

- Com Law Question 4Documento2 páginasCom Law Question 4Nero ShaAinda não há avaliações

- Walt Disney Strategic CaseDocumento28 páginasWalt Disney Strategic CaseArleneCastroAinda não há avaliações

- 3229 - Lecture 14 - Development in PSADocumento10 páginas3229 - Lecture 14 - Development in PSANero ShaAinda não há avaliações

- Lec14 ShariahDocumento21 páginasLec14 ShariahNero ShaAinda não há avaliações

- Lecture 12 - Working Capital and Current Assets ManagementDocumento76 páginasLecture 12 - Working Capital and Current Assets ManagementNero ShaAinda não há avaliações

- Project Planning ProcessDocumento23 páginasProject Planning ProcessNero ShaAinda não há avaliações

- ch17 SDocumento30 páginasch17 SNero ShaAinda não há avaliações

- Hindu Scientific FactsDocumento1 páginaHindu Scientific FactsNero ShaAinda não há avaliações

- The Source of Malaysian LawDocumento2 páginasThe Source of Malaysian LawNero ShaAinda não há avaliações

- Applicationform Undergrad 2014Documento4 páginasApplicationform Undergrad 2014Nero ShaAinda não há avaliações

- Study Link Personal StatementDocumento9 páginasStudy Link Personal StatementNero ShaAinda não há avaliações

- The Role of Tax Checks in The Determination of Taxes Owed (Case Study at Pt. Indonesian Railways)Documento9 páginasThe Role of Tax Checks in The Determination of Taxes Owed (Case Study at Pt. Indonesian Railways)International Journal of Innovative Science and Research TechnologyAinda não há avaliações

- P.V Number: 177394 Buyer Code: 2910004931695: Beaconhouse-Upper Mall Primary NTN 22-13-0786158-3 BCRDocumento1 páginaP.V Number: 177394 Buyer Code: 2910004931695: Beaconhouse-Upper Mall Primary NTN 22-13-0786158-3 BCRHassan NavidAinda não há avaliações

- Pakistan's Fertilizer Industry: An Analysis of Key Trends and DevelopmentsDocumento23 páginasPakistan's Fertilizer Industry: An Analysis of Key Trends and DevelopmentsShahzaib RazaAinda não há avaliações

- Covering Letter-For Karanam Ind-PebDocumento13 páginasCovering Letter-For Karanam Ind-PebswapnilAinda não há avaliações

- Finman ReviewerDocumento5 páginasFinman ReviewerCecilia TanAinda não há avaliações

- Market and Feasibility StudiesDocumento35 páginasMarket and Feasibility StudiesprinthubphAinda não há avaliações

- 11th BPS Arrears Income Tax Relief 89 1 RajManglamDocumento8 páginas11th BPS Arrears Income Tax Relief 89 1 RajManglamShubhamGuptaAinda não há avaliações

- Ghana Company Categories and FormsDocumento9 páginasGhana Company Categories and Formsben atAinda não há avaliações

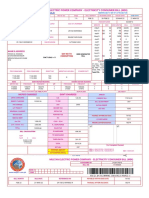

- Multan Electric Power Company - Electricity Consumer Bill (Mdi)Documento1 páginaMultan Electric Power Company - Electricity Consumer Bill (Mdi)Zohaib AhmadAinda não há avaliações

- Singapore L&F MarketDocumento62 páginasSingapore L&F MarketnarendraAinda não há avaliações

- Turkish Tax SystemDocumento3 páginasTurkish Tax Systemapi-3835399Ainda não há avaliações

- Chapter 8 - Refundable Tax Credits, Benefits and T1 AdjustmentsDocumento62 páginasChapter 8 - Refundable Tax Credits, Benefits and T1 AdjustmentsRyan YangAinda não há avaliações

- Financial Analysis Dr. Reddy'sDocumento9 páginasFinancial Analysis Dr. Reddy'sSoumya ChakrabortyAinda não há avaliações

- Financial Times UK. September 06, 2022Documento24 páginasFinancial Times UK. September 06, 2022Mãi Mãi LàbaoxaAinda não há avaliações

- Revocable Living TrustDocumento16 páginasRevocable Living TrustRoberto Monterrosa100% (7)

- Bustax Final ExamDocumento13 páginasBustax Final Examshudaye100% (3)

- Plumbing CodeDocumento154 páginasPlumbing Codedennis moreyAinda não há avaliações

- IGNTU EContent 456503968929 B.com 6 Prof - shailendraSinghBhadouriaDean& FINANCIALSERVICES AllDocumento4 páginasIGNTU EContent 456503968929 B.com 6 Prof - shailendraSinghBhadouriaDean& FINANCIALSERVICES AllDinesh PKAinda não há avaliações

- IncomeTax Chapter 8Documento17 páginasIncomeTax Chapter 8Marie Frances Sayson50% (2)

- Notice: Health Insurance Portability and Accountability Act of 1996 Implementation: Taxpayer Advocacy PanelsDocumento1 páginaNotice: Health Insurance Portability and Accountability Act of 1996 Implementation: Taxpayer Advocacy PanelsJustia.comAinda não há avaliações

- Evaluation of StakeholderDocumento3 páginasEvaluation of StakeholderTalha KhanAinda não há avaliações

- Cottage Savings Assn V CirDocumento7 páginasCottage Savings Assn V CirKTAinda não há avaliações

- En Bookcore Your-Booking Cb7d3krbg1 Print Lang enDocumento2 páginasEn Bookcore Your-Booking Cb7d3krbg1 Print Lang enneethu1995georgeAinda não há avaliações

- Balance Sheet and Financial Ratios for 2009 FYDocumento19 páginasBalance Sheet and Financial Ratios for 2009 FYpradeepkallurAinda não há avaliações

- Extra Book - June 2015 FinalDocumento84 páginasExtra Book - June 2015 Finaldanishzafar100% (1)

- Chemical Sector in IndiaDocumento11 páginasChemical Sector in IndiaAatmprakash MishraAinda não há avaliações

- RBWM Property Co LTD - Business PlanDocumento48 páginasRBWM Property Co LTD - Business PlanLeslie BonnerAinda não há avaliações

- Filing Requirements NotesDocumento42 páginasFiling Requirements NotesAllanAinda não há avaliações

- GST S4HANA Master Data ConfigurationDocumento6 páginasGST S4HANA Master Data ConfigurationAkshay GuptaAinda não há avaliações

- Foundations - Tax Exempt Foundations Their Impact On Our Economy US Gov 1962 140pgs PDFDocumento140 páginasFoundations - Tax Exempt Foundations Their Impact On Our Economy US Gov 1962 140pgs PDFjulianbreAinda não há avaliações