Você também pode gostar

- BMI ChartDocumento24 páginasBMI ChartMerlinda PacquiaoAinda não há avaliações

- Sebelum Senam Sesudah SenamDocumento12 páginasSebelum Senam Sesudah SenamKlinik Cempaka PutihAinda não há avaliações

- Export Unit Value & Volume Indices (2010 100), November 2022Documento6 páginasExport Unit Value & Volume Indices (2010 100), November 2022Fauzan SyahmiAinda não há avaliações

- Gerongan-Es-Endline-Ns 22-23Documento83 páginasGerongan-Es-Endline-Ns 22-23JANET ALMENANAAinda não há avaliações

- Rumus ' S ' Curve (Version 1)Documento7 páginasRumus ' S ' Curve (Version 1)Najib MuhammadAinda não há avaliações

- ANALYSIS OF EMPLOYEE PERFORMANCE, MOTIVATION, ORGANIZATIONAL CLIMATE AND COMMUNICATION VARIABLESDocumento5 páginasANALYSIS OF EMPLOYEE PERFORMANCE, MOTIVATION, ORGANIZATIONAL CLIMATE AND COMMUNICATION VARIABLESAguswan FurwendoAinda não há avaliações

- Sincua PS NS Endline 2022 2023Documento79 páginasSincua PS NS Endline 2022 2023JANET ALMENANAAinda não há avaliações

- Bets Remaining Win/Loss Kelly Bankroll Alternative Bankroll Win %Documento8 páginasBets Remaining Win/Loss Kelly Bankroll Alternative Bankroll Win %sandip_exlAinda não há avaliações

- Height-For-Age GIRLS: 5 To 19 Years (Z-Scores)Documento7 páginasHeight-For-Age GIRLS: 5 To 19 Years (Z-Scores)krisyantotigadaraAinda não há avaliações

- Realannualcommoditybasedexchangerates 1Documento22 páginasRealannualcommoditybasedexchangerates 1luizcorradini10Ainda não há avaliações

- Hfa Boys 5 19years ZDocumento7 páginasHfa Boys 5 19years ZYessy AndikaAinda não há avaliações

- Load Oriented Manufacturing Control (LOMC) Tugas Pertemuan 6Documento3 páginasLoad Oriented Manufacturing Control (LOMC) Tugas Pertemuan 6SEBRIELLA AULIA SIREGARAinda não há avaliações

- Nutritional Status - Five 2018Documento130 páginasNutritional Status - Five 2018icy clorionAinda não há avaliações

- Base plate capacity tables for column designDocumento7 páginasBase plate capacity tables for column designvtalexAinda não há avaliações

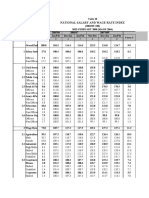

- National Salary and Wage Rate Index TrendsDocumento4 páginasNational Salary and Wage Rate Index TrendsMadhav BaralAinda não há avaliações

- SO2 Gas - Sulphur Burner Outlet Analysis Chart PDFDocumento2 páginasSO2 Gas - Sulphur Burner Outlet Analysis Chart PDFYalamati SatyanarayanaAinda não há avaliações

- Bmi g12 EmeraldDocumento487 páginasBmi g12 EmeraldGladzangel LoricabvAinda não há avaliações

- Descriptive Statistics: The Farthest Most People Ever GetDocumento53 páginasDescriptive Statistics: The Farthest Most People Ever GetpalanivelAinda não há avaliações

- Bmiwhf - Marj (Grade 7,8,9)Documento151 páginasBmiwhf - Marj (Grade 7,8,9)Beth PangilinanAinda não há avaliações

- Frequency TableDocumento6 páginasFrequency TableLê Hoàng VyAinda não há avaliações

- Tabela Psicométrica PDFDocumento4 páginasTabela Psicométrica PDFsoliveira_149796Ainda não há avaliações

- QC glucose analysis reportDocumento3 páginasQC glucose analysis reportPutri LendaAinda não há avaliações

- BMI 2022-2023 (1)Documento784 páginasBMI 2022-2023 (1)florriza bombioAinda não há avaliações

- BMI W HFA 15 Sec (5-29-17)Documento384 páginasBMI W HFA 15 Sec (5-29-17)Dang-dang QueAinda não há avaliações

- Nutritional Status EndlineDocumento108 páginasNutritional Status Endlineethel mae gabrielAinda não há avaliações

- NOTE-combined Analysis and Conclusion at The End : Year Item Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov DecDocumento9 páginasNOTE-combined Analysis and Conclusion at The End : Year Item Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov DecShreya TalujaAinda não há avaliações

- LJ Chart Electrolytes Dec 2022 - NewDocumento49 páginasLJ Chart Electrolytes Dec 2022 - NewKoton RoyAinda não há avaliações

- How to use the School Nutrition ProgramDocumento484 páginasHow to use the School Nutrition ProgramLorremae ArponAinda não há avaliações

- Nutritional Status FormDocumento529 páginasNutritional Status FormKaren Lozano ManqueriaAinda não há avaliações

- Pemetaan Daerah Resiko JenepontoDocumento2 páginasPemetaan Daerah Resiko JenepontoBayu KhonjoAinda não há avaliações

- Bmi Hfa Old FormsDocumento44 páginasBmi Hfa Old FormsPASDA ELEMAinda não há avaliações

- How to use the School Nutrition ProgramDocumento512 páginasHow to use the School Nutrition Programlyra mae maravillaAinda não há avaliações

- Free!: Program Features and Some Tips!Documento50 páginasFree!: Program Features and Some Tips!Analyn PenarandaAinda não há avaliações

- How to use the School Nutrition ProgramDocumento50 páginasHow to use the School Nutrition ProgramAnalyn PenarandaAinda não há avaliações

- Nutritional Status Bmi 2022 2023 BaselineDocumento781 páginasNutritional Status Bmi 2022 2023 BaselineAdelo MagnayeAinda não há avaliações

- Bmi Sy 2022-23 SoftDocumento996 páginasBmi Sy 2022-23 SoftRichdel TulabingAinda não há avaliações

- Nutritional Status Bmi 2022 2023 Baseline g10 DiscernmentDocumento781 páginasNutritional Status Bmi 2022 2023 Baseline g10 DiscernmentAdelo MagnayeAinda não há avaliações

- Ns - Software.elem With Grade 3Documento105 páginasNs - Software.elem With Grade 3ARLENE AQUINOAinda não há avaliações

- Nutritional Status EMERALDDocumento90 páginasNutritional Status EMERALDMaureen SantosAinda não há avaliações

- Free!: Program Features and Some Tips!Documento489 páginasFree!: Program Features and Some Tips!Yna Graciela BarcelonaAinda não há avaliações

- BMIWHF1Documento790 páginasBMIWHF1ELEANOR ERMITANIOAinda não há avaliações

- Grade 1 NSDocumento47 páginasGrade 1 NSMary Jennifer SoteloAinda não há avaliações

- BMI TVL NDocumento785 páginasBMI TVL NShiela Mie Malasaga BallonAinda não há avaliações

- How to use the School Nutrition ProgramDocumento97 páginasHow to use the School Nutrition ProgramBryan Landor TamayoAinda não há avaliações

- Miramar Nutritional Status 2021 2022 1Documento63 páginasMiramar Nutritional Status 2021 2022 1Yom KiroAinda não há avaliações

- Bmi VenusDocumento489 páginasBmi VenusLea SantueleAinda não há avaliações

- Grade 1 and 2Documento746 páginasGrade 1 and 2Romilyn QuiñoAinda não há avaliações

- Bmi Sy 2022-23 SoftDocumento996 páginasBmi Sy 2022-23 SoftRichdel TulabingAinda não há avaliações

- BMI W HFA 2018Documento996 páginasBMI W HFA 2018joshua doradoAinda não há avaliações

- Nutritional Status Ates 22 23 EndlineDocumento783 páginasNutritional Status Ates 22 23 EndlineLoreli AtesAinda não há avaliações

- Long BMI W HFA 215 Sec (4-15-2017)Documento996 páginasLong BMI W HFA 215 Sec (4-15-2017)Mary Rose ArengaAinda não há avaliações

- Bmi G9 Boyle Sy2023 2024Documento736 páginasBmi G9 Boyle Sy2023 2024Renalyn CastigadorAinda não há avaliações

- Rose Nutritional-Status 19-20 PostDocumento92 páginasRose Nutritional-Status 19-20 PostHaydee Fay GomezAinda não há avaliações

- Nutritional StatusDocumento44 páginasNutritional StatusEljhie AllabaAinda não há avaliações

- How to use this school nutrition programDocumento151 páginasHow to use this school nutrition programMarvelous Villafania100% (3)

- Auto Nutritional Status EndlineDocumento98 páginasAuto Nutritional Status EndlinearisuAinda não há avaliações

- BMI W HFA Validated 60 Sec (5!16!2017)Documento151 páginasBMI W HFA Validated 60 Sec (5!16!2017)Sheena San GabrielAinda não há avaliações

- Abby-Post BmiDocumento151 páginasAbby-Post BmiAbigael Abac RiveraAinda não há avaliações

- STUDENT PROJECT SabarishDocumento7 páginasSTUDENT PROJECT SabarishSriniAinda não há avaliações

- Heat Power Lab ManualDocumento68 páginasHeat Power Lab ManualRaghu KrishnanAinda não há avaliações

- Gas Turbines PDFDocumento3 páginasGas Turbines PDFSriniAinda não há avaliações

- Me6404 - Thermal EngineeringDocumento195 páginasMe6404 - Thermal EngineeringSasidharan MadhavikrishnankuttyAinda não há avaliações

- NEET 2017 Answer KeyDocumento21 páginasNEET 2017 Answer KeySriniAinda não há avaliações

- Effect of Speed On Boundary Friction ForceDocumento39 páginasEffect of Speed On Boundary Friction ForceSriniAinda não há avaliações

- Transmission Design Course MaterialDocumento116 páginasTransmission Design Course Materialharishankarnadar0% (1)

- TE Lab PDFDocumento79 páginasTE Lab PDFrkaruppasamyAinda não há avaliações

- Allen: Neet-2017 Test Paper With Answer & Solutions (Held On Sunday 07 MAY, 2017)Documento7 páginasAllen: Neet-2017 Test Paper With Answer & Solutions (Held On Sunday 07 MAY, 2017)Anurag LaddhaAinda não há avaliações

- Part A - AnswersDocumento7 páginasPart A - AnswersSriniAinda não há avaliações

- Thermal NotesDocumento192 páginasThermal NotesSriniAinda não há avaliações

- Gas TurbinesDocumento3 páginasGas TurbinesSriniAinda não há avaliações

- Chrompet VaishnavaDocumento2 páginasChrompet VaishnavaSriniAinda não há avaliações

- Morse Test On Multi Cylinder Petrol EngineDocumento4 páginasMorse Test On Multi Cylinder Petrol EnginealagurmAinda não há avaliações

- Solar Water Purifier 1Documento40 páginasSolar Water Purifier 1Srini0% (1)

- RPDocumento10 páginasRPpatilsspAinda não há avaliações

- Em QBDocumento24 páginasEm QBSriniAinda não há avaliações

- Rapid Prototyping NotesDocumento37 páginasRapid Prototyping NotesSriniAinda não há avaliações

- Graphics November - December 2011Documento2 páginasGraphics November - December 2011Dmj Anbu RajAinda não há avaliações

- Scanned by CamscannerDocumento4 páginasScanned by CamscannerSriniAinda não há avaliações

- 3yr 1sem Mech Thermal Engineering Lab ManualDocumento85 páginas3yr 1sem Mech Thermal Engineering Lab Manualrahulmahesh3A6Ainda não há avaliações

- Scanned by CamscannerDocumento4 páginasScanned by CamscannerSriniAinda não há avaliações

- Conduction and Heat ExchangersDocumento1 páginaConduction and Heat ExchangersSriniAinda não há avaliações

- Unit - IDocumento19 páginasUnit - ISriniAinda não há avaliações

- Gate Model Test 1Documento3 páginasGate Model Test 1SriniAinda não há avaliações

- FMM Cycle Test 3Documento2 páginasFMM Cycle Test 3SriniAinda não há avaliações

- Mech 32 HT Lab ManualDocumento74 páginasMech 32 HT Lab Manualalp_alp100% (1)

- HMT5Documento9 páginasHMT5SriniAinda não há avaliações

- AUT R2010 SyllabusDocumento1 páginaAUT R2010 SyllabusSriniAinda não há avaliações

- Low rank tensor product smooths for GAMMsDocumento24 páginasLow rank tensor product smooths for GAMMsDiego SotoAinda não há avaliações

- WaidhanDocumento86 páginasWaidhanPatel Nitesh OadAinda não há avaliações

- Listening Script 11Documento11 páginasListening Script 11harshkumarbhallaAinda não há avaliações

- List of SDAsDocumento4 páginasList of SDAsAthouba SagolsemAinda não há avaliações

- Azura Amid (Eds.) - Recombinant Enzymes - From Basic Science To Commercialization-Springer International Publishing (2015) PDFDocumento191 páginasAzura Amid (Eds.) - Recombinant Enzymes - From Basic Science To Commercialization-Springer International Publishing (2015) PDFnurul qAinda não há avaliações

- Introducing The Phenomenon To Be Discussed: Stating Your OpinionDocumento8 páginasIntroducing The Phenomenon To Be Discussed: Stating Your OpinionRam RaghuwanshiAinda não há avaliações

- A Study To Assess The Effectiveness of PDocumento9 páginasA Study To Assess The Effectiveness of PKamal JindalAinda não há avaliações

- AI Berkeley Solution PDFDocumento9 páginasAI Berkeley Solution PDFPrathamGuptaAinda não há avaliações

- Sensor Guide: Standard Triaxial Geophones Specialty Triaxial Geophones Standard Overpressure MicrophonesDocumento1 páginaSensor Guide: Standard Triaxial Geophones Specialty Triaxial Geophones Standard Overpressure MicrophonesDennis Elias TaipeAinda não há avaliações

- Graffiti Model Lesson PlanDocumento9 páginasGraffiti Model Lesson Planapi-286619177100% (1)

- Configure NTP, OSPF, logging and SSH on routers R1, R2 and R3Documento2 páginasConfigure NTP, OSPF, logging and SSH on routers R1, R2 and R3Lars Rembrandt50% (2)

- 6907 6 52 0040Documento35 páginas6907 6 52 0040amitkumar8946Ainda não há avaliações

- Frame Fit Specs SramDocumento22 páginasFrame Fit Specs SramJanekAinda não há avaliações

- Toolbox Meeting Or, TBT (Toolbox TalkDocumento10 páginasToolbox Meeting Or, TBT (Toolbox TalkHarold PonceAinda não há avaliações

- Vehicle Tracker Offer SheetDocumento1 páginaVehicle Tracker Offer SheetBihun PandaAinda não há avaliações

- Capacitor BanksDocumento49 páginasCapacitor BanksAmal P RaviAinda não há avaliações

- Test 420001 PDFDocumento13 páginasTest 420001 PDFmaria100% (1)

- Obeid Specialized Hospital - Riyadh: Inpatient DeptsDocumento4 páginasObeid Specialized Hospital - Riyadh: Inpatient DeptsLovelydePerioAinda não há avaliações

- Adiabatic Production of Acetic AnhydrideDocumento7 páginasAdiabatic Production of Acetic AnhydrideSunilParjapatiAinda não há avaliações

- Katja Kruckeberg, Wolfgang Amann, Mike Green-Leadership and Personal Development - A Toolbox For The 21st Century Professional-Information Age Publishing (2011)Documento383 páginasKatja Kruckeberg, Wolfgang Amann, Mike Green-Leadership and Personal Development - A Toolbox For The 21st Century Professional-Information Age Publishing (2011)MariaIoanaTelecan100% (1)

- 10 ExtSpringsDocumento27 páginas10 ExtSpringsresh27Ainda não há avaliações

- Schippers and Bendrup - Ethnomusicology Ecology and SustainabilityDocumento12 páginasSchippers and Bendrup - Ethnomusicology Ecology and SustainabilityLuca GambirasioAinda não há avaliações

- Marginal Field Development Concepts (Compatibility Mode)Documento17 páginasMarginal Field Development Concepts (Compatibility Mode)nallay1705100% (1)

- CH - 1Documento4 páginasCH - 1Phantom GamingAinda não há avaliações

- Air Cooled Screw Chiller Performance SpecificationDocumento2 páginasAir Cooled Screw Chiller Performance SpecificationDajuko Butarbutar100% (1)

- Methanol Technical Data Sheet FactsDocumento1 páginaMethanol Technical Data Sheet FactsmkgmotleyAinda não há avaliações

- An Introduction to Heisenberg Groups in Analysis and GeometryDocumento7 páginasAn Introduction to Heisenberg Groups in Analysis and Geometrynitrosc16703Ainda não há avaliações

- Fire InsuranceDocumento108 páginasFire Insurancem_dattaias88% (8)

- Overview On Image Captioning TechniquesDocumento6 páginasOverview On Image Captioning TechniquesWARSE JournalsAinda não há avaliações

- Electronics Today 1977 10Documento84 páginasElectronics Today 1977 10cornel_24100% (3)