Você também pode gostar

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (120)

- Linnea BookshelfDocumento3 páginasLinnea BookshelfMiguel Alfonso Estrada Cerrato100% (1)

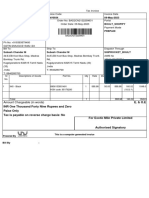

- Exotic Mile Private Limited BINV0934 09-May-2023 Boult - ShopifyDocumento1 páginaExotic Mile Private Limited BINV0934 09-May-2023 Boult - ShopifyMellodie GamingAinda não há avaliações

- ISO 14001 Auditing ChecklistDocumento45 páginasISO 14001 Auditing ChecklistPercy MphulanyaneAinda não há avaliações

- Hasbro Q3 2023 Earnings Management RemarksDocumento9 páginasHasbro Q3 2023 Earnings Management RemarksDionnelle VillalobosAinda não há avaliações

- Puma Energy Sustainability Report 2022Documento34 páginasPuma Energy Sustainability Report 2022Oscar Raul Ynan AndersonAinda não há avaliações

- Final Consulting Project 394-3Documento4 páginasFinal Consulting Project 394-3AD RAinda não há avaliações

- Case Study Amazon ObDocumento2 páginasCase Study Amazon ObMama SihamAinda não há avaliações

- 17e GNB CH05 SMDocumento169 páginas17e GNB CH05 SMRidwanur Rahman 26-195Ainda não há avaliações

- Supply C1 C4Documento4 páginasSupply C1 C4shielamayavillanueva25Ainda não há avaliações

- A Survey To Study Consumer Satisfaction Towards Samsung Smart Watches in Varanasi CityDocumento12 páginasA Survey To Study Consumer Satisfaction Towards Samsung Smart Watches in Varanasi CityinfoAinda não há avaliações

- Best Frequency Strategies - How Often To Post On Social Media PDFDocumento24 páginasBest Frequency Strategies - How Often To Post On Social Media PDFLiet CanasAinda não há avaliações

- Instruction Manual: Kids Teepee TentDocumento4 páginasInstruction Manual: Kids Teepee TentRrsc RamsAinda não há avaliações

- Kaplan Homes Price List 2020Documento8 páginasKaplan Homes Price List 2020Tonnie LamAinda não há avaliações

- Chapter 1Documento47 páginasChapter 1honeyAinda não há avaliações

- MGT201 Pass PaperDocumento55 páginasMGT201 Pass PaperNaresh ShewaniAinda não há avaliações

- Auxiliar de Repaso: Pregunta 1Documento7 páginasAuxiliar de Repaso: Pregunta 1hectorfa1Ainda não há avaliações

- Sample Essay EducationDocumento8 páginasSample Essay Educationajdegacaf100% (2)

- Application For The Issuance of LabelsDocumento1 páginaApplication For The Issuance of LabelsLee LimAinda não há avaliações

- 2015 SALN Form BLANK 1 Annex 35 For Saln 2022Documento2 páginas2015 SALN Form BLANK 1 Annex 35 For Saln 2022Bediones Econ ClassAinda não há avaliações

- FM II Assignment 12 W22Documento2 páginasFM II Assignment 12 W22Farah ImamiAinda não há avaliações

- Cover 1 4Documento4 páginasCover 1 4kumara1986Ainda não há avaliações

- Executive Summary: The ConceptDocumento8 páginasExecutive Summary: The Conceptcamile buhanginAinda não há avaliações

- Lockwood, T - Design - Thinking PDFDocumento3 páginasLockwood, T - Design - Thinking PDFandrehluna0% (2)

- PT. Makmur Berkat Solusi: Company Profile 2020Documento19 páginasPT. Makmur Berkat Solusi: Company Profile 2020Dea Candra Ivana PutriAinda não há avaliações

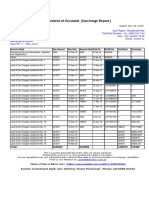

- Surcharge Report BTKSC-P05164Documento1 páginaSurcharge Report BTKSC-P05164Nasir Badshah AfridiAinda não há avaliações

- Always PadsDocumento12 páginasAlways PadsAiaman ShahzadAinda não há avaliações

- NTSGEPCO 22 - Candidate (Portal)Documento2 páginasNTSGEPCO 22 - Candidate (Portal)DaneshAinda não há avaliações

- Advertising Planning & StrategyDocumento29 páginasAdvertising Planning & StrategyMALAY KUMARAinda não há avaliações

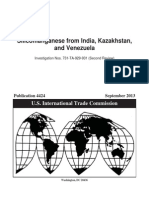

- 4424 PDFDocumento162 páginas4424 PDFmonish147852Ainda não há avaliações

- Godrej Consumer ProductsDocumento6 páginasGodrej Consumer ProductsRuchika SinghAinda não há avaliações