Você também pode gostar

- Barangay BudgetingDocumento25 páginasBarangay BudgetingEarthAngel OrganicsAinda não há avaliações

- Annual Investment Program CY 2016Documento125 páginasAnnual Investment Program CY 2016Carl100% (1)

- NEOP First 100 Days For Municipal Mayors Edited 1Documento89 páginasNEOP First 100 Days For Municipal Mayors Edited 1Eden GesmundoAinda não há avaliações

- Guidelines and Mechanics: 6 Re-Dated Arawngtibungco Cheerdance CompetitionDocumento4 páginasGuidelines and Mechanics: 6 Re-Dated Arawngtibungco Cheerdance CompetitionAl SimbajonAinda não há avaliações

- DILG Full Disclosure PolicyDocumento6 páginasDILG Full Disclosure PolicyHelen FabraAinda não há avaliações

- Certificate of Availability of Funds (CAF)Documento1 páginaCertificate of Availability of Funds (CAF)Al Simbajon100% (3)

- Module 2 - Formulation of BADAC Plan of ActionDocumento42 páginasModule 2 - Formulation of BADAC Plan of ActionSharamae Dalogdog100% (3)

- October 2010 Als A& E Test PassresDocumento200 páginasOctober 2010 Als A& E Test Passresallen1006g53% (19)

- Ellen's PPT BFDPDocumento19 páginasEllen's PPT BFDParaceli aure-naciongayoAinda não há avaliações

- Annex 7 - C: Fy - Annual Investment Program (Aip) by Program/Project/Activity by SectorDocumento1 páginaAnnex 7 - C: Fy - Annual Investment Program (Aip) by Program/Project/Activity by SectorCarl Francis Cariaso100% (1)

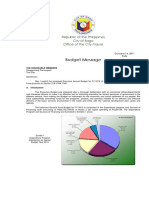

- Budget Message: Republic of The Philippines City of Bago Office of The City MayorDocumento3 páginasBudget Message: Republic of The Philippines City of Bago Office of The City MayorAl SimbajonAinda não há avaliações

- 7083 Assessment of Barangay Nutrition Program Implementation in Selected Municipalities in Ifugao Bulacan and Siquijor Community Partners Perspectives PDFDocumento9 páginas7083 Assessment of Barangay Nutrition Program Implementation in Selected Municipalities in Ifugao Bulacan and Siquijor Community Partners Perspectives PDFAl SimbajonAinda não há avaliações

- MADAC LogfaDocumento5 páginasMADAC LogfaJomidy MidtanggalAinda não há avaliações

- 7 Dilg BLGD Lgu DTP GuidelinesDocumento23 páginas7 Dilg BLGD Lgu DTP GuidelinesDILG Naga50% (2)

- Solicitation LettersDocumento3 páginasSolicitation LettersAl SimbajonAinda não há avaliações

- Solicitation LettersDocumento3 páginasSolicitation LettersAl SimbajonAinda não há avaliações

- EP With CDRADocumento89 páginasEP With CDRARheii EstandarteAinda não há avaliações

- State Universities and Colleges DirectoryDocumento21 páginasState Universities and Colleges DirectoryMaylene UdtojanAinda não há avaliações

- 2019 Barangay FormsDocumento16 páginas2019 Barangay FormsHelen Marie PatindolAinda não há avaliações

- LECTURE 07 Comprehensive Development PlanDocumento30 páginasLECTURE 07 Comprehensive Development PlanTJ BungayAinda não há avaliações

- Activity Design - ADAC StrengtheningDocumento3 páginasActivity Design - ADAC StrengtheningRee MaslogAinda não há avaliações

- MPDO Citizen's Charter SampleDocumento11 páginasMPDO Citizen's Charter Sampleryanpacabis23Ainda não há avaliações

- Local Youth Development Plan: City of DanaoDocumento11 páginasLocal Youth Development Plan: City of DanaoJohn Keach CoyocaAinda não há avaliações

- Barangay GFPSDocumento18 páginasBarangay GFPSVinvin EsoenAinda não há avaliações

- Vawc Desk OrdinanceDocumento2 páginasVawc Desk OrdinanceAl Simbajon88% (58)

- Advisory Calendar of Barangay Mandatory DeliverablesDocumento9 páginasAdvisory Calendar of Barangay Mandatory DeliverablesJo ReyesAinda não há avaliações

- AIP Blank Form 2020Documento1 páginaAIP Blank Form 2020Johara Soriano0% (1)

- Guidelines On LYDP CBYDP and ABYIPv2024 FINALDocumento31 páginasGuidelines On LYDP CBYDP and ABYIPv2024 FINALDILG IBAJAYAinda não há avaliações

- BDP MessageDocumento1 páginaBDP MessageAl Simbajon89% (9)

- Badac Action PlanDocumento2 páginasBadac Action PlanAl Simbajon100% (18)

- Annex A. LCPC WFP Form 001 CDocumento1 páginaAnnex A. LCPC WFP Form 001 CRhapAinda não há avaliações

- New CDP PPT Session 3 - CDP ProcessDocumento33 páginasNew CDP PPT Session 3 - CDP ProcessnagtipunanAinda não há avaliações

- DTP CapDev Agenda With BrgyDocumento83 páginasDTP CapDev Agenda With BrgyRoxanne Vicedo100% (1)

- Accreditation Form BarangayDocumento7 páginasAccreditation Form BarangayAl Simbajon100% (3)

- To Print Core ValuesDocumento50 páginasTo Print Core ValuesJeraldine RepolloAinda não há avaliações

- GAD Planning (JMC 2016-01)Documento109 páginasGAD Planning (JMC 2016-01)Maria Fiona Duran MerquitaAinda não há avaliações

- Basics of Barangay Development Planning: BNEO Online CourseDocumento40 páginasBasics of Barangay Development Planning: BNEO Online CourseJOSEL PEREZ ENRILE100% (2)

- ADVISORY Re 2021 PILOT TESTING OF THE SEAL OF GOOD LOCAL GOVERNANCE FOR BARANGAY SGLGBDocumento73 páginasADVISORY Re 2021 PILOT TESTING OF THE SEAL OF GOOD LOCAL GOVERNANCE FOR BARANGAY SGLGBDonavel Nodora Jojuico100% (1)

- BADAC EoDocumento4 páginasBADAC EoAl Simbajon95% (60)

- Functionality Assessment of The Barangay Development Council (BDC)Documento27 páginasFunctionality Assessment of The Barangay Development Council (BDC)DILG Isabela CICAinda não há avaliações

- Bpops Template (Plan)Documento1 páginaBpops Template (Plan)Al Simbajon95% (19)

- Gad Focal Point SystemDocumento2 páginasGad Focal Point SystemAl Simbajon100% (4)

- 7 Basics of BDPDocumento39 páginas7 Basics of BDPCLUSTER II DILGTARLACAinda não há avaliações

- Barangay Business Clearance: Barangay Officials: Ricardo Callueng JRDocumento5 páginasBarangay Business Clearance: Barangay Officials: Ricardo Callueng JRAl SimbajonAinda não há avaliações

- Form 1 LGU Profile PDFDocumento6 páginasForm 1 LGU Profile PDFArt Henrhey Bulic50% (2)

- BPOPS Accomplishment ReportDocumento1 páginaBPOPS Accomplishment ReportAl Simbajon88% (24)

- Draft Ordinance - CSO Participation - v2Documento12 páginasDraft Ordinance - CSO Participation - v2Miamor NatividadAinda não há avaliações

- CDP Assessment ToolDocumento20 páginasCDP Assessment ToolDilg Rizal Province0% (1)

- Vawc Desk EoDocumento2 páginasVawc Desk EoAl Simbajon71% (7)

- Executive Legislative FormulationDocumento47 páginasExecutive Legislative FormulationSing KhoAinda não há avaliações

- SLPBC Presentation DILGDocumento24 páginasSLPBC Presentation DILGDanpaul SantosAinda não há avaliações

- SGLG Scorecard PresentationDocumento22 páginasSGLG Scorecard PresentationRey Jan Sly100% (1)

- Joint Memorandum Circular No 1 S 2007Documento12 páginasJoint Memorandum Circular No 1 S 2007tikboyblueAinda não há avaliações

- Bgy Development PlanningDocumento35 páginasBgy Development PlanningRom LiwAinda não há avaliações

- Contemporary Phil ArtsDocumento36 páginasContemporary Phil ArtsGinle SatumcacalAinda não há avaliações

- DTP For Barangay Introduction and FSFDocumento32 páginasDTP For Barangay Introduction and FSFGem BesandeAinda não há avaliações

- Sectoral StudiesDocumento108 páginasSectoral StudiesIan Yoselle Narciso100% (1)

- Dilg Reports Resources 202064 - 09a370057c PDFDocumento52 páginasDilg Reports Resources 202064 - 09a370057c PDFJayson De LemonAinda não há avaliações

- RCSP Guidelines - Dilg7Documento73 páginasRCSP Guidelines - Dilg7MaricelBaguinonOchate-NaragaAinda não há avaliações

- Gad DutiesDocumento9 páginasGad DutiesRohaina Sapal100% (1)

- Cert Honors - Acad AchieversDocumento40 páginasCert Honors - Acad AchieversMary Joyce CuiAinda não há avaliações

- LPTRP Manual Volume 1.2Documento185 páginasLPTRP Manual Volume 1.2minari myouiAinda não há avaliações

- BNEO Development Planning PresentationDocumento38 páginasBNEO Development Planning PresentationBadidz Ong Suco100% (1)

- Types of Analogies: Activity Sheet in English Grade 7Documento3 páginasTypes of Analogies: Activity Sheet in English Grade 7Fernan Enad100% (2)

- Barangay Development Planning: Dilg CalabarzonDocumento34 páginasBarangay Development Planning: Dilg CalabarzonEd Seng100% (1)

- ANNEX B. Form 3b Project Brief For Each PPA SantaFeDocumento84 páginasANNEX B. Form 3b Project Brief For Each PPA SantaFePrincess Hayria B. PiangAinda não há avaliações

- ELA CAPDEV Presentation 2022Documento85 páginasELA CAPDEV Presentation 2022aeron antonioAinda não há avaliações

- Science DLL Grade 7 - Quarter 2Documento47 páginasScience DLL Grade 7 - Quarter 2Marl Rina Esperanza100% (1)

- Bid Form GoodsDocumento2 páginasBid Form GoodsAl SimbajonAinda não há avaliações

- Brgy Devt PlanningDocumento50 páginasBrgy Devt PlanningJeprox Lora100% (1)

- Letter To COADocumento1 páginaLetter To COAAl SimbajonAinda não há avaliações

- Solicitation Letters ConstructionDocumento1 páginaSolicitation Letters ConstructionAl Simbajon100% (2)

- Bac Reso SampleDocumento2 páginasBac Reso SampleAl SimbajonAinda não há avaliações

- Executive-Legislative Agenda For Davao City: City Director Vicky P. Sarcena DILG Davao City OfficeDocumento33 páginasExecutive-Legislative Agenda For Davao City: City Director Vicky P. Sarcena DILG Davao City OfficeHannah Cris Azcona Echavez100% (1)

- Formulation/Updating OF THE Barangay Development Plan (BDP)Documento15 páginasFormulation/Updating OF THE Barangay Development Plan (BDP)Operations Primus100% (1)

- Executive-Legislative Agenda FormulationDocumento7 páginasExecutive-Legislative Agenda FormulationBryan RiveraAinda não há avaliações

- 2021 Local Government Functionality Appraisal (Logfa) Indicator and Rating ReferenceDocumento15 páginas2021 Local Government Functionality Appraisal (Logfa) Indicator and Rating ReferenceAnn ManaloconAinda não há avaliações

- Revised BGPMS ManualDocumento43 páginasRevised BGPMS Manuallovels23100% (7)

- ELA Formulation ProcessDocumento12 páginasELA Formulation ProcessRODEL D. HILARIOAinda não há avaliações

- Briefer On CFLGA and SCFLG - Updated 01 Sept 21Documento39 páginasBriefer On CFLGA and SCFLG - Updated 01 Sept 21lothyAinda não há avaliações

- Design - Clup Public HearingDocumento2 páginasDesign - Clup Public HearingMENRO KiambaAinda não há avaliações

- Masa MasidDocumento19 páginasMasa MasidDilg Talomo Toril100% (11)

- ANNUAL LCCAP (Sto - Tomas)Documento16 páginasANNUAL LCCAP (Sto - Tomas)Bienvenido TamondongAinda não há avaliações

- RPMES ManualDocumento92 páginasRPMES ManualJam ColasAinda não há avaliações

- ELA Formulation ProcessDocumento12 páginasELA Formulation ProcessRODEL D. HILARIOAinda não há avaliações

- BDRRM Plan Template EnglishDocumento44 páginasBDRRM Plan Template EnglishRodnie AlburoAinda não há avaliações

- Legends: Basic-20%, Progressive-21-50%, Mature - 51-79% and Ideal - 80-100% - Bonus PointDocumento3 páginasLegends: Basic-20%, Progressive-21-50%, Mature - 51-79% and Ideal - 80-100% - Bonus PointEthelyne DomingoAinda não há avaliações

- End-User/Unit: Barangay Charged To: General Fund Projects, Programs and Activities (Paps)Documento1 páginaEnd-User/Unit: Barangay Charged To: General Fund Projects, Programs and Activities (Paps)Ruel Umali ZagadoAinda não há avaliações

- MLG20 5 Units 1Documento1 páginaMLG20 5 Units 1Al SimbajonAinda não há avaliações

- Barangay Budgeting Workbook: User'S Manual: A. Introduction A. IntroductionDocumento11 páginasBarangay Budgeting Workbook: User'S Manual: A. Introduction A. IntroductionJuvy RascoAinda não há avaliações

- Cutting CertificationDocumento9 páginasCutting CertificationAl Simbajon50% (2)

- By-Laws Rules and Regs UpdatedDocumento30 páginasBy-Laws Rules and Regs UpdatedAl SimbajonAinda não há avaliações

- BOHOLDocumento66 páginasBOHOLAl SimbajonAinda não há avaliações

- Page 1 of 1Documento3 páginasPage 1 of 1Al SimbajonAinda não há avaliações

- Bid Form InfraDocumento3 páginasBid Form InfraAl SimbajonAinda não há avaliações

- Hta Alumni Batch 90 Scholarship Program: InitiativeDocumento2 páginasHta Alumni Batch 90 Scholarship Program: InitiativeAl SimbajonAinda não há avaliações

- Local Budget Memorandum No 77 ADocumento22 páginasLocal Budget Memorandum No 77 AAl SimbajonAinda não há avaliações

- Invitation To Bid SampleDocumento2 páginasInvitation To Bid SampleAl SimbajonAinda não há avaliações

- 2023 NHWSS Orientation ScheduleDocumento2 páginas2023 NHWSS Orientation ScheduleMary April Ann VistarAinda não há avaliações

- 4c Status Report On Star Rating of DPWH Reg'l. & District Matl's. Testing Labs.Documento8 páginas4c Status Report On Star Rating of DPWH Reg'l. & District Matl's. Testing Labs.Yuri ValenciaAinda não há avaliações

- Gordon College: Detailed Learning Module inDocumento62 páginasGordon College: Detailed Learning Module inPaula Marie BialaAinda não há avaliações

- Region 7 CentralvisayasDocumento3 páginasRegion 7 CentralvisayasLiaa Angelique BaranganAinda não há avaliações

- Emergency NumbersDocumento2 páginasEmergency NumbersDiego DionsonAinda não há avaliações

- Vistamar (5-17-2012)Documento86 páginasVistamar (5-17-2012)restomataAinda não há avaliações

- Region 7-8 Central and Eastern Visayas PDFDocumento95 páginasRegion 7-8 Central and Eastern Visayas PDFdafuq 12344Ainda não há avaliações

- RD Survey Report 2018Documento106 páginasRD Survey Report 2018Roldan CallejaAinda não há avaliações

- Philippine Indigenous Community: Name: Marzon, Jeraldin R. Section Code and Schedule: Pced-03-401PDocumento64 páginasPhilippine Indigenous Community: Name: Marzon, Jeraldin R. Section Code and Schedule: Pced-03-401PDen-den Roble MarzonAinda não há avaliações

- Form 14Documento4 páginasForm 14WinstonEnriquezFernandezAinda não há avaliações

- Schools Division of Negros Oriental: Accomplishment ReportDocumento6 páginasSchools Division of Negros Oriental: Accomplishment ReportMacrina VillaluzAinda não há avaliações

- 2014 Als A&E Test - Elementary Level Test PassersDocumento189 páginas2014 Als A&E Test - Elementary Level Test PassersBrylleAinda não há avaliações

- Republic of The Philippines: Days of Work Attendance and Time and PeriodDocumento6 páginasRepublic of The Philippines: Days of Work Attendance and Time and PeriodDecelyn RaboyAinda não há avaliações

- Certification of TransferDocumento5 páginasCertification of TransferDebra Cuyos DuabanAinda não há avaliações

- Mapeh Monitoring ProgressDocumento1 páginaMapeh Monitoring ProgressMelvin Yolle SantillanaAinda não há avaliações

- MFAT ToolDocumento7 páginasMFAT Toollucena cenaAinda não há avaliações

- RegionsDocumento20 páginasRegionsbhongskirnAinda não há avaliações

- 2023 TargetDocumento1.078 páginas2023 TargetCris GapasAinda não há avaliações

- New Memo ComelecDocumento6 páginasNew Memo ComelecNikerose BelaguasAinda não há avaliações

- New List QRFDocumento4 páginasNew List QRFTeddie B. YapAinda não há avaliações

- Transportation Study Metropolitan CEBU - A Case StudyDocumento150 páginasTransportation Study Metropolitan CEBU - A Case StudyAira SofiaAinda não há avaliações

- Registry of Trainings AttendedDocumento7 páginasRegistry of Trainings AttendedGifsy Robledo CastroAinda não há avaliações