Você também pode gostar

- Get Rich with Dividends: A Proven System for Earning Double-Digit ReturnsNo EverandGet Rich with Dividends: A Proven System for Earning Double-Digit ReturnsAinda não há avaliações

- Equity Valuation: Models from Leading Investment BanksNo EverandEquity Valuation: Models from Leading Investment BanksJan ViebigAinda não há avaliações

- NeoGames Investor Presentation (11.10.21) - v2 PDFDocumento35 páginasNeoGames Investor Presentation (11.10.21) - v2 PDFEmmanuel Emiliano Reyes FuentesAinda não há avaliações

- I. Case BackgroundDocumento7 páginasI. Case BackgroundHiya BhandariBD21070Ainda não há avaliações

- Fourth Quarter 2010 Earnings Review: January 18, 2011Documento36 páginasFourth Quarter 2010 Earnings Review: January 18, 2011oliverzzeng1152Ainda não há avaliações

- Citigroup - Financial Summary: 1Q 2Q 3Q 4Q 2004 2004 2004 2004Documento5 páginasCitigroup - Financial Summary: 1Q 2Q 3Q 4Q 2004 2004 2004 2004Mark ReinhardtAinda não há avaliações

- Model Assignment Aug-23Documento3 páginasModel Assignment Aug-23Abner ogegaAinda não há avaliações

- Ceres Gardening CompanyDocumento6 páginasCeres Gardening Companypallavikotha84Ainda não há avaliações

- Case 20 Target Corporation 1Documento37 páginasCase 20 Target Corporation 1hnooy100% (1)

- Simple LBO Model - Equity Value and Enterprise Value in A Cash-Free, Debt-Free DealDocumento2 páginasSimple LBO Model - Equity Value and Enterprise Value in A Cash-Free, Debt-Free Dealmerag76668Ainda não há avaliações

- Nasdaq Aaon 2014Documento76 páginasNasdaq Aaon 2014gaja babaAinda não há avaliações

- IMT CeresDocumento5 páginasIMT Ceresnikhil hoodaAinda não há avaliações

- Chapter 4 SolutionsDocumento5 páginasChapter 4 SolutionsapremsAinda não há avaliações

- Company A Financial Statement S$ Million Year 0 Year 1 Year 2 Total Total TotalDocumento14 páginasCompany A Financial Statement S$ Million Year 0 Year 1 Year 2 Total Total TotalAARZOO DEWANAinda não há avaliações

- CASE Solution VyadermDocumento8 páginasCASE Solution VyadermIshan Shah100% (2)

- Practice Exam 3Documento7 páginasPractice Exam 3AndresAinda não há avaliações

- Executive Officers and Capital Expenditure Committee MembersDocumento37 páginasExecutive Officers and Capital Expenditure Committee MembersKritikaPandeyAinda não há avaliações

- Att Ar 2012 ManagementDocumento35 páginasAtt Ar 2012 ManagementDevandro MahendraAinda não há avaliações

- Nasdaq Aaon 2011Documento72 páginasNasdaq Aaon 2011gaja babaAinda não há avaliações

- IMT CeresDocumento7 páginasIMT Ceresraman.joshi751Ainda não há avaliações

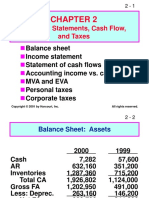

- Financial Statements, Cash Flow, and TaxesDocumento44 páginasFinancial Statements, Cash Flow, and TaxesJuliani Tania RizkyAinda não há avaliações

- BCG Forage Core Strategy - Telco (Task 2 Additional Data)Documento11 páginasBCG Forage Core Strategy - Telco (Task 2 Additional Data)Akshay rajAinda não há avaliações

- FactBookFY 2021andq1 2022Documento26 páginasFactBookFY 2021andq1 2022Prateek PandeyAinda não há avaliações

- Practice Exam - SolutionsDocumento12 páginasPractice Exam - SolutionsSu Suan TanAinda não há avaliações

- Cloudpoint Technology Berhad IPO Prospectus 9 May 2023 Part 2Documento154 páginasCloudpoint Technology Berhad IPO Prospectus 9 May 2023 Part 2Oliver Oscar100% (1)

- HLX 2011arDocumento158 páginasHLX 2011arMike MaguireAinda não há avaliações

- Intel Corporation Q2 2010 Earnings Review: ATF CapitalDocumento6 páginasIntel Corporation Q2 2010 Earnings Review: ATF CapitalAndre SetiawanAinda não há avaliações

- Vyaderm Caseanalysis PDFDocumento6 páginasVyaderm Caseanalysis PDFSahil Azher RashidAinda não há avaliações

- ch02 Financial Statement, Cash Flows and TaxesDocumento30 páginasch02 Financial Statement, Cash Flows and TaxesAffan AhmedAinda não há avaliações

- BCG Forage Core Strategy - Telco (Task 2 Additional Data)Documento11 páginasBCG Forage Core Strategy - Telco (Task 2 Additional Data)Fadil JauhariAinda não há avaliações

- Annual Report 2015 EN 2 PDFDocumento132 páginasAnnual Report 2015 EN 2 PDFQusai BassamAinda não há avaliações

- ChinaNet 2012 Investor PresentationDocumento74 páginasChinaNet 2012 Investor PresentationJosé ivan LópezAinda não há avaliações

- Vyaderm-Case Analysis 2006Documento4 páginasVyaderm-Case Analysis 2006Mridul SharmaAinda não há avaliações

- Interim Report q3 2023Documento26 páginasInterim Report q3 2023jvnshrAinda não há avaliações

- Write Your Answer For Part A HereDocumento9 páginasWrite Your Answer For Part A HereMATHEW JACOBAinda não há avaliações

- DATEDocumento10 páginasDATEbiancaftw90Ainda não há avaliações

- BCG InsideSherpa Core Strategy - Telco (Task 2 Additional Data) - UpdateDocumento9 páginasBCG InsideSherpa Core Strategy - Telco (Task 2 Additional Data) - UpdateAbinash AgrawalAinda não há avaliações

- Seagate 2Documento5 páginasSeagate 2Bruno Peña Jaramillo33% (3)

- Group Work Number 2Documento10 páginasGroup Work Number 2Enizel MontrondAinda não há avaliações

- Chapter 8Documento6 páginasChapter 8ديـنـا عادلAinda não há avaliações

- q2 Fy23 EarningsDocumento19 páginasq2 Fy23 EarningsGan ZhiHanAinda não há avaliações

- Case Study COS-Solved at ClassDocumento90 páginasCase Study COS-Solved at ClassMohsenAinda não há avaliações

- Chapter Fifteen SolutionsDocumento21 páginasChapter Fifteen Solutionsapi-3705855Ainda não há avaliações

- MeharVerma IMT CeresDocumento8 páginasMeharVerma IMT CeresMehar VermaAinda não há avaliações

- BCG Forage Core Strategy - Telco (Task 2 Additional Data) - UpdateDocumento10 páginasBCG Forage Core Strategy - Telco (Task 2 Additional Data) - UpdateHằng TừAinda não há avaliações

- BCG Forage Core Strategy - Telco (Task 2 Additional Data)Documento13 páginasBCG Forage Core Strategy - Telco (Task 2 Additional Data)Ramakrishna MaityAinda não há avaliações

- 2019 LBG q1 Ims CombinedDocumento19 páginas2019 LBG q1 Ims CombinedsaxobobAinda não há avaliações

- Interim Management StatementDocumento10 páginasInterim Management StatementsaxobobAinda não há avaliações

- IMT CeresDocumento5 páginasIMT CeresKAJAL SHARMAAinda não há avaliações

- 00388FS2021Documento96 páginas00388FS2021MUSE OMHAinda não há avaliações

- Test 2023Documento12 páginasTest 2023paingheinkhanttAinda não há avaliações

- Ceres Gardening Company Submission TemplateDocumento7 páginasCeres Gardening Company Submission Templatenikitapansare208Ainda não há avaliações

- Forecasting ProblemsDocumento7 páginasForecasting ProblemsJoel Pangisban0% (3)

- MeharVerma IMT Ceres 240110 163643Documento9 páginasMeharVerma IMT Ceres 240110 163643Mehar VermaAinda não há avaliações

- q3 Fy22 EarningsDocumento20 páginasq3 Fy22 EarningsMani packageAinda não há avaliações

- 2010 ArDocumento158 páginas2010 Ar叶芊Ainda não há avaliações

- CF MBA S23 Ch2 (B2) QsDocumento6 páginasCF MBA S23 Ch2 (B2) QsWaris 3478-FBAS/BSCS/F16Ainda não há avaliações

- q4 Fy21 EarningsDocumento19 páginasq4 Fy21 EarningsJoseph Adinolfi Jr.Ainda não há avaliações

- Annual Report of Nike PDFDocumento17 páginasAnnual Report of Nike PDFJeni FerAinda não há avaliações

- Steinberg Alexandra 4536 A3Documento136 páginasSteinberg Alexandra 4536 A3Yong RenAinda não há avaliações

- Cash Flow Ind AS 7Documento37 páginasCash Flow Ind AS 7Satish Kumar100% (1)

- Finance Marketing Term Courses Faculty: Pre Requisite OFD Term 4Documento2 páginasFinance Marketing Term Courses Faculty: Pre Requisite OFD Term 4Satish KumarAinda não há avaliações

- Micro16 Externalities 2016Documento53 páginasMicro16 Externalities 2016Satish KumarAinda não há avaliações

- Equity Derivatives Beginners Module PDFDocumento66 páginasEquity Derivatives Beginners Module PDFadityalal0% (4)

- Amit Behera DM19211 Ruksar Irshad Shaikh DM19240 Satish Kumar S DM19243 Shravani Sarma DM19247 Utkarsh Bhatnagar DM19254Documento3 páginasAmit Behera DM19211 Ruksar Irshad Shaikh DM19240 Satish Kumar S DM19243 Shravani Sarma DM19247 Utkarsh Bhatnagar DM19254Satish KumarAinda não há avaliações

- P&ID, An Insight Into Oil RefineryDocumento3 páginasP&ID, An Insight Into Oil RefinerySatish KumarAinda não há avaliações

- Static GK Theory FinalDocumento387 páginasStatic GK Theory FinalRahul NkAinda não há avaliações

- Laser CuttingDocumento13 páginasLaser CuttingSatish KumarAinda não há avaliações

- International Journal of Adhesion & Adhesives: Xiaocong HeDocumento8 páginasInternational Journal of Adhesion & Adhesives: Xiaocong HeSatish KumarAinda não há avaliações

- Privatize ThisDocumento220 páginasPrivatize Thisdonafutow2073Ainda não há avaliações

- Ma Assignment 2Documento7 páginasMa Assignment 2Osama YaqoobAinda não há avaliações

- Partnership DeedDocumento5 páginasPartnership DeedFarrukh SaleemAinda não há avaliações

- Tax Table Corporations 2022Documento4 páginasTax Table Corporations 2022Xandredg Sumpt LatogAinda não há avaliações

- Cape Mob Unit 1 IaDocumento11 páginasCape Mob Unit 1 IaShae Conner100% (1)

- Lbo Modeling Test Example: StreetofwallsDocumento18 páginasLbo Modeling Test Example: StreetofwallsLesterAinda não há avaliações

- Arsenal Football Club Annual Report 2009Documento58 páginasArsenal Football Club Annual Report 2009wcewong100% (1)

- Audit ProgramDocumento16 páginasAudit Programanon_806011137100% (4)

- Accounting and Finance Numericals Problems and AnsDocumento11 páginasAccounting and Finance Numericals Problems and AnsPramodh Kanulla0% (1)

- ACC210 SyllabusDocumento10 páginasACC210 SyllabusGrantham University0% (1)

- Sag Short Film Agreement Sample 2009Documento10 páginasSag Short Film Agreement Sample 2009kekepania176Ainda não há avaliações

- Marketing StrategiesDocumento63 páginasMarketing StrategiesChetan PahwaAinda não há avaliações

- Tally Ledger Groups List (Ledger Under Which Head or Group in Accounts PDFDocumento13 páginasTally Ledger Groups List (Ledger Under Which Head or Group in Accounts PDFravi100% (1)

- Monte BiancoDocumento10 páginasMonte BiancoJeanine Benjamin100% (4)

- BSBFIM601 Assessment 1 - Project - 2017 - No HeaddersDocumento8 páginasBSBFIM601 Assessment 1 - Project - 2017 - No Headdersnimisha chaturvediAinda não há avaliações

- NCCC Business PlanDocumento60 páginasNCCC Business PlanLuvsansharav Naranbaatar50% (2)

- Case Study Royal Bank of CanadaDocumento10 páginasCase Study Royal Bank of Canadandgharat100% (1)

- TaxationDocumento742 páginasTaxationSrinivasa Rao Bandlamudi83% (6)

- Amherst Schools Staff Salaries 2012Documento17 páginasAmherst Schools Staff Salaries 2012Larry KelleyAinda não há avaliações

- SNAP Program BrochureDocumento2 páginasSNAP Program BrochureSC AppleseedAinda não há avaliações

- Spring 2016 SUA Document No 1Documento6 páginasSpring 2016 SUA Document No 1Esther Dorce0% (2)

- FSA Assignment WMP10055Documento7 páginasFSA Assignment WMP10055Anshul VermaAinda não há avaliações

- Quiz Bee Problems Version 1Documento68 páginasQuiz Bee Problems Version 1Lalaine De JesusAinda não há avaliações

- Fesco Online BilllDocumento1 páginaFesco Online BilllNasir ArslanAinda não há avaliações

- Cost AccountingDocumento15 páginasCost AccountingADAinda não há avaliações

- Consolidation AccountingDocumento3 páginasConsolidation AccountingTauseef AbbasAinda não há avaliações

- 50 AAPL Buyside PitchbookDocumento22 páginas50 AAPL Buyside PitchbookZefi KtsiAinda não há avaliações

- Case Study KodakDocumento31 páginasCase Study KodakZineb Elouataoui100% (1)

- FRS 123 Borrowing Costs PDFDocumento4 páginasFRS 123 Borrowing Costs PDFRandy AsnorAinda não há avaliações

- AE 24 Lesson 2-3Documento4 páginasAE 24 Lesson 2-3Keahlyn BoticarioAinda não há avaliações