Você também pode gostar

- NoticeOfLiability To USA Agents Mrs. Alvarado PDFDocumento16 páginasNoticeOfLiability To USA Agents Mrs. Alvarado PDFMARSHA MAINESAinda não há avaliações

- Reassessing PresidencyDocumento830 páginasReassessing PresidencyIvan JanssensAinda não há avaliações

- United States Invasion of PanamaDocumento26 páginasUnited States Invasion of PanamaLidia CastroAinda não há avaliações

- Legal requirements for international marriageDocumento1 páginaLegal requirements for international marriagemaria fe moncadaAinda não há avaliações

- SpecPro - LEE vs. CA GR118387Documento3 páginasSpecPro - LEE vs. CA GR118387Niño CarbonillaAinda não há avaliações

- Intern Non-Disclosure Agreement: Article I: Scope of AgreementDocumento5 páginasIntern Non-Disclosure Agreement: Article I: Scope of Agreementfeel free userAinda não há avaliações

- Fiscal Policy and Government DebtDocumento14 páginasFiscal Policy and Government DebtNick GrzebienikAinda não há avaliações

- PEOPLE Vs DE GRANODocumento2 páginasPEOPLE Vs DE GRANOLoiseAinda não há avaliações

- Mankiw - 7e - Chapter 7Documento22 páginasMankiw - 7e - Chapter 7Gosaye DesalegnAinda não há avaliações

- CHAP19Documento35 páginasCHAP19veveng100% (1)

- RUBI v. Provincial BoardDocumento3 páginasRUBI v. Provincial BoardMaila Fortich RosalAinda não há avaliações

- Chapter No.18Documento11 páginasChapter No.18Kamal SinghAinda não há avaliações

- 11 Eastland Mfg. vs. Noriel - DIGDocumento2 páginas11 Eastland Mfg. vs. Noriel - DIGbananayellowsharpieAinda não há avaliações

- Mendirikan Kllinik BPJSDocumento9 páginasMendirikan Kllinik BPJSIstifa AmaliaAinda não há avaliações

- Kemiskinan Di BoyolaliDocumento15 páginasKemiskinan Di BoyolaliDede Firmansyah AlbanjaryAinda não há avaliações

- Self Made Data For HRMDocumento4 páginasSelf Made Data For HRMridaAinda não há avaliações

- Laporan Magang BI MalangDocumento49 páginasLaporan Magang BI MalangBlue NetAinda não há avaliações

- Budget and Fiscal Policy - EnglishDocumento12 páginasBudget and Fiscal Policy - EnglishMegha guptaAinda não há avaliações

- Pelanggaran HAM di PalestinaDocumento20 páginasPelanggaran HAM di PalestinarahzalursanAinda não há avaliações

- Analisis Investasi China Ke Indonesia Sebelum Dan Sesudah ACFTADocumento33 páginasAnalisis Investasi China Ke Indonesia Sebelum Dan Sesudah ACFTAaya_kubAinda não há avaliações

- EC204 Chapter 19 Business Cycle TheoriesDocumento32 páginasEC204 Chapter 19 Business Cycle Theoriesrajan20202000Ainda não há avaliações

- DEWI-Indonesia, ASEAN and Regional Stability CompressDocumento28 páginasDEWI-Indonesia, ASEAN and Regional Stability Compress-Ayu Mara Qonita-Ainda não há avaliações

- Kerjasama InternasionalDocumento7 páginasKerjasama InternasionalAmin No Hitori100% (1)

- Penafsiran Konstitusi - Tanto PDFDocumento19 páginasPenafsiran Konstitusi - Tanto PDFBGSTAinda não há avaliações

- Qualitative Research STAN September 2018Documento36 páginasQualitative Research STAN September 2018DesianaAinda não há avaliações

- The Dangers of Hustle Culture and the Importance of RestDocumento1 páginaThe Dangers of Hustle Culture and the Importance of RestAnirudh Kar 1912705Ainda não há avaliações

- Chap15 - Gov DebtDocumento34 páginasChap15 - Gov DebtChevalier ChevalierAinda não há avaliações

- Mankiw9e Lecture Slides Chap19 MCWDocumento40 páginasMankiw9e Lecture Slides Chap19 MCWrishunislam9Ainda não há avaliações

- Social Secuirty and The Federal BudgetDocumento14 páginasSocial Secuirty and The Federal BudgetOurFiscalSecurityAinda não há avaliações

- Gruberch 04Documento62 páginasGruberch 04Boy ColdAinda não há avaliações

- CH 16Documento34 páginasCH 16siwoerAinda não há avaliações

- Global Economics: PGP: Shekhar TomarDocumento38 páginasGlobal Economics: PGP: Shekhar TomarDivyang SaxenaAinda não há avaliações

- Topic 5Documento29 páginasTopic 5Sakshi VermaAinda não há avaliações

- Economic Modelling: Deficit Financing, National Debt and Ricardian EquivalenceDocumento15 páginasEconomic Modelling: Deficit Financing, National Debt and Ricardian EquivalencecbagriAinda não há avaliações

- chapter16_F2022Documento31 páginaschapter16_F2022ethanwuu03Ainda não há avaliações

- Working Paper 7 ADocumento144 páginasWorking Paper 7 Aziyad786123Ainda não há avaliações

- ArgentinecrisisDocumento16 páginasArgentinecrisisRuchit AndhariaAinda não há avaliações

- ICPAK PAYE PresentationDocumento13 páginasICPAK PAYE PresentationREJAY89Ainda não há avaliações

- Fiscal Policy Exercise-1Documento3 páginasFiscal Policy Exercise-1caden matthews100% (1)

- The First Step: A Progressive Plan For Meaningful Deficit Reduction by 2015Documento42 páginasThe First Step: A Progressive Plan For Meaningful Deficit Reduction by 2015Center for American ProgressAinda não há avaliações

- The National DebtDocumento13 páginasThe National DebtdeepfriedcatsAinda não há avaliações

- Lecture 13Documento35 páginasLecture 13Mohammad NurzamanAinda não há avaliações

- Global Markets Exam PrepDocumento14 páginasGlobal Markets Exam Prepbaler73561Ainda não há avaliações

- Chapter 34MP 13-14 2sDocumento6 páginasChapter 34MP 13-14 2sexcA1996Ainda não há avaliações

- Economics Handout Public Debt: The Debt Stock Net Budget DeficitDocumento6 páginasEconomics Handout Public Debt: The Debt Stock Net Budget DeficitOnella GrantAinda não há avaliações

- RSC FY2011 Budget ProposalDocumento34 páginasRSC FY2011 Budget ProposalRandall SmithAinda não há avaliações

- Chapter 11Documento9 páginasChapter 11Kotryna RudelytėAinda não há avaliações

- Cut Deficits by Cutting SpendingDocumento4 páginasCut Deficits by Cutting SpendingAdrià LópezAinda não há avaliações

- ECO3152 - CH 9 Equil and RE 2020fallDocumento51 páginasECO3152 - CH 9 Equil and RE 2020fallTeachers OnlineAinda não há avaliações

- Fiscal Policy and Government DebtDocumento25 páginasFiscal Policy and Government Debtapple21Ainda não há avaliações

- Econ Macro Canadian 1st Edition Mceachern Solutions ManualDocumento8 páginasEcon Macro Canadian 1st Edition Mceachern Solutions Manualkathleenjonesswzrqcmkex100% (13)

- Ebook Econ Macro Canadian 1St Edition Mceachern Solutions Manual Full Chapter PDFDocumento29 páginasEbook Econ Macro Canadian 1St Edition Mceachern Solutions Manual Full Chapter PDFhannhijhu100% (10)

- Public Sector Economy v4Documento79 páginasPublic Sector Economy v4M-userAinda não há avaliações

- America Turning Japanese? Global Debt Deflation & Manipulated Asset MarketsDocumento20 páginasAmerica Turning Japanese? Global Debt Deflation & Manipulated Asset Marketsaao5269Ainda não há avaliações

- Crowding in or Crowding Out?Documento26 páginasCrowding in or Crowding Out?Avik SarkarAinda não há avaliações

- Outlook Eng Focus Tcm43 132318Documento15 páginasOutlook Eng Focus Tcm43 132318vipulmajmudar1456Ainda não há avaliações

- Ugba 101b Test 2 2008Documento12 páginasUgba 101b Test 2 2008Minji KimAinda não há avaliações

- GM545 - Week 6 Homework Solutions V3Documento2 páginasGM545 - Week 6 Homework Solutions V3Deji LipedeAinda não há avaliações

- Inflation Isn't A Four Letter WordDocumento1 páginaInflation Isn't A Four Letter WordvanschaikAinda não há avaliações

- Macro Policy Debates: Active vs Passive, Rules vs Discretion, and Views on Government DebtDocumento41 páginasMacro Policy Debates: Active vs Passive, Rules vs Discretion, and Views on Government DebtJuny NhưAinda não há avaliações

- 2021 HSC EconomicsDocumento24 páginas2021 HSC EconomicspotpalAinda não há avaliações

- Budget Deficit: Some Facts and InformationDocumento4 páginasBudget Deficit: Some Facts and InformationSandhya GuptaAinda não há avaliações

- The Design of The Tax SystemDocumento42 páginasThe Design of The Tax SystemAnugerah BagusAinda não há avaliações

- Principles 2e Ch31Documento28 páginasPrinciples 2e Ch31AdityaAinda não há avaliações

- Debt ReductionDocumento3 páginasDebt ReductionmerluzzaAinda não há avaliações

- Refined PowerpointDocumento12 páginasRefined PowerpointAhmedAinda não há avaliações

- q4 Global Forecast ReportDocumento8 páginasq4 Global Forecast ReportElysia M. AbainAinda não há avaliações

- 1.2. Alphabet Soup The Shape of The COVID-19 Recession - Forbes AdvisorDocumento15 páginas1.2. Alphabet Soup The Shape of The COVID-19 Recession - Forbes AdvisorAbhinav UppalAinda não há avaliações

- WR CSP 21 NameList Engl 021121Documento325 páginasWR CSP 21 NameList Engl 021121Mohd BilalAinda não há avaliações

- Memorandum of Agreement Maam MonaDocumento2 páginasMemorandum of Agreement Maam MonaYamden OliverAinda não há avaliações

- Mohawk Case 2006-8 Katenies (Aka Janet Davis)Documento59 páginasMohawk Case 2006-8 Katenies (Aka Janet Davis)Truth Press MediaAinda não há avaliações

- An Essay On The Foreign Policy of IndiaDocumento2 páginasAn Essay On The Foreign Policy of IndiatintucrajuAinda não há avaliações

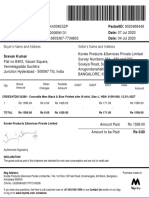

- Tax Invoice SummaryDocumento1 páginaTax Invoice SummaryDashing DealAinda não há avaliações

- Gstin Number: Packetid: 9020468448 Invoice Number: Date: 07 Jul 2020 Order Number: Date: 04 Jul 2020Documento1 páginaGstin Number: Packetid: 9020468448 Invoice Number: Date: 07 Jul 2020 Order Number: Date: 04 Jul 2020Sravan KumarAinda não há avaliações

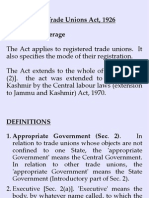

- Trade Unions ActDocumento35 páginasTrade Unions ActAnam AminAinda não há avaliações

- TYBCom Five Heads Theory 89 PgsDocumento90 páginasTYBCom Five Heads Theory 89 PgsPrabhu Gabriel0% (1)

- College of Criminology: Midterm Exam For Crim 6 BE HONEST... Good Luck... Ten (10) Points EachDocumento1 páginaCollege of Criminology: Midterm Exam For Crim 6 BE HONEST... Good Luck... Ten (10) Points EachAnitaManzanilloAinda não há avaliações

- Perfam Mendoza To LiyaoDocumento30 páginasPerfam Mendoza To Liyaoeugenebriones27yahoo.comAinda não há avaliações

- Public Corp Cases FulltextDocumento96 páginasPublic Corp Cases FulltextJose MasarateAinda não há avaliações

- Consti Case List Secs 6-22Documento26 páginasConsti Case List Secs 6-22Matthew WittAinda não há avaliações

- Po1 Recruitment Application Form: Cabannag Cherry Mae Licuben Taripan, Malibcong, Abra, Car 2820Documento1 páginaPo1 Recruitment Application Form: Cabannag Cherry Mae Licuben Taripan, Malibcong, Abra, Car 2820Angeline CabannagAinda não há avaliações

- Oracle Database 11g: Administration Workshop IDocumento2 páginasOracle Database 11g: Administration Workshop IFilipe Santos100% (1)

- Javellana V Lutero and RCA JaroDocumento4 páginasJavellana V Lutero and RCA JaroYet Barreda BasbasAinda não há avaliações

- GR 158896 Siayngco Vs Siayngco PIDocumento1 páginaGR 158896 Siayngco Vs Siayngco PIMichael JonesAinda não há avaliações

- P L D 2016 Lahore 587 - Releif Not Prayed For Cannot Be GrantedDocumento14 páginasP L D 2016 Lahore 587 - Releif Not Prayed For Cannot Be GrantedAhmad RazaAinda não há avaliações

- Company FNLDocumento30 páginasCompany FNLpriyaAinda não há avaliações

- Hamer v. SidwayDocumento3 páginasHamer v. SidwayAnonymous eJBhs9CgAinda não há avaliações

- Alcantara V RepublicDocumento15 páginasAlcantara V RepublicEzer SccatsAinda não há avaliações

- Not PrecedentialDocumento9 páginasNot PrecedentialScribd Government DocsAinda não há avaliações

- Kuratko 8 Ech 07Documento20 páginasKuratko 8 Ech 07Jawwad HussainAinda não há avaliações