Você também pode gostar

- C13 Gitman Leverage and CapitalDocumento53 páginasC13 Gitman Leverage and CapitalPhước Nguyễn100% (1)

- CHAPTER 1: Resource Utilization & Economics Part I: Identification Directions: Fill in The BlanksDocumento28 páginasCHAPTER 1: Resource Utilization & Economics Part I: Identification Directions: Fill in The BlanksAngelo Montelibano Patron100% (4)

- Cornchopper Company BreakEven SolutionDocumento2 páginasCornchopper Company BreakEven Solutionakshay_kapAinda não há avaliações

- Bronze Adora Case StudyDocumento8 páginasBronze Adora Case StudyTitiAinda não há avaliações

- Chapter 8 ProfitabilityDocumento90 páginasChapter 8 ProfitabilityAudra Joy San JuanAinda não há avaliações

- Ratios and InterpretationDocumento6 páginasRatios and Interpretationjohngay1987Ainda não há avaliações

- Ap 1 Primary Financial Statements October 2023 EegDocumento54 páginasAp 1 Primary Financial Statements October 2023 EegOyeleye TofunmiAinda não há avaliações

- (Valix) EpsDocumento58 páginas(Valix) EpsMaeAinda não há avaliações

- Analysis of Financial StatementsDocumento77 páginasAnalysis of Financial StatementsGandharv ChopraAinda não há avaliações

- Analyzing and Interpreting Financial StatementsDocumento42 páginasAnalyzing and Interpreting Financial StatementsLiluAinda não há avaliações

- 21decentralized Operations and Segment ReportingDocumento142 páginas21decentralized Operations and Segment ReportingyejiAinda não há avaliações

- Income STDocumento23 páginasIncome STKholoud LabadyAinda não há avaliações

- Mgtp04 - Prelim ReviewerDocumento6 páginasMgtp04 - Prelim ReviewerAngel Rose CoralesAinda não há avaliações

- Presentation 5 Chapter 6Documento33 páginasPresentation 5 Chapter 6Mia MohsinAinda não há avaliações

- Three Basic Accounting Statements:: - Income StatementDocumento14 páginasThree Basic Accounting Statements:: - Income Statementamedina8131Ainda não há avaliações

- 28 Diff Bet Usgaap Igaap IfrsDocumento7 páginas28 Diff Bet Usgaap Igaap IfrsRohit BeniwalAinda não há avaliações

- Chapter 5 Review Questions and ProblemsDocumento11 páginasChapter 5 Review Questions and ProblemsLars FriasAinda não há avaliações

- Minggu 12 - BAB 12 - Kelompok 1Documento25 páginasMinggu 12 - BAB 12 - Kelompok 1rifaAinda não há avaliações

- AC16 601A HONSON Comparing Financial Statements of The GovernmentDocumento8 páginasAC16 601A HONSON Comparing Financial Statements of The GovernmentAlyssa Mae HonsonAinda não há avaliações

- Acknowledgments: 80 Sme Mining Engineering HandbookDocumento1 páginaAcknowledgments: 80 Sme Mining Engineering HandbookYeimsAinda não há avaliações

- Chapter 2 Concept 16 To 22Documento7 páginasChapter 2 Concept 16 To 22sundaram MishraAinda não há avaliações

- Managerial Accounting 16th Ed Textbook Solutions Manual Chapter 15Documento51 páginasManagerial Accounting 16th Ed Textbook Solutions Manual Chapter 15car itselfAinda não há avaliações

- Earnings Per ShareDocumento2 páginasEarnings Per SharerobinsonsgAinda não há avaliações

- Noer Rachmadhani H - 1810523011 - Week 10 AssignmentDocumento9 páginasNoer Rachmadhani H - 1810523011 - Week 10 AssignmentSajakul SornAinda não há avaliações

- Materi Kel 1 FATDocumento30 páginasMateri Kel 1 FATFawwazAinda não há avaliações

- Financial Mix RatiosDocumento7 páginasFinancial Mix RatiosansanandresAinda não há avaliações

- What Are Revenue Receipts and Capital Receipts - Tax2winDocumento14 páginasWhat Are Revenue Receipts and Capital Receipts - Tax2winKapil SharmaAinda não há avaliações

- Analysis of IFRSDocumento50 páginasAnalysis of IFRSjanckercfAinda não há avaliações

- Dwnload Full Corporate Finance A Focused Approach 5th Edition Ehrhardt Solutions Manual PDFDocumento36 páginasDwnload Full Corporate Finance A Focused Approach 5th Edition Ehrhardt Solutions Manual PDFmiltongoodwin2490i100% (15)

- Full Download Corporate Finance A Focused Approach 5th Edition Ehrhardt Solutions ManualDocumento36 páginasFull Download Corporate Finance A Focused Approach 5th Edition Ehrhardt Solutions Manualkisslingcicelypro100% (35)

- Is Your Private Company Return On Investment Adequate-How To Correctly Measure Adn Significantly Improve ROI - Long VersionDocumento12 páginasIs Your Private Company Return On Investment Adequate-How To Correctly Measure Adn Significantly Improve ROI - Long Versionsakron100% (1)

- IRFS Notes Part 4Documento31 páginasIRFS Notes Part 4Deandre DreyerAinda não há avaliações

- FA - Whitepaper - 2015 (1) 2Documento13 páginasFA - Whitepaper - 2015 (1) 2BAlmohsinAinda não há avaliações

- Internal AnalysisDocumento80 páginasInternal AnalysisAditi ShriyaAinda não há avaliações

- Financial Statement Analysis An Introduction: Fabricio Chala, CFA, FRMDocumento45 páginasFinancial Statement Analysis An Introduction: Fabricio Chala, CFA, FRMJhonatan Perez VillanuevaAinda não há avaliações

- 05 Econ 118 Profitability and Financial FlexibilityDocumento20 páginas05 Econ 118 Profitability and Financial FlexibilityPaul KimAinda não há avaliações

- EDHEC - MSC Fin - FAA - Overview of The Income StatementDocumento27 páginasEDHEC - MSC Fin - FAA - Overview of The Income StatementGabriele GabrieliAinda não há avaliações

- ACCT 102 Lecture Notes Chapter 13 SPR 2018Documento5 páginasACCT 102 Lecture Notes Chapter 13 SPR 2018Sophia Varias CruzAinda não há avaliações

- Interpretation of Financial StatementsDocumento26 páginasInterpretation of Financial StatementsPresident Musuki100% (1)

- Determinants of Dividends Policy and Dividend Policy of Companies Trend and Ratio AnalysisDocumento31 páginasDeterminants of Dividends Policy and Dividend Policy of Companies Trend and Ratio Analysissonal jainAinda não há avaliações

- Finman ReviewerDocumento8 páginasFinman ReviewerRafael BensigAinda não há avaliações

- IAChap004PPT - AmendedDocumento54 páginasIAChap004PPT - AmendedAseel Al NajraniAinda não há avaliações

- PFRS 8Documento2 páginasPFRS 8Ella MaeAinda não há avaliações

- Shareholder Value & Global Reporting. Reconciliation of Indian GAAP Financial Statements With US/International GAAPSDocumento15 páginasShareholder Value & Global Reporting. Reconciliation of Indian GAAP Financial Statements With US/International GAAPSvdforeAinda não há avaliações

- Usgaap, Igaap & IfrsDocumento7 páginasUsgaap, Igaap & IfrsdhangarsachinAinda não há avaliações

- Chapter 3Documento32 páginasChapter 3Abd El-Rahman El-syeoufyAinda não há avaliações

- Importance of Financial StatementDocumento11 páginasImportance of Financial StatementJAY SHUKLAAinda não há avaliações

- Prudential PLC Ar 2020Documento404 páginasPrudential PLC Ar 2020Lim KaixianAinda não há avaliações

- How To Read Balance SheetDocumento28 páginasHow To Read Balance SheetAnupam JyotiAinda não há avaliações

- Pfs Project WebinarDocumento31 páginasPfs Project WebinarNeji HergliAinda não há avaliações

- Ratio Analysis Notes: Liquidity RatiosDocumento7 páginasRatio Analysis Notes: Liquidity RatiosShaigari VenkateshAinda não há avaliações

- RatiosDocumento3 páginasRatiosFaridul TayyibahAinda não há avaliações

- Public Utility Entity Is Not Allowed To Use The Pfrs For Smes in The Philippines)Documento6 páginasPublic Utility Entity Is Not Allowed To Use The Pfrs For Smes in The Philippines)Glen JavellanaAinda não há avaliações

- SCOPE OF IAS 33 Earnings Per ShareDocumento16 páginasSCOPE OF IAS 33 Earnings Per Sharearrowphoto8161343rejelynAinda não há avaliações

- Chapter#3 Fianacial Statement and Ratio Analysis - Whole ChapterDocumento103 páginasChapter#3 Fianacial Statement and Ratio Analysis - Whole ChapterAhmed Abir ChoudhuryAinda não há avaliações

- Accounting in A Nutshell 7: Financial Ratios and AnalysisDocumento3 páginasAccounting in A Nutshell 7: Financial Ratios and AnalysisBusiness Expert PressAinda não há avaliações

- Final Version Group 4-Mid Course Group AssignmentDocumento22 páginasFinal Version Group 4-Mid Course Group AssignmentDiane MoutranAinda não há avaliações

- Pertemuan 9BDocumento36 páginasPertemuan 9Bleny aisyahAinda não há avaliações

- Operating Segment: Pfrs 8Documento28 páginasOperating Segment: Pfrs 8Giellay OyaoAinda não há avaliações

- Afm 1Documento20 páginasAfm 1antrikshaagrawalAinda não há avaliações

- Business FormulaeDocumento16 páginasBusiness Formulae12345JONESAinda não há avaliações

- Introduction To Nike:: University of Oregon Phil Knight Bill Bower Man Tiger AsicsDocumento3 páginasIntroduction To Nike:: University of Oregon Phil Knight Bill Bower Man Tiger AsicsHafsah Khan100% (1)

- Colombia Report Resubmit.Documento8 páginasColombia Report Resubmit.Hafsah KhanAinda não há avaliações

- Country Analysis BrazilDocumento32 páginasCountry Analysis BrazilHafsah KhanAinda não há avaliações

- Country Analysis TurkeyDocumento28 páginasCountry Analysis TurkeyHafsah KhanAinda não há avaliações

- Some Facts About PractoDocumento2 páginasSome Facts About PractoinfoAinda não há avaliações

- Dos and Donts For ITRV (Efiling Acknowledgement Form)Documento2 páginasDos and Donts For ITRV (Efiling Acknowledgement Form)bh_mehta_06Ainda não há avaliações

- International Economics FinalDocumento2 páginasInternational Economics FinalMain Uddin OrionAinda não há avaliações

- Departmental Exams Himachal PradeshDocumento2 páginasDepartmental Exams Himachal PradeshmadhaniasureshAinda não há avaliações

- BVPS and Eps Exercises PDFDocumento9 páginasBVPS and Eps Exercises PDFKyla Valencia NgoAinda não há avaliações

- Maersk GlossaryDocumento28 páginasMaersk GlossaryPrashant BhardwajAinda não há avaliações

- Ratio Analysis - BBA ClassDocumento27 páginasRatio Analysis - BBA ClassSophiya PrabinAinda não há avaliações

- BDM of 12.10.2015 - Buyback Program, Sell Up and PayoutDocumento5 páginasBDM of 12.10.2015 - Buyback Program, Sell Up and PayoutBVMF_RIAinda não há avaliações

- Lead - 2012 - Preparation of Liquidation and Distribution AccountsDocumento5 páginasLead - 2012 - Preparation of Liquidation and Distribution AccountsMpho MalemeAinda não há avaliações

- Microns20 DraftDocumento294 páginasMicrons20 DraftadhavvikasAinda não há avaliações

- Infosys - Q4FY22 - Result Update - Investor ReportDocumento10 páginasInfosys - Q4FY22 - Result Update - Investor ReportSavil GuptaAinda não há avaliações

- Diagnostic Exercises2Documento32 páginasDiagnostic Exercises2HanaAinda não há avaliações

- Comparative Study of Loan SchemesDocumento48 páginasComparative Study of Loan Schemessumesh8940% (1)

- Cost Behavior and Cost-Volume-Profit Analysis: Opening CommentsDocumento16 páginasCost Behavior and Cost-Volume-Profit Analysis: Opening CommentsNnickyle LaboresAinda não há avaliações

- Ecomom Post MortemDocumento7 páginasEcomom Post Mortemashontell67% (3)

- Soal UsDocumento2 páginasSoal UsAreb SubandiAinda não há avaliações

- Scholarship Application 2024 1Documento3 páginasScholarship Application 2024 1Abeera KhanAinda não há avaliações

- Financial Management: I. Concept NotesDocumento6 páginasFinancial Management: I. Concept NotesDanica Christele AlfaroAinda não há avaliações

- ACC202 Principles of Managerial AccountingDocumento14 páginasACC202 Principles of Managerial AccountingG JhaAinda não há avaliações

- Unit 4Documento112 páginasUnit 4Vetri Velan100% (1)

- Cost Accounting RefresherDocumento16 páginasCost Accounting RefresherDemi PardilloAinda não há avaliações

- Moduel 4 Financial Statement Modeling Theory and ConceptsDocumento26 páginasModuel 4 Financial Statement Modeling Theory and ConceptsAkshay Krishnan P RCBSAinda não há avaliações

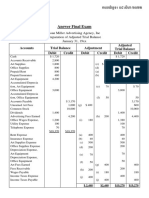

- Answer Final Exam (POA)Documento2 páginasAnswer Final Exam (POA)Phâk Tèr ÑgAinda não há avaliações

- Chapter 1: IntroductionDocumento48 páginasChapter 1: IntroductionnemchandAinda não há avaliações

- AppendixDocumento30 páginasAppendixLeigh Arrel DivinoAinda não há avaliações

- Do It! 2: Accounting Principles (1) First GradeDocumento4 páginasDo It! 2: Accounting Principles (1) First GradeAmer Wagdy GergesAinda não há avaliações

- Internal vs. External SWOT TemplateDocumento6 páginasInternal vs. External SWOT TemplateGirish Ranjan MishraAinda não há avaliações