Você também pode gostar

- Business Ethics Concepts & Cases: Manuel G. VelasquezDocumento21 páginasBusiness Ethics Concepts & Cases: Manuel G. VelasquezFariza SiswantiAinda não há avaliações

- Deteksi Financial Statement Fraud Penguj A32b077bDocumento12 páginasDeteksi Financial Statement Fraud Penguj A32b077bdaniel marselinusAinda não há avaliações

- AUDITING 1 Tuanakotta Chapter 15-30Documento33 páginasAUDITING 1 Tuanakotta Chapter 15-30daniel marselinusAinda não há avaliações

- B1C212023 - Sitedi - JURNAL Kurniawan Kahar B1C2 12 023Documento15 páginasB1C212023 - Sitedi - JURNAL Kurniawan Kahar B1C2 12 023titin gusmayantuAinda não há avaliações

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (399)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (265)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (119)

- Volatility Index75 RISK AND MONEY MANAGEMENT-UPDATEDDocumento12 páginasVolatility Index75 RISK AND MONEY MANAGEMENT-UPDATEDJoseph Chukwu100% (1)

- Safe Shop Plan - 2022 JuneDocumento40 páginasSafe Shop Plan - 2022 Juneshinu pokemon masterAinda não há avaliações

- Documentos Comerciales en InglesDocumento46 páginasDocumentos Comerciales en InglesMiguel100% (3)

- Inflation: Its Causes, Effects, and Social Costs: MacroeconomicsDocumento61 páginasInflation: Its Causes, Effects, and Social Costs: MacroeconomicsTai612Ainda não há avaliações

- State Finances in Haryana - Manju DalalDocumento26 páginasState Finances in Haryana - Manju Dalalvoldemort1989Ainda não há avaliações

- Asset Partner Opportunity OverviewDocumento1 páginaAsset Partner Opportunity OverviewkaranAinda não há avaliações

- Taxes On Savings: Jonathan Gruber Public Finance and Public PolicyDocumento51 páginasTaxes On Savings: Jonathan Gruber Public Finance and Public PolicyGaluh WicaksanaAinda não há avaliações

- Backlog 202021 VoucherDocumento1 páginaBacklog 202021 VoucherYousufAinda não há avaliações

- BootcampX Day 6Documento15 páginasBootcampX Day 6Vivek LasunaAinda não há avaliações

- RBS Holdings N.V. Annual Report and Accounts 2011Documento256 páginasRBS Holdings N.V. Annual Report and Accounts 2011Iskandar IsAinda não há avaliações

- BPO Frequently Asked Questions Corporates May2018 FinalDocumento10 páginasBPO Frequently Asked Questions Corporates May2018 FinalMuthu SelvanAinda não há avaliações

- RA 7906 (Thrift Banks)Documento17 páginasRA 7906 (Thrift Banks)Jerwin DaveAinda não há avaliações

- Effect of Budgetary Control On Financial Performance of Savings and Credit Cooperative Organizations in Nairobi CountyDocumento21 páginasEffect of Budgetary Control On Financial Performance of Savings and Credit Cooperative Organizations in Nairobi CountyNATASHA ATHIRA BINTI RUSLI UPMAinda não há avaliações

- ThesisDocumento17 páginasThesisKritiAinda não há avaliações

- Salam & Parallel Salam Transactions-CH.7Documento36 páginasSalam & Parallel Salam Transactions-CH.7Yusuf Hussein0% (1)

- NSE Yield Curve and Implied Yields ReportDocumento2 páginasNSE Yield Curve and Implied Yields ReportCarl RossAinda não há avaliações

- NoteDocumento3 páginasNotePriya GoyalAinda não há avaliações

- Study online at quizlet.com/_23q1qiDocumento2 páginasStudy online at quizlet.com/_23q1qiAPRATIM BHUIYANAinda não há avaliações

- Week 3 Tutorial SolutionsDocumento31 páginasWeek 3 Tutorial SolutionsalexandraAinda não há avaliações

- Micro Financing HistoryDocumento62 páginasMicro Financing HistoryVincent KonoteyAinda não há avaliações

- Project Report On Mutual Fund Schemes of SBIDocumento43 páginasProject Report On Mutual Fund Schemes of SBIRonak Jain100% (2)

- Acctg Lab 7Documento8 páginasAcctg Lab 7AngieAinda não há avaliações

- Cambridge Assessment International Education: Accounting 0452/22 October/November 2017Documento12 páginasCambridge Assessment International Education: Accounting 0452/22 October/November 2017pyaaraasingh716Ainda não há avaliações

- Economics (Simple and Compound Interest#2)Documento17 páginasEconomics (Simple and Compound Interest#2)api-2636776733% (3)

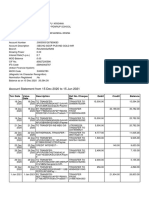

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocumento4 páginasStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalancePrince BharvadAinda não há avaliações

- Vethathiri - WisdomDocumento40 páginasVethathiri - WisdomProf. Madhavan100% (2)

- New NabilDocumento30 páginasNew NabilMadhurendra SinghAinda não há avaliações

- Topic 2 - Business CombinationsDocumento32 páginasTopic 2 - Business Combinationshayat_illusionAinda não há avaliações

- ACF Project ReportDocumento17 páginasACF Project Reportpranita mundraAinda não há avaliações

- Account statement for Mr. SAVARAPU KRISHNA from Dec 2020 to Jun 2021Documento9 páginasAccount statement for Mr. SAVARAPU KRISHNA from Dec 2020 to Jun 2021SRINIVASARAO JONNALAAinda não há avaliações