Você também pode gostar

- Corporate Finance Formulas: A Simple IntroductionNo EverandCorporate Finance Formulas: A Simple IntroductionNota: 4 de 5 estrelas4/5 (8)

- MATLAB TutorialDocumento182 páginasMATLAB Tutorialxfreshtodef123Ainda não há avaliações

- Lecture 2 HvacDocumento38 páginasLecture 2 HvacJohn BennettAinda não há avaliações

- Performance Prediction and Analytics of Fuzzy, Reliability and Queuing Models Theory and Applications by Kusum Deep, Madhu Jain, Said Salhi PDFDocumento282 páginasPerformance Prediction and Analytics of Fuzzy, Reliability and Queuing Models Theory and Applications by Kusum Deep, Madhu Jain, Said Salhi PDFSazzadAinda não há avaliações

- Ch. 2. Asset Pricing Theory (721383S) : Juha Joenväärä University of Oulu March 2014Documento31 páginasCh. 2. Asset Pricing Theory (721383S) : Juha Joenväärä University of Oulu March 2014Asma DahmenAinda não há avaliações

- CH 5 MARKET RISK - VaRDocumento29 páginasCH 5 MARKET RISK - VaRAisyah Vira AmandaAinda não há avaliações

- Financial Markets 1 What Financial Markets Do: 2.1 One Riskless and One Risky AssetDocumento18 páginasFinancial Markets 1 What Financial Markets Do: 2.1 One Riskless and One Risky AssetArmanbekAlkinAinda não há avaliações

- Basic Utility Theory For Portfolio SelectionDocumento25 páginasBasic Utility Theory For Portfolio SelectionTecwyn LimAinda não há avaliações

- Utility and Risk AversionDocumento22 páginasUtility and Risk AversionMihai StoicaAinda não há avaliações

- Lecture 1: Risk and Risk AversionDocumento15 páginasLecture 1: Risk and Risk AversionDavide Paccia BattistiniAinda não há avaliações

- Introduction To Portfolio Selection and Capital Market Theory: Static AnalysisDocumento97 páginasIntroduction To Portfolio Selection and Capital Market Theory: Static AnalysisAkshay TyagiAinda não há avaliações

- Optimal InsuranceDocumento14 páginasOptimal InsuranceNavya KhandelwalAinda não há avaliações

- Decision Making Under Uncertainty Expected UtilityDocumento37 páginasDecision Making Under Uncertainty Expected Utilityckv1987Ainda não há avaliações

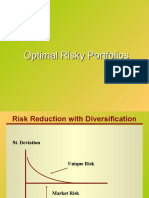

- Risk Reduction with DiversificationDocumento23 páginasRisk Reduction with DiversificationJay GuptaAinda não há avaliações

- The Value at Risk: Andreas de VriesDocumento10 páginasThe Value at Risk: Andreas de VriesJesús Alcalá GarcíaAinda não há avaliações

- Lecture 3 Risk Aversion and Capital Allocation - Optimal Risky PortfolioDocumento66 páginasLecture 3 Risk Aversion and Capital Allocation - Optimal Risky Portfolionoobmaster 0206Ainda não há avaliações

- FINM7008 Applied Investments: Week 3 Capital Allocation and Optimal Risky PortfoliosDocumento24 páginasFINM7008 Applied Investments: Week 3 Capital Allocation and Optimal Risky PortfoliosNatalie OngAinda não há avaliações

- Portfolio Risk and Utility FunctionsDocumento72 páginasPortfolio Risk and Utility FunctionsJohnThomasAinda não há avaliações

- Attitude Towards RiskDocumento11 páginasAttitude Towards RiskOrestis :. KonstantinidisAinda não há avaliações

- Lecture 4 Risk Aversion and Capital Allocation To Risky AssetsDocumento20 páginasLecture 4 Risk Aversion and Capital Allocation To Risky AssetsLuisLoAinda não há avaliações

- Lecture 4 Optimal Risky PortfoliosDocumento66 páginasLecture 4 Optimal Risky Portfoliosi YuerukiAinda não há avaliações

- Optimal Portfolios and The Mutual Fund Separation Theorem: I 1 2 N IjDocumento3 páginasOptimal Portfolios and The Mutual Fund Separation Theorem: I 1 2 N IjMachaca Alvaro MamaniAinda não há avaliações

- API 111 Solutions 7Documento8 páginasAPI 111 Solutions 76doitAinda não há avaliações

- AssetAlloc and RiskManagementDocumento16 páginasAssetAlloc and RiskManagementNeel KanakAinda não há avaliações

- 6 Modern Portfolio TheoryDocumento78 páginas6 Modern Portfolio Theorysupeng huangAinda não há avaliações

- Expected Utility OptimizationDocumento73 páginasExpected Utility OptimizationL SAinda não há avaliações

- Risk-Bearing in A Winner-Take-All ContestDocumento18 páginasRisk-Bearing in A Winner-Take-All ContestDRAinda não há avaliações

- Chapter-10 Return & RiskDocumento19 páginasChapter-10 Return & Riskaparajita promaAinda não há avaliações

- SAPM - Optimal Risky Portfolio - DistributionDocumento24 páginasSAPM - Optimal Risky Portfolio - DistributionShubham AgrawalAinda não há avaliações

- Learning Module 3: Optimal Asset Allocation: Portfolio ManagementDocumento30 páginasLearning Module 3: Optimal Asset Allocation: Portfolio ManagementYaonik HimmatramkaAinda não há avaliações

- Money, Banking & Finance: Risk, Return and Portfolio TheoryDocumento39 páginasMoney, Banking & Finance: Risk, Return and Portfolio TheorysarahjohnsonAinda não há avaliações

- Economics 302Documento13 páginasEconomics 302Rana AhmedAinda não há avaliações

- Finance ReviewDocumento18 páginasFinance ReviewZahidul IslamAinda não há avaliações

- Asset Pricing ModelDocumento62 páginasAsset Pricing ModelA. LatifAinda não há avaliações

- Portfolio QuestionsDocumento6 páginasPortfolio QuestionsHarsh RajAinda não há avaliações

- FIB3005Documento10 páginasFIB3005Nga nguyen thiAinda não há avaliações

- Introduction To Risk Premium and Markowitz-BBDocumento22 páginasIntroduction To Risk Premium and Markowitz-BBCarla SolerAinda não há avaliações

- The Tools of Portfolio AnalysisDocumento12 páginasThe Tools of Portfolio AnalysisTheYellowKingAinda não há avaliações

- Ch03-5 Portifolio Theory - Risk Return AnalysisDocumento113 páginasCh03-5 Portifolio Theory - Risk Return AnalysismupiwamasimbaAinda não há avaliações

- Econometrics 1 Slide5Documento29 páginasEconometrics 1 Slide5yingdong liuAinda não há avaliações

- Lecture 1.3: Risk-Return Characteristics of Securities: Investment Analysis Fall, 2012Documento24 páginasLecture 1.3: Risk-Return Characteristics of Securities: Investment Analysis Fall, 2012Hugo PagolaAinda não há avaliações

- Financial Decision-Making Under UncertaintyDocumento18 páginasFinancial Decision-Making Under UncertaintyMateo PulidoAinda não há avaliações

- General Theory Economics of Risk and Time: Toulouse School of Economics Catherine Bobtcheff Catherine - Bobtcheff@tse-Fr - EuDocumento49 páginasGeneral Theory Economics of Risk and Time: Toulouse School of Economics Catherine Bobtcheff Catherine - Bobtcheff@tse-Fr - EuTrúc LinhAinda não há avaliações

- Capital Allocation Between The Risky and The Risk-Free AssetDocumento32 páginasCapital Allocation Between The Risky and The Risk-Free AssetanushreegoAinda não há avaliações

- Chapter1 Measuing Risk and ReturnDocumento29 páginasChapter1 Measuing Risk and Returneya feguiriAinda não há avaliações

- CH 13Documento55 páginasCH 13Atif AslamAinda não há avaliações

- Bas430 FPD 2 2021 2 PDFDocumento121 páginasBas430 FPD 2 2021 2 PDFNkhandu S M WilliamsAinda não há avaliações

- CHOICEDocumento9 páginasCHOICEtegegn mogessieAinda não há avaliações

- Capital Allocation Across RiskyDocumento23 páginasCapital Allocation Across RiskyVaidyanathan RavichandranAinda não há avaliações

- Optimal Risky Portfolio (Bodie) PDFDocumento20 páginasOptimal Risky Portfolio (Bodie) PDFjoel_kifAinda não há avaliações

- Risk, Return and Cost of CapitalDocumento9 páginasRisk, Return and Cost of CapitalQuoc Viet DuongAinda não há avaliações

- Mean-Variance Analysis and the CAPM ExplainedDocumento20 páginasMean-Variance Analysis and the CAPM ExplainedAlexandra MiroiuAinda não há avaliações

- Chapter 5 Utility FunctionDocumento32 páginasChapter 5 Utility FunctionNermine LimemeAinda não há avaliações

- Arrow Pratt BBDocumento15 páginasArrow Pratt BBCarla SolerAinda não há avaliações

- Mean-Variance Optimization and the CAPM: A 38-Character IntroductionDocumento7 páginasMean-Variance Optimization and the CAPM: A 38-Character Introductionmazin903Ainda não há avaliações

- MATH4512 - Fundamentals of Mathematical FinanceDocumento127 páginasMATH4512 - Fundamentals of Mathematical FinanceustmathjjAinda não há avaliações

- Portfolio ReturnDocumento23 páginasPortfolio ReturnAbhishek ChahalAinda não há avaliações

- Chapter11 Stock Valuation and RiskDocumento39 páginasChapter11 Stock Valuation and RiskprojectonamlonAinda não há avaliações

- Chapter 7Documento7 páginasChapter 7bobby brownAinda não há avaliações

- Ec2723 Assignment 4 Review QuestionsDocumento5 páginasEc2723 Assignment 4 Review Questions6doitAinda não há avaliações

- Capstone FinalDocumento66 páginasCapstone FinalNisha RaniAinda não há avaliações

- A 19Documento28 páginasA 19Nisha RaniAinda não há avaliações

- Debt MarketDocumento46 páginasDebt MarketNisha Rani100% (1)

- Ansal Housing and Construction LTDDocumento5 páginasAnsal Housing and Construction LTDNisha RaniAinda não há avaliações

- Dependability 3 UnlockedDocumento26 páginasDependability 3 UnlockedAngelBlancoPomaAinda não há avaliações

- Joint Tutorial Analyzes Circular Opening Near WeaknessDocumento12 páginasJoint Tutorial Analyzes Circular Opening Near WeaknessTeofilo Augusto Huaranccay HuamaniAinda não há avaliações

- Unit2 PFMHDocumento281 páginasUnit2 PFMHLihas AirohalAinda não há avaliações

- Humphreys.-The Material Balance Equation For A Gas Condensate Reservoir With Significant Water VaporizationDocumento8 páginasHumphreys.-The Material Balance Equation For A Gas Condensate Reservoir With Significant Water VaporizationSergio FloresAinda não há avaliações

- Quantitative Aptitude PDFDocumento35 páginasQuantitative Aptitude PDFjeevithaAinda não há avaliações

- Symmetry in Art and ArchitectureDocumento59 páginasSymmetry in Art and ArchitectureIIRemmyIIAinda não há avaliações

- Chemical Physics: Manish Chopra, Niharendu ChoudhuryDocumento11 páginasChemical Physics: Manish Chopra, Niharendu ChoudhuryasdikaAinda não há avaliações

- GIRO - Global Ionospheric Radio ObservatoryDocumento20 páginasGIRO - Global Ionospheric Radio ObservatoryVincent J. CataldiAinda não há avaliações

- Report CVP AnalysisDocumento25 páginasReport CVP AnalysisSaief Dip100% (1)

- MATH 1003 Calculus and Linear Algebra (Lecture 2) : Albert KuDocumento17 páginasMATH 1003 Calculus and Linear Algebra (Lecture 2) : Albert Kuandy15Ainda não há avaliações

- Ch23 (Young-Freedman) Parte 2Documento19 páginasCh23 (Young-Freedman) Parte 2JorgeCortezAinda não há avaliações

- 1.1 Gauss's LawDocumento14 páginas1.1 Gauss's LawSatya ReddyAinda não há avaliações

- UR Script ManualDocumento102 páginasUR Script ManualAlexandru BourAinda não há avaliações

- 2016 CodeUGM Usingn Code Design Life For Fatigue of WeldsDocumento32 páginas2016 CodeUGM Usingn Code Design Life For Fatigue of WeldsdddAinda não há avaliações

- AverageDocumento4 páginasAveragerauf tabassumAinda não há avaliações

- Business Math CBLM Com MathDocumento54 páginasBusiness Math CBLM Com MathJoy CelestialAinda não há avaliações

- Ripple Carry and Carry Lookahead Addition and Subtraction CircuitsDocumento19 páginasRipple Carry and Carry Lookahead Addition and Subtraction CircuitsSurya KanthAinda não há avaliações

- SPC For Non-Normal DataDocumento4 páginasSPC For Non-Normal DataEdAinda não há avaliações

- SAP2000 Demo 2013 PDFDocumento24 páginasSAP2000 Demo 2013 PDFLi Yin Ting TerryAinda não há avaliações

- Naming Angle Pairs 1Documento3 páginasNaming Angle Pairs 1ann dumadagAinda não há avaliações

- Cs8792-Cryptography and Network Security Unit-3: Sn. No. Option 1 Option 2 Option 3 Option 4 Correct OptionDocumento3 páginasCs8792-Cryptography and Network Security Unit-3: Sn. No. Option 1 Option 2 Option 3 Option 4 Correct Optionabrar nahinAinda não há avaliações

- Non Linear Data StructuresDocumento50 páginasNon Linear Data Structuresnaaz_pinuAinda não há avaliações

- CAPM - An Absured ModelDocumento17 páginasCAPM - An Absured ModelanalysesAinda não há avaliações

- Aluminium 2014 t6 2014 t651 PDFDocumento3 páginasAluminium 2014 t6 2014 t651 PDFAbhishek AnandAinda não há avaliações

- Fluid Mechanics Summary Notes PDFDocumento322 páginasFluid Mechanics Summary Notes PDFLendo PosaraAinda não há avaliações

- Signal-Flow Graphs & Mason's RuleDocumento18 páginasSignal-Flow Graphs & Mason's RuleRemuel ArellanoAinda não há avaliações

- Strength of Materials Lab Report on Helical Spring TestingDocumento7 páginasStrength of Materials Lab Report on Helical Spring TestingG. Dancer GhAinda não há avaliações