Você também pode gostar

- Working Capital Management (2015)Documento62 páginasWorking Capital Management (2015)AJAinda não há avaliações

- Interest Rates and Their Role in FinanceDocumento17 páginasInterest Rates and Their Role in FinanceClyden Jaile RamirezAinda não há avaliações

- CHAPTER 5 - Portfolio TheoryDocumento58 páginasCHAPTER 5 - Portfolio TheoryKabutu ChuungaAinda não há avaliações

- SRGGDocumento31 páginasSRGGPinky LongalongAinda não há avaliações

- Intermediate Accounting 2Documento2 páginasIntermediate Accounting 2stephbatac241Ainda não há avaliações

- Tax ReviewerDocumento4 páginasTax ReviewerMel Loise DelmoroAinda não há avaliações

- The Cost of Capital: Multiple Choice QuestionsDocumento26 páginasThe Cost of Capital: Multiple Choice QuestionsRodAinda não há avaliações

- Chapter 6 VDocumento14 páginasChapter 6 VAdd AllAinda não há avaliações

- Chap12 (Capital Budgeting and Estimating Cash Flows) VanHorne&Brigham, CabreaDocumento4 páginasChap12 (Capital Budgeting and Estimating Cash Flows) VanHorne&Brigham, CabreaClaudine DuhapaAinda não há avaliações

- Tax 1 C1,3Documento10 páginasTax 1 C1,3Artjerjes Comendador PorrasAinda não há avaliações

- Incom Taxation 21 Chapter 3Documento33 páginasIncom Taxation 21 Chapter 3Charl RegenciaAinda não há avaliações

- Quiz On Fringe Benefit Tax and Dealings in Properties (ACOBA 2TAY2021 BBINCTAX)Documento7 páginasQuiz On Fringe Benefit Tax and Dealings in Properties (ACOBA 2TAY2021 BBINCTAX)Nicole Daphne FigueroaAinda não há avaliações

- Gross IncomeDocumento32 páginasGross IncomeMariaCarlaMañagoAinda não há avaliações

- IFRS Ethiopia D1S3 Presentation and Disclosure 3Documento69 páginasIFRS Ethiopia D1S3 Presentation and Disclosure 3Yalem Alemayehu100% (1)

- SARIEPHINE GRACE ARAS-ACTIVITY No 2 Corporate Income TaxDocumento8 páginasSARIEPHINE GRACE ARAS-ACTIVITY No 2 Corporate Income TaxSariephine Grace ArasAinda não há avaliações

- Chapter 3 Predetermined FOH RatesDocumento37 páginasChapter 3 Predetermined FOH RatesAtif SaeedAinda não há avaliações

- Quiz 3 InclusionsDocumento4 páginasQuiz 3 InclusionshotgirlsummerAinda não há avaliações

- Chapter IV Gross Income NotesDocumento5 páginasChapter IV Gross Income NotesJasmin AlapagAinda não há avaliações

- M6 - Deductions P3 (13B) Students'Documento56 páginasM6 - Deductions P3 (13B) Students'micaella pasionAinda não há avaliações

- Tutorial 1: 1. What Is The Basic Functions of Financial Markets?Documento6 páginasTutorial 1: 1. What Is The Basic Functions of Financial Markets?Ramsha ShafeelAinda não há avaliações

- Introduction To Business Taxes: September 4, 2020Documento20 páginasIntroduction To Business Taxes: September 4, 2020Bancas YvonAinda não há avaliações

- Mixed Income EarnersDocumento6 páginasMixed Income EarnersEzi AngelesAinda não há avaliações

- Cost of Capital Capital BudgetingDocumento19 páginasCost of Capital Capital BudgetingFahad AliAinda não há avaliações

- IAS 19 SummaryDocumento6 páginasIAS 19 SummaryMuchaa VlogAinda não há avaliações

- 13corporate Social Responsibility in International BusinessDocumento23 páginas13corporate Social Responsibility in International BusinessShruti SharmaAinda não há avaliações

- Universal BankDocumento1 páginaUniversal Bankhailene lorenaAinda não há avaliações

- Midterm Exam Problem Submissions: 420, 000andshareholder Equityof SDocumento3 páginasMidterm Exam Problem Submissions: 420, 000andshareholder Equityof SkvelezAinda não há avaliações

- Horizontal Analysis Interpretation PDFDocumento2 páginasHorizontal Analysis Interpretation PDFAlison JcAinda não há avaliações

- Auditing Chapter 1Documento7 páginasAuditing Chapter 1Sigei LeonardAinda não há avaliações

- Chapter 11-12 VDocumento30 páginasChapter 11-12 VAdd AllAinda não há avaliações

- Managerial EconomicsDocumento7 páginasManagerial EconomicsMohsinali2100% (1)

- Tax Chap 14 To 15Documento7 páginasTax Chap 14 To 15Jea XeleneAinda não há avaliações

- ConsumerismDocumento16 páginasConsumerismTamal ChattarajAinda não há avaliações

- IFRS 9 Financial Instruments - F7Documento39 páginasIFRS 9 Financial Instruments - F7TD2 from Henry HarvinAinda não há avaliações

- Activity Percentage of Time: Unloading 40% Counting 25 Inspecting 35Documento9 páginasActivity Percentage of Time: Unloading 40% Counting 25 Inspecting 35Alia ShabbirAinda não há avaliações

- Accounting For Income Tax: Technical KnowledgeDocumento42 páginasAccounting For Income Tax: Technical KnowledgeAngela Miles DizonAinda não há avaliações

- Chapter Three CVP AnalysisDocumento65 páginasChapter Three CVP AnalysisBettyAinda não há avaliações

- The Pioneer Legislation and Its Tax Implications AwokeDocumento12 páginasThe Pioneer Legislation and Its Tax Implications Awokeawokede100% (2)

- Individual Income TaxationDocumento50 páginasIndividual Income TaxationGab RielAinda não há avaliações

- Interest Rates Determination 3Documento38 páginasInterest Rates Determination 3kafi100% (1)

- 7.basic Income TaxationDocumento4 páginas7.basic Income TaxationMerlajoy VillanuevaAinda não há avaliações

- Management Accounting Concepts and TechniquesDocumento277 páginasManagement Accounting Concepts and TechniquesCalvince OumaAinda não há avaliações

- The Following Unadjusted Trial Balance Is For Ace Construction CoDocumento1 páginaThe Following Unadjusted Trial Balance Is For Ace Construction Cotrilocksp SinghAinda não há avaliações

- Economic DevelopmentDocumento17 páginasEconomic DevelopmentVher Christopher Ducay100% (1)

- CFAS - Chapter 26Documento49 páginasCFAS - Chapter 26Syrell NaborAinda não há avaliações

- AE 27 Lesson 3 Understanding FSDocumento26 páginasAE 27 Lesson 3 Understanding FSMARC BENNETH BERIÑAAinda não há avaliações

- Chapter Five Inventory Management - Chapter 4Documento10 páginasChapter Five Inventory Management - Chapter 4eferemAinda não há avaliações

- Tax SemisDocumento50 páginasTax SemisTeam MindanaoAinda não há avaliações

- IAS 19 Employee Benefits (2021)Documento6 páginasIAS 19 Employee Benefits (2021)Tawanda Tatenda Herbert100% (1)

- Chapter08 PDFDocumento22 páginasChapter08 PDFBabuM ACC FIN ECOAinda não há avaliações

- On The Dot Trading Statement of Financial Position As of December 31 2017 2016 Increase (Decrease) AmountDocumento3 páginasOn The Dot Trading Statement of Financial Position As of December 31 2017 2016 Increase (Decrease) AmountRuthAinda não há avaliações

- GROUP 10 (Corporation Income Taxation - Regular Corporation)Documento16 páginasGROUP 10 (Corporation Income Taxation - Regular Corporation)Denmark David Gaspar NatanAinda não há avaliações

- Week 7 Module 7 TAX2 - Business and Transfer Taxation - PADAYHAGDocumento23 páginasWeek 7 Module 7 TAX2 - Business and Transfer Taxation - PADAYHAGfernan opeliñaAinda não há avaliações

- Chapter One Accounting Principles and Professional PracticeDocumento22 páginasChapter One Accounting Principles and Professional PracticeHussen Abdulkadir100% (1)

- CHAPTER I and IIDocumento13 páginasCHAPTER I and IIPritz Marc Bautista MorataAinda não há avaliações

- Gen. Principles of TaxationDocumento22 páginasGen. Principles of TaxationPageduesca RouelAinda não há avaliações

- Quiz-01-10-16-20-Class Finacc7 DDocumento8 páginasQuiz-01-10-16-20-Class Finacc7 DKhevin AlvaradoAinda não há avaliações

- Income Taxation Term Assessment 2 SEM SY 2019 - 2020: Coverage: Chapter 8 - 11Documento4 páginasIncome Taxation Term Assessment 2 SEM SY 2019 - 2020: Coverage: Chapter 8 - 11Nhel AlvaroAinda não há avaliações

- 5Documento46 páginas5Navindra JaggernauthAinda não há avaliações

- Richard 2019Documento29 páginasRichard 2019Richard MoszynskiAinda não há avaliações

- Income Taxation For IndividualsDocumento60 páginasIncome Taxation For IndividualsFrancis Elaine FortunAinda não há avaliações

- Proforma InvoiceDocumento3 páginasProforma InvoiceSuresh KumarAinda não há avaliações

- Solved Interpret Each of The Following Citations A 54 T C 1514 1970 BDocumento1 páginaSolved Interpret Each of The Following Citations A 54 T C 1514 1970 BAnbu jaromiaAinda não há avaliações

- Hotel Diwanki Building, Daman, INCOME TAX OFFICE, Hotel Diwanji Building, Devkanand, DAMAN, Gujarat, 396210 Email: Daman - Ito@Incometax - Gov.InDocumento2 páginasHotel Diwanki Building, Daman, INCOME TAX OFFICE, Hotel Diwanji Building, Devkanand, DAMAN, Gujarat, 396210 Email: Daman - Ito@Incometax - Gov.Insanjiv kumarAinda não há avaliações

- Form No. Requirement Deadline For Manual FilersDocumento1 páginaForm No. Requirement Deadline For Manual FilersLhyraAinda não há avaliações

- Income Tax Quiz 5Documento3 páginasIncome Tax Quiz 5Calix CasanovaAinda não há avaliações

- Challan Cum Tax InvoiceDocumento1 páginaChallan Cum Tax InvoiceSahil KadamAinda não há avaliações

- Supdt. of Police, Baruipur Police District Pay Slip Government of West BengalDocumento1 páginaSupdt. of Police, Baruipur Police District Pay Slip Government of West BengalSumita KhanAinda não há avaliações

- Fort Langley BIA Budget (8) SpecialDocumento2 páginasFort Langley BIA Budget (8) Speciallangleyrecord8339Ainda não há avaliações

- Tax InvoiceDocumento1 páginaTax InvoiceMR. MU.Ainda não há avaliações

- Tax Invoice Shankara Bakthula Narasimha Chary: Billing Period Invoice Date Amount Payable Due Date Amount After Due DateDocumento3 páginasTax Invoice Shankara Bakthula Narasimha Chary: Billing Period Invoice Date Amount Payable Due Date Amount After Due DateJeevanreddy JeevanreddyAinda não há avaliações

- Set Off and Carry Forward of Losses An AnalysisDocumento6 páginasSet Off and Carry Forward of Losses An AnalysisRam IyerAinda não há avaliações

- Tax Evasion and AvoidanceDocumento11 páginasTax Evasion and AvoidanceMerlita TuralbaAinda não há avaliações

- Quiz On VAT154623Documento5 páginasQuiz On VAT154623Sandy100% (1)

- SalarySlip 1 - 2023Documento1 páginaSalarySlip 1 - 2023Rizham IbniAinda não há avaliações

- Diedrich v. Commissioner, 457 U.S. 191 (1982)Documento10 páginasDiedrich v. Commissioner, 457 U.S. 191 (1982)Scribd Government DocsAinda não há avaliações

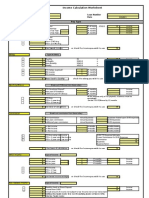

- Income Calculation WorksheetDocumento1 páginaIncome Calculation Worksheetrush2serveAinda não há avaliações

- Revenue Memorandum Circular No. 26-2018: Bureau of Internal RevenueDocumento3 páginasRevenue Memorandum Circular No. 26-2018: Bureau of Internal RevenuePaul GeorgeAinda não há avaliações

- Taxation 101 Income Taxation: Mr. Mario M. Castro, Cpa, MBDocumento12 páginasTaxation 101 Income Taxation: Mr. Mario M. Castro, Cpa, MBKristine Aubrey AlvarezAinda não há avaliações

- Excitel - Procare A DecDocumento2 páginasExcitel - Procare A Decmdumar0164Ainda não há avaliações

- Pay Slip Components: Australian Concert and Entertainment Security Pty LTDDocumento1 páginaPay Slip Components: Australian Concert and Entertainment Security Pty LTDGaro KhatcherianAinda não há avaliações

- Balongis Taxable de Minimis BenefitsDocumento3 páginasBalongis Taxable de Minimis BenefitsKrizah Marie CaballeroAinda não há avaliações

- Pay Slip JunDocumento1 páginaPay Slip Junraj d100% (1)

- FABM2Documento27 páginasFABM2Shai Rose Jumawan QuiboAinda não há avaliações

- Innocent Spouse FlowchartDocumento1 páginaInnocent Spouse FlowchartHansley Templeton CookAinda não há avaliações

- Laws of Taxation in TanzaniaDocumento508 páginasLaws of Taxation in TanzaniaRuhuro tetere100% (3)

- Chapter 26 MCQs On International TaxationDocumento26 páginasChapter 26 MCQs On International TaxationSuranjali Tiwari100% (1)

- W-8BEN: Certificate of Foreign Status of Beneficial Owner For United States Tax Withholding and Reporting (Individuals)Documento1 páginaW-8BEN: Certificate of Foreign Status of Beneficial Owner For United States Tax Withholding and Reporting (Individuals)DupanAinda não há avaliações

- CPA Exam REG Area 04 - Individual TaxationDocumento3 páginasCPA Exam REG Area 04 - Individual TaxationManny MarroquinAinda não há avaliações