Você também pode gostar

- WILEY Stock - Trader.Almanac.2005 PDFDocumento195 páginasWILEY Stock - Trader.Almanac.2005 PDFRazvan Filimon100% (1)

- ICT Method for Finding High Probability Day Trading SetupsDocumento50 páginasICT Method for Finding High Probability Day Trading Setupsjim kang100% (1)

- Complete Forex Trading Guide - Forex - Doc-1Documento228 páginasComplete Forex Trading Guide - Forex - Doc-1Raph Sun90% (40)

- Hero Motocorp FinancialsDocumento41 páginasHero Motocorp FinancialssahilkuAinda não há avaliações

- John M CaseDocumento10 páginasJohn M Caseadrian_simm100% (1)

- Key Mechanics of Corporate Bonds ExplainedDocumento54 páginasKey Mechanics of Corporate Bonds ExplainedAnna LinAinda não há avaliações

- Corporate Finance Outline, Spring 2013Documento60 páginasCorporate Finance Outline, Spring 2013Kasem Ahmed100% (1)

- Solution q1 in q3 CapitalAssetPricingModelHomeworkDocumento14 páginasSolution q1 in q3 CapitalAssetPricingModelHomeworkAbdu AbdoulayeAinda não há avaliações

- Corporate Actions: A Guide to Securities Event ManagementNo EverandCorporate Actions: A Guide to Securities Event ManagementAinda não há avaliações

- Individual AssignmentDocumento10 páginasIndividual Assignmentparitosh nayakAinda não há avaliações

- Case 1 Spreadsheet - EI DuPontDocumento6 páginasCase 1 Spreadsheet - EI DuPontSamuel BishopAinda não há avaliações

- HDFC NL-7-operating-expenses-schedule83ba5e2655f74e719aff9e122100f65d (1)Documento2 páginasHDFC NL-7-operating-expenses-schedule83ba5e2655f74e719aff9e122100f65d (1)SatyamSinghAinda não há avaliações

- quant Mid Cap Fund MONTHLY PORTFOLIO STATEMENT AS ON 30 Sep 2022Documento9 páginasquant Mid Cap Fund MONTHLY PORTFOLIO STATEMENT AS ON 30 Sep 2022vnrAinda não há avaliações

- Updated Par DashboardDocumento19 páginasUpdated Par DashboardGobi IlaiAinda não há avaliações

- Nepal Stock Exchange Limited: Singhadurbar Plaza, Kathmandu, Nepal. Phone: 977-1-4250758,4250735, Fax: 977-1-4262538Documento58 páginasNepal Stock Exchange Limited: Singhadurbar Plaza, Kathmandu, Nepal. Phone: 977-1-4250758,4250735, Fax: 977-1-4262538member2 mtriAinda não há avaliações

- Weekly Product Breakdown 20220207Documento1 páginaWeekly Product Breakdown 20220207sdfasdfahgadsAinda não há avaliações

- Intrinsic Value Analysis of Tata Motors LtdDocumento24 páginasIntrinsic Value Analysis of Tata Motors LtdApurvAdarshAinda não há avaliações

- ICICI form-nl-7-operating-expenses-scheduleDocumento2 páginasICICI form-nl-7-operating-expenses-scheduleSatyamSinghAinda não há avaliações

- Nepal Stock Exchange Limited: Singhadurbar Plaza, Kathmandu, Nepal. Phone: 977-1-4250758,4250735, Fax: 977-1-4262538Documento76 páginasNepal Stock Exchange Limited: Singhadurbar Plaza, Kathmandu, Nepal. Phone: 977-1-4250758,4250735, Fax: 977-1-4262538Dammar JoshiAinda não há avaliações

- Nepal Stock Exchange Limited: Singhadurbar Plaza, Kathmandu, Nepal. Phone: 977-1-4250758,4250735, Fax: 977-1-4262538Documento59 páginasNepal Stock Exchange Limited: Singhadurbar Plaza, Kathmandu, Nepal. Phone: 977-1-4250758,4250735, Fax: 977-1-4262538sagar gurungAinda não há avaliações

- Case Harvard - Marriott Corporation Restructuring - SpreadsheetDocumento25 páginasCase Harvard - Marriott Corporation Restructuring - SpreadsheetCarla ArecheAinda não há avaliações

- Consolidated Financial Statements - FY23Documento59 páginasConsolidated Financial Statements - FY23Bhuvaneshwari .AAinda não há avaliações

- HSL - Daily Derivative Overview 11092023-202309110910404544703Documento10 páginasHSL - Daily Derivative Overview 11092023-202309110910404544703vikash.4051591Ainda não há avaliações

- Exercise SampleDocumento62 páginasExercise SampleChandra SekarAinda não há avaliações

- T-bill Auctions 2009-2010 Summary and Ownership Patterns of Govt SecuritiesDocumento4 páginasT-bill Auctions 2009-2010 Summary and Ownership Patterns of Govt SecuritiesIshwar ChhedaAinda não há avaliações

- Nepal Stock Exchange Limited: Singhadurbar Plaza, Kathmandu, Nepal. Phone: 977-1-4250758,4250735, Fax: 977-1-4262538Documento15 páginasNepal Stock Exchange Limited: Singhadurbar Plaza, Kathmandu, Nepal. Phone: 977-1-4250758,4250735, Fax: 977-1-4262538axzc sAinda não há avaliações

- BhartiAndMTN FinancialsDocumento10 páginasBhartiAndMTN FinancialsGirish RamachandraAinda não há avaliações

- CF-Export-05-03-2024 10Documento11 páginasCF-Export-05-03-2024 10v4d4f8hkc2Ainda não há avaliações

- Portfolio & Risk Management: Presented By:-Shubham Dave Roll No:-02Documento8 páginasPortfolio & Risk Management: Presented By:-Shubham Dave Roll No:-02vipul sutharAinda não há avaliações

- BEML Limited Annual Report 2011-12 Financial HighlightsDocumento121 páginasBEML Limited Annual Report 2011-12 Financial HighlightsNihit SandAinda não há avaliações

- Assets Liabilites and Owners' EquityDocumento5 páginasAssets Liabilites and Owners' EquityVinay JajuAinda não há avaliações

- ReebokDocumento23 páginasReebokChristian Fernández OchoaAinda não há avaliações

- NRB KFI-Ashwin-2079 PDFDocumento1 páginaNRB KFI-Ashwin-2079 PDFLikesh ShresthaAinda não há avaliações

- Apollo Tyres DCF AnalysisDocumento20 páginasApollo Tyres DCF AnalysisnishantAinda não há avaliações

- FinolexCablesFSA Final DRAFTDocumento14 páginasFinolexCablesFSA Final DRAFTAbhisek MohantyAinda não há avaliações

- 05-03-22 Focal Cma DataDocumento6 páginas05-03-22 Focal Cma DataShivam SharmaAinda não há avaliações

- Nepal Stock Exchange Summary Report: Market Stats and Sector IndexDocumento15 páginasNepal Stock Exchange Summary Report: Market Stats and Sector IndexJeevan ChaudharyAinda não há avaliações

- Quant Large Mid Fund Sep 2022Documento9 páginasQuant Large Mid Fund Sep 2022vnrAinda não há avaliações

- MECWIN Investment ProposalDocumento4 páginasMECWIN Investment ProposalVamsi PavuluriAinda não há avaliações

- Growth, Profitability, and Financial Ratios For Citra Marga Nusaphala Persada TBK (CMNP) FromDocumento1 páginaGrowth, Profitability, and Financial Ratios For Citra Marga Nusaphala Persada TBK (CMNP) FromadjipramAinda não há avaliações

- FS-Consolidated 84Documento6 páginasFS-Consolidated 84trollilluminati123Ainda não há avaliações

- Enhanced Comprehensive Local Integration Program (E-CLIP) : UpdatesDocumento15 páginasEnhanced Comprehensive Local Integration Program (E-CLIP) : UpdatesYann LauanAinda não há avaliações

- Periodic Disclosures: FORM L-38 Business Acquisition Through Different Channels (Individuals)Documento1 páginaPeriodic Disclosures: FORM L-38 Business Acquisition Through Different Channels (Individuals)jdchandrapal4980Ainda não há avaliações

- 2020 Nevada 10 16 20Documento1 página2020 Nevada 10 16 20Las Vegas Review-JournalAinda não há avaliações

- Financial Statements Analysis of Companies (Non-Financial) Listed at Karachi Stock Exchange 2010-2015Documento29 páginasFinancial Statements Analysis of Companies (Non-Financial) Listed at Karachi Stock Exchange 2010-2015Nazish HussainAinda não há avaliações

- Quote 202207janDocumento43 páginasQuote 202207janBilal AhmadAinda não há avaliações

- Supreme Annual Report 15 16Documento104 páginasSupreme Annual Report 15 16adoniscalAinda não há avaliações

- btv201617 PDFDocumento1 páginabtv201617 PDFShantanuKaleAinda não há avaliações

- SIVBQ SVB Financial Group Annual Balance Sheet - WSJDocumento1 páginaSIVBQ SVB Financial Group Annual Balance Sheet - WSJSanchit BudhirajaAinda não há avaliações

- Bharat 22 EtfDocumento6 páginasBharat 22 EtfSahi GAinda não há avaliações

- Chicago Market Share YTD 4-17-09Documento2 páginasChicago Market Share YTD 4-17-09stevemcewen2992100% (1)

- Quant Tax Plan Sep 2022Documento9 páginasQuant Tax Plan Sep 2022vnrAinda não há avaliações

- TCS RATIO Calulations-1Documento4 páginasTCS RATIO Calulations-1reddynagendrapalle123Ainda não há avaliações

- We Are Not Above Nature, We Are A Part of NatureDocumento216 páginasWe Are Not Above Nature, We Are A Part of NaturePRIYADARSHI GOURAVAinda não há avaliações

- Reporte Copeme Imf Mar2023Documento52 páginasReporte Copeme Imf Mar2023Jesús Del Prado MattosAinda não há avaliações

- Jindal Steels & Power LimitedDocumento10 páginasJindal Steels & Power LimitedHIMANSHU RAWATAinda não há avaliações

- DSCR Gaurang Singh & Govardhan SinghDocumento6 páginasDSCR Gaurang Singh & Govardhan SinghPriya KalraAinda não há avaliações

- OMSEC Morning Note 26 09 2022Documento6 páginasOMSEC Morning Note 26 09 2022Ropafadzo KwarambaAinda não há avaliações

- PSX Quote 31-08-2022Documento42 páginasPSX Quote 31-08-2022wasayrazaAinda não há avaliações

- Complete Spreadsheet - From 2020Documento233 páginasComplete Spreadsheet - From 2020cpacpacpaAinda não há avaliações

- Bank Balance Sheet and Profit-Loss ReportDocumento11 páginasBank Balance Sheet and Profit-Loss ReportSyam SudarAinda não há avaliações

- ARN Code of The Bank and Financial Companies of IndiaDocumento10 páginasARN Code of The Bank and Financial Companies of IndiaNirbhay KumarAinda não há avaliações

- Quantum Leap Forward: Particulars 2007-08 2008-09 2009-2010 A Key IndicatorsDocumento7 páginasQuantum Leap Forward: Particulars 2007-08 2008-09 2009-2010 A Key IndicatorsHemant JangidAinda não há avaliações

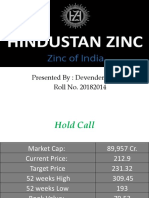

- Hindustan ZincDocumento8 páginasHindustan ZincDevender SharmaAinda não há avaliações

- Beml Limited: Annual Report 2012-2013Documento162 páginasBeml Limited: Annual Report 2012-2013Nihit SandAinda não há avaliações

- Ten YearDocumento1 páginaTen Yearvikkyjan19Ainda não há avaliações

- S BqFC2 - T5KgahQtv8 SXQ - Module 3 7 iMBA Example LBO TypeDocumento8 páginasS BqFC2 - T5KgahQtv8 SXQ - Module 3 7 iMBA Example LBO TypeharshAinda não há avaliações

- To Download The TCPro Application-1Documento42 páginasTo Download The TCPro Application-1Shahrizan Abdul RahmanAinda não há avaliações

- Valuation of Securities: by - ) Ajay Rana, Sonam Gupta, Shivani, Gurpreet, ShilpaDocumento46 páginasValuation of Securities: by - ) Ajay Rana, Sonam Gupta, Shivani, Gurpreet, ShilpaTanmoy ChakrabortyAinda não há avaliações

- 8 12Documento13 páginas8 12Nguyen TrangAinda não há avaliações

- Illustrative Financial Statements: Private Equity & Venture CapitalDocumento36 páginasIllustrative Financial Statements: Private Equity & Venture CapitalCreative MarqetingAinda não há avaliações

- Bloomberg For Education Links 9.12Documento27 páginasBloomberg For Education Links 9.12Amogh SumanAinda não há avaliações

- Module 2 - AnswersDocumento26 páginasModule 2 - AnswersSinghan SAinda não há avaliações

- Concept, Nature & Kinds of Shares: Corporate Law ProjectDocumento12 páginasConcept, Nature & Kinds of Shares: Corporate Law ProjectEHTMAM KHANAinda não há avaliações

- Financial Derivative Ajitav AcharyaDocumento45 páginasFinancial Derivative Ajitav AcharyaBhabani Sankar BrahmaAinda não há avaliações

- Nse Research Analysis 2020Documento53 páginasNse Research Analysis 2020Anuj ThapaAinda não há avaliações

- Reliance Monthly Portfolios 31 03 2013 FinalDocumento292 páginasReliance Monthly Portfolios 31 03 2013 Finalluvisfact7616Ainda não há avaliações

- Week 3 LectureDocumento31 páginasWeek 3 LectureAnselmAinda não há avaliações

- Relative ValuationDocumento29 páginasRelative ValuationOnal RautAinda não há avaliações

- Chapter 4 - Contingent Claim ValuationDocumento2 páginasChapter 4 - Contingent Claim ValuationSteffany RoqueAinda não há avaliações

- Government Securities (Gsecs), India: 1. What Is A Government Security?Documento4 páginasGovernment Securities (Gsecs), India: 1. What Is A Government Security?baby0310Ainda não há avaliações

- 3 Waas Presentation Slide DeckDocumento26 páginas3 Waas Presentation Slide Decktuborg2011Ainda não há avaliações

- PT - Kuncimas Agromina AJCE Side Type 20 T PDFDocumento1 páginaPT - Kuncimas Agromina AJCE Side Type 20 T PDFRidloAinda não há avaliações

- Private PlacementDocumento24 páginasPrivate PlacementVrinda GargAinda não há avaliações

- Comp-XM - Inquirer ReportDocumento29 páginasComp-XM - Inquirer ReportOmprakash PandeyAinda não há avaliações

- 21 - 27 Nov 2022Documento21 páginas21 - 27 Nov 2022jay pujaraAinda não há avaliações

- Bond Examples FabozziDocumento36 páginasBond Examples FabozziMauricio Bedoya100% (1)

- TreehousedraftDocumento299 páginasTreehousedraftjkaraniAinda não há avaliações

- Kidlat Chronicles: Part 1: Profiting From Upward MomentumDocumento22 páginasKidlat Chronicles: Part 1: Profiting From Upward MomentumbalalovmyfrensAinda não há avaliações

- KEATProX Feature, sHARE TRADINGDocumento7 páginasKEATProX Feature, sHARE TRADINGindresh.vermaAinda não há avaliações