Você também pode gostar

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- Emb170 190Documento34 páginasEmb170 190api-375762975% (4)

- 2007 02 Performanceanalysis - Phenom100Documento8 páginas2007 02 Performanceanalysis - Phenom100api-3757629Ainda não há avaliações

- Regional JetsDocumento20 páginasRegional Jetsapi-3757629Ainda não há avaliações

- ThompsonDocumento16 páginasThompsonapi-3757629Ainda não há avaliações

- Palestra SucupiraDocumento22 páginasPalestra Sucupiraapi-3757629Ainda não há avaliações

- Strategy 01 Manu Amitabh FinalDocumento19 páginasStrategy 01 Manu Amitabh FinalSwapnil PatilAinda não há avaliações

- Brasilen 2Documento17 páginasBrasilen 2api-3757629Ainda não há avaliações

- F5Ch 02Documento29 páginasF5Ch 02api-3757629Ainda não há avaliações

- Strategic ThinkingDocumento20 páginasStrategic Thinkingapi-375762967% (6)

- StrathinkDocumento3 páginasStrathinkapi-3757629Ainda não há avaliações

- StrategyDocumento43 páginasStrategyapi-3757629Ainda não há avaliações

- Bus StrategyDocumento25 páginasBus StrategyChavan VirajAinda não há avaliações

- Total Quality Management (TQM) : Prepared byDocumento14 páginasTotal Quality Management (TQM) : Prepared byapi-3757629100% (1)

- Investment FunctionDocumento17 páginasInvestment Functionapi-3757629Ainda não há avaliações

- Price IndicesDocumento14 páginasPrice Indicesapi-3757629Ainda não há avaliações

- Evoluton of Strategic Thinking and Lessons For Managers: Associate Professor Mehmet BARCA University of Sakarya, TurkeyDocumento18 páginasEvoluton of Strategic Thinking and Lessons For Managers: Associate Professor Mehmet BARCA University of Sakarya, Turkeyapi-3757629Ainda não há avaliações

- MoneyDocumento26 páginasMoneyapi-3757629Ainda não há avaliações

- InflationDocumento10 páginasInflationapi-3757629Ainda não há avaliações

- Monetary and Fiscal PolicyDocumento27 páginasMonetary and Fiscal Policyapi-3757629100% (2)

- Report BudgetDocumento19 páginasReport Budgetapi-3757629Ainda não há avaliações

- Sales and Distribution-Mm: Made By-Bhaibhab Nath Deepshikha Bansal Jignesh Joshi Mehak Oberoi Rashi Jain Sonal SmritiDocumento22 páginasSales and Distribution-Mm: Made By-Bhaibhab Nath Deepshikha Bansal Jignesh Joshi Mehak Oberoi Rashi Jain Sonal Smritiapi-3757629Ainda não há avaliações

- SCM FinDocumento21 páginasSCM Finapi-3757629100% (2)

- RFID IT PPT 2003Documento20 páginasRFID IT PPT 2003api-3757629100% (2)

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- Chapter 15 - Taxation and Corporate IncomeDocumento26 páginasChapter 15 - Taxation and Corporate Incomewatts1Ainda não há avaliações

- Som - Organizational Redesign at BPCL The Challenge of PrivaDocumento12 páginasSom - Organizational Redesign at BPCL The Challenge of PrivaHitanchi KulkarniAinda não há avaliações

- Balance Sheet of State Bank of IndiaDocumento8 páginasBalance Sheet of State Bank of IndiaJyoti VijayAinda não há avaliações

- Auditors Report 2012Documento89 páginasAuditors Report 2012Md MasumAinda não há avaliações

- Gabriel A.D. Preireich - The Nature of Dividends, 1934Documento248 páginasGabriel A.D. Preireich - The Nature of Dividends, 1934Pedro GamaAinda não há avaliações

- Business Finance Week 2 2Documento14 páginasBusiness Finance Week 2 2Phoebe Rafunsel Sumbongan Juyad100% (1)

- Capital Structure and Dividend PolicyDocumento25 páginasCapital Structure and Dividend PolicySarah Mae SudayanAinda não há avaliações

- Annual Report - SKNL - SmallDocumento164 páginasAnnual Report - SKNL - SmallShashikanth Ramamurthy100% (1)

- Financial Accounting One - PART IIDocumento43 páginasFinancial Accounting One - PART IIDennis VelasquezAinda não há avaliações

- Analysis of Hofstede's 5-D Model in SAUDI ARABIADocumento9 páginasAnalysis of Hofstede's 5-D Model in SAUDI ARABIAKhloud Uitm100% (3)

- NRI TaxationDocumento9 páginasNRI TaxationTekumani Naveen KumarAinda não há avaliações

- L&T Infotech: Strong Operational PerformanceDocumento12 páginasL&T Infotech: Strong Operational Performanceashok yadavAinda não há avaliações

- BhelDocumento109 páginasBhelKuldeep SinghAinda não há avaliações

- Corporate Finance Ch. 16Documento29 páginasCorporate Finance Ch. 16diaAinda não há avaliações

- FMA Project (Working Capital)Documento19 páginasFMA Project (Working Capital)PowerPoint GoAinda não há avaliações

- Dividend Decisions-1Documento24 páginasDividend Decisions-1TIBUGWISHA IVANAinda não há avaliações

- Financial Statements Analysis - An IntroductionDocumento19 páginasFinancial Statements Analysis - An Introductionbiniam meazanehAinda não há avaliações

- This Study Resource Was: CASTILLO, Lauren Financial Management Mam Barquez BSA-3 Problem 1 (Pro Forma Statements)Documento5 páginasThis Study Resource Was: CASTILLO, Lauren Financial Management Mam Barquez BSA-3 Problem 1 (Pro Forma Statements)KATHRYN CLAUDETTE RESENTE100% (2)

- Conceptual Frameworks and Accounting Standards PDFDocumento58 páginasConceptual Frameworks and Accounting Standards PDFJieyan Oliveros0% (1)

- New TDS & TCS Provisions - SummaryDocumento12 páginasNew TDS & TCS Provisions - Summaryyashgoyal87502Ainda não há avaliações

- Madison Hotel CaseDocumento31 páginasMadison Hotel CaseCaroline SmithAinda não há avaliações

- Basic Cooperative Course (BCC)Documento75 páginasBasic Cooperative Course (BCC)Troy Eric O. Cordero100% (1)

- A Study On Working Capital Management With Special Reference To Tube Products of India Limited, ChennaiDocumento41 páginasA Study On Working Capital Management With Special Reference To Tube Products of India Limited, ChennaiBasant NagarAinda não há avaliações

- REVENUE MEMORANDUM CIRCULAR NO. 40-2004 Issued On July 1, 2004Documento2 páginasREVENUE MEMORANDUM CIRCULAR NO. 40-2004 Issued On July 1, 2004Kyrzen NovillaAinda não há avaliações

- WCM - Unit 2 Cash ManagementDocumento51 páginasWCM - Unit 2 Cash ManagementkartikAinda não há avaliações

- Questions and Answers For Essay QuestionsDocumento12 páginasQuestions and Answers For Essay QuestionsPushpendra Singh ShekhawatAinda não há avaliações

- Warren Buffett and Wall StreetDocumento4 páginasWarren Buffett and Wall StreetcoolchadsAinda não há avaliações

- Startups ShabdkoshDocumento89 páginasStartups ShabdkoshRujuta Kulkarni0% (1)

- ch01 PDFDocumento59 páginasch01 PDFsaad bin saadaqatAinda não há avaliações

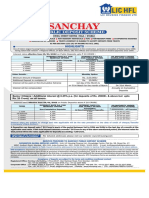

- Sanchay: Public Deposit SchemeDocumento1 páginaSanchay: Public Deposit SchemeShrikant MasulkerAinda não há avaliações