Você também pode gostar

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNo EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceNota: 4 de 5 estrelas4/5 (895)

- Role of A Managerial EconomistDocumento1 páginaRole of A Managerial EconomistSurya PanwarAinda não há avaliações

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNo EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeNota: 4 de 5 estrelas4/5 (5794)

- Principles of Managerial EconomicsDocumento7 páginasPrinciples of Managerial EconomicsSurya PanwarAinda não há avaliações

- Computer Graphics VIII Comp. Sci. & Engg. 8 Semester Question Bank Unit-IDocumento5 páginasComputer Graphics VIII Comp. Sci. & Engg. 8 Semester Question Bank Unit-ISurya PanwarAinda não há avaliações

- Managerial Economics Lecture Firm AlternativeDocumento42 páginasManagerial Economics Lecture Firm AlternativeSurya PanwarAinda não há avaliações

- The Yellow House: A Memoir (2019 National Book Award Winner)No EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Nota: 4 de 5 estrelas4/5 (98)

- Marginal Ism and Incremental IsmDocumento7 páginasMarginal Ism and Incremental IsmSurya PanwarAinda não há avaliações

- Managerial EconomicsDocumento15 páginasManagerial EconomicsSurya PanwarAinda não há avaliações

- Marginal Ism and Incremental IsmDocumento7 páginasMarginal Ism and Incremental IsmSurya PanwarAinda não há avaliações

- The Little Book of Hygge: Danish Secrets to Happy LivingNo EverandThe Little Book of Hygge: Danish Secrets to Happy LivingNota: 3.5 de 5 estrelas3.5/5 (400)

- A Market Structure Characterized by A Large Number of Small FirmsDocumento9 páginasA Market Structure Characterized by A Large Number of Small FirmsSurya PanwarAinda não há avaliações

- Never Split the Difference: Negotiating As If Your Life Depended On ItNo EverandNever Split the Difference: Negotiating As If Your Life Depended On ItNota: 4.5 de 5 estrelas4.5/5 (838)

- Cost Analysis: C.M.JoshiDocumento14 páginasCost Analysis: C.M.JoshiSurya PanwarAinda não há avaliações

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNo EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureNota: 4.5 de 5 estrelas4.5/5 (474)

- List of Attempted Questions and AnswersDocumento3 páginasList of Attempted Questions and AnswersSurya PanwarAinda não há avaliações

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNo EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryNota: 3.5 de 5 estrelas3.5/5 (231)

- Demand Analysis: C.M.JoshiDocumento17 páginasDemand Analysis: C.M.JoshiSurya PanwarAinda não há avaliações

- Performanceiof 04Documento14 páginasPerformanceiof 04Surya PanwarAinda não há avaliações

- The Emperor of All Maladies: A Biography of CancerNo EverandThe Emperor of All Maladies: A Biography of CancerNota: 4.5 de 5 estrelas4.5/5 (271)

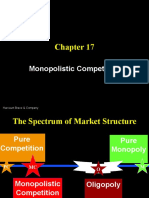

- Monopolistic Competition: Harcourt Brace & CompanyDocumento33 páginasMonopolistic Competition: Harcourt Brace & CompanySurya PanwarAinda não há avaliações

- Imperfect 3Documento17 páginasImperfect 3Surya PanwarAinda não há avaliações

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNo EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaNota: 4.5 de 5 estrelas4.5/5 (266)

- Monopolistic Competition Is A MarketDocumento8 páginasMonopolistic Competition Is A MarketSurya PanwarAinda não há avaliações

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNo EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersNota: 4.5 de 5 estrelas4.5/5 (345)

- Monopolistic Competition: Activity 3-12-1Documento11 páginasMonopolistic Competition: Activity 3-12-1Surya PanwarAinda não há avaliações

- Monopolistic and Oligopoly: © 2006 Thomson/South-WesternDocumento34 páginasMonopolistic and Oligopoly: © 2006 Thomson/South-WesternSurya PanwarAinda não há avaliações

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyNo EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyNota: 3.5 de 5 estrelas3.5/5 (2259)

- Market StructureDocumento42 páginasMarket StructureSurya PanwarAinda não há avaliações

- Team of Rivals: The Political Genius of Abraham LincolnNo EverandTeam of Rivals: The Political Genius of Abraham LincolnNota: 4.5 de 5 estrelas4.5/5 (234)

- Feenstra Taylor Econ CH06Documento64 páginasFeenstra Taylor Econ CH06Surya Panwar100% (2)

- The Unwinding: An Inner History of the New AmericaNo EverandThe Unwinding: An Inner History of the New AmericaNota: 4 de 5 estrelas4/5 (45)

- Monopolistic Competition and Product DifferentiationDocumento18 páginasMonopolistic Competition and Product DifferentiationSurya PanwarAinda não há avaliações

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNo EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreNota: 4 de 5 estrelas4/5 (1090)

- Chapter 10 Stud VerDocumento27 páginasChapter 10 Stud VerSurya PanwarAinda não há avaliações

- Introduction To Economics I Dr. Ka-Fu WONG: ECON 1001 ABDocumento29 páginasIntroduction To Economics I Dr. Ka-Fu WONG: ECON 1001 ABSurya PanwarAinda não há avaliações

- A Simple and Reliable Submental Intubation.68Documento4 páginasA Simple and Reliable Submental Intubation.68Tîrban Pantelimon FlorinAinda não há avaliações

- Shakespeare Ubd Unit PlanDocumento16 páginasShakespeare Ubd Unit Planapi-239477809Ainda não há avaliações

- Chapter 1 - Lesson 2 - Transforming Equations From Standard Form To General FormDocumento8 páginasChapter 1 - Lesson 2 - Transforming Equations From Standard Form To General FormhadukenAinda não há avaliações

- Relativity Space-Time and Cosmology - WudkaDocumento219 páginasRelativity Space-Time and Cosmology - WudkaAlan CalderónAinda não há avaliações

- Syllabus Financial AccountingDocumento3 páginasSyllabus Financial AccountingHusain ADAinda não há avaliações

- Clostridium BotulinumDocumento37 páginasClostridium Botulinummaria dulceAinda não há avaliações

- Problem Sheet 3 - External Forced Convection - WatermarkDocumento2 páginasProblem Sheet 3 - External Forced Convection - WatermarkUzair KhanAinda não há avaliações

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)No EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Nota: 4.5 de 5 estrelas4.5/5 (121)

- Hyperinflation of Zimbabwe and The Lesson For Zimbabwe: Foreign Trade University Faculty of Banking and FinanceDocumento38 páginasHyperinflation of Zimbabwe and The Lesson For Zimbabwe: Foreign Trade University Faculty of Banking and FinancePham Việt AnhAinda não há avaliações

- Police Log September 24, 2016Documento14 páginasPolice Log September 24, 2016MansfieldMAPoliceAinda não há avaliações

- TTD Accommodation ReceiptDocumento2 páginasTTD Accommodation ReceiptDharani KumarAinda não há avaliações

- Student EssaysDocumento41 páginasStudent EssaysAsif RahmanAinda não há avaliações

- Four Quartets: T.S. EliotDocumento32 páginasFour Quartets: T.S. Eliotschwarzgerat00000100% (1)

- FTec 150 - Intro To Meat ProcessingDocumento51 páginasFTec 150 - Intro To Meat ProcessingJessa Silvano ArgallonAinda não há avaliações

- Model-Checking: A Tutorial Introduction: January 1999Documento26 páginasModel-Checking: A Tutorial Introduction: January 1999Quý Trương QuangAinda não há avaliações

- Report On Sonepur MelaDocumento4 páginasReport On Sonepur Melakashtum23Ainda não há avaliações

- Ed508-5e-Lesson-Plan-Severe Weather EventsDocumento3 páginasEd508-5e-Lesson-Plan-Severe Weather Eventsapi-526575993Ainda não há avaliações

- Dual Nature and RadiationDocumento39 páginasDual Nature and RadiationWedger RealmeAinda não há avaliações

- Sri Anjaneya Cotton Mills LimitedDocumento63 páginasSri Anjaneya Cotton Mills LimitedPrashanth PB50% (2)

- WikipediaDocumento29 páginasWikipediaradhakodirekka8732Ainda não há avaliações

- The Little MermaidDocumento6 páginasThe Little MermaidBobbie LittleAinda não há avaliações

- Viva Questions For Even SemestersDocumento22 páginasViva Questions For Even SemestersSiddhanta DuttaAinda não há avaliações

- Public Economics - All Lecture Note PDFDocumento884 páginasPublic Economics - All Lecture Note PDFAllister HodgeAinda não há avaliações

- Ecosystems FYBCom PDFDocumento41 páginasEcosystems FYBCom PDFShouvik palAinda não há avaliações

- Roundtracer Flash En-Us Final 2021-06-09Documento106 páginasRoundtracer Flash En-Us Final 2021-06-09Kawee BoonsuwanAinda não há avaliações

- Adherence Tradeoff To Multiple Preventive Therapies and All-Cause Mortality After Acute Myocardial InfarctionDocumento12 páginasAdherence Tradeoff To Multiple Preventive Therapies and All-Cause Mortality After Acute Myocardial InfarctionRoberto López MataAinda não há avaliações

- GSM Rtu Controller Rtu5011 v2 PDFDocumento27 páginasGSM Rtu Controller Rtu5011 v2 PDFAbdul GhaniAinda não há avaliações

- Mini Test 2 - HSDocumento4 páginasMini Test 2 - HSNgan Nguyen ThuAinda não há avaliações

- Oleg Losev NegativeDocumento2 páginasOleg Losev NegativeRyan LizardoAinda não há avaliações

- Stock Trak AssignmentDocumento4 páginasStock Trak AssignmentPat ParisiAinda não há avaliações

- Harvester Main MenuDocumento3 páginasHarvester Main MenuWonderboy DickinsonAinda não há avaliações